We hear this everywhere and it’s common knowledge that we live in a consumer-driven society. With prices sky-rocketing and the possibility that GST will be increased to 9% is not helping the increase in expenses.

We ALL know that it’s important to spend our money wisely and keep track of our finances and that is what Seedly is all about; helping people in their personal finance! Knowing this, how do we know if we are spending excessively, in other words, if we are spending beyond our means?

This guide is based on the average Singaporean, we understand that everyone’s financial situation is different, so do take this with a pinch of salt ?

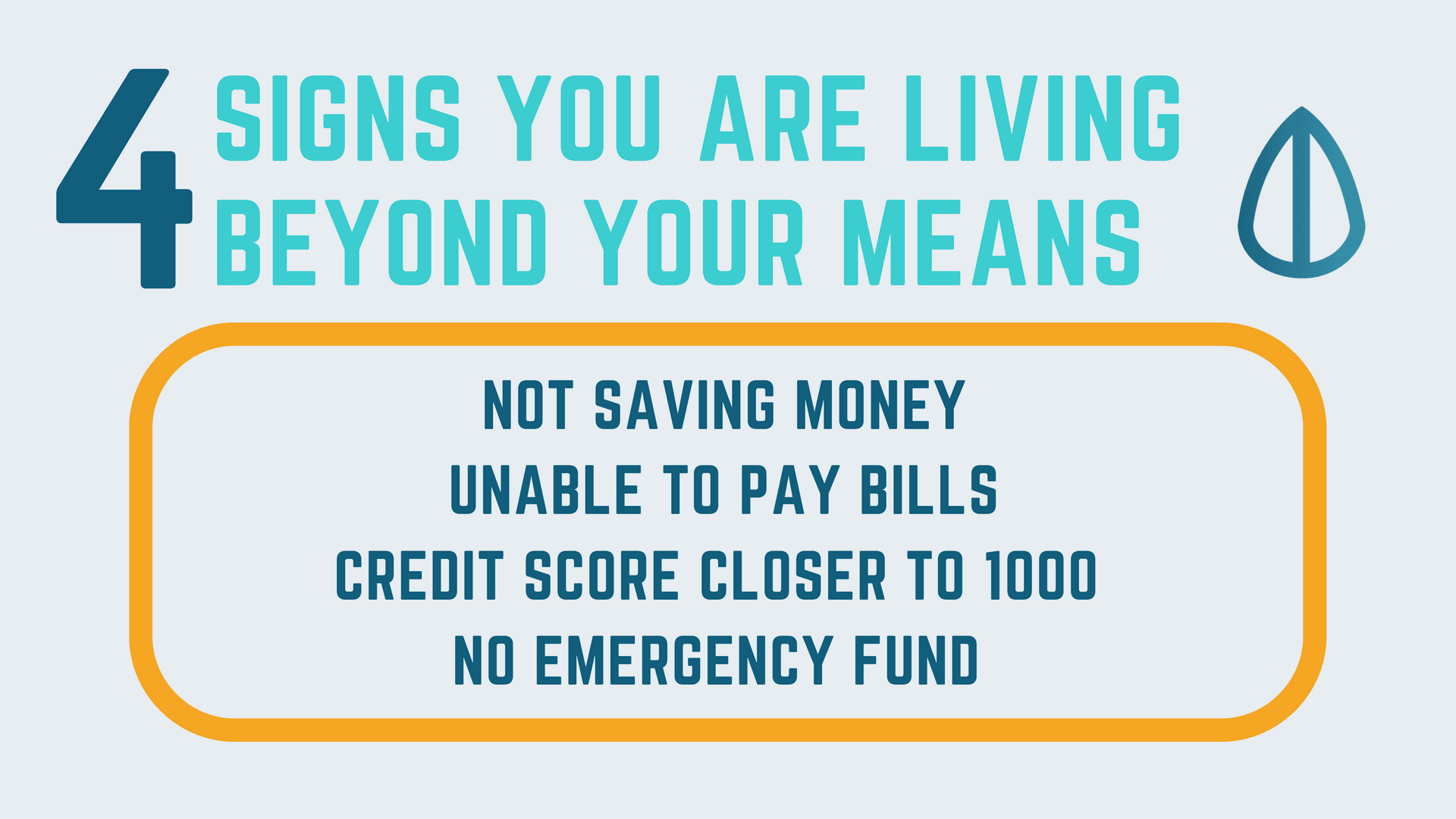

1. You Are Not Saving Money

In our article on allocating your monthly salary, we talked about how certain percentages of your salary should go to. The ideal percentage that should go into your savings account would be 20%. Assuming the average salary is $2,200 (inclusive of employer and employee contribution), that would mean approximately $440 should be placed in your savings.

However, let’s say you find 20% too much for placing in your savings account but if you find yourself struggling to put in 5% ($110), it’s a possible sign you are living beyond your means or you just have to allocate your money properly!

2. You Are Unable To Pay Your Bills

The older we get the more bills we have and we start to lose track of what has and has not been paid. It gets exciting when you buy new items and when it’s paid in instalments, it doesn’t sound as bad.

There is, of course,e the benefit of buying items on your credit card which does help to improve your credit score but what happens when you aren’t able to pay your bills (not to mention the minimum amount!)?

This is when your bills start to roll over and before you know it, you’re neck-high in debt and struggling to get out. So, if you find yourself experiencing this, snap out of it and pay off your bills when you can!

Here are some hacks that will help you clear your debt ASAP!

3. Your Credit Score Is Closer To 1000

Following the message of paying your bills on time, you don’t want your credit score to be affected by your poor payment history. According to Investopedia, payment history is the major component that is looked at when considering granting loans!

Taken from Credit Bureau Singapore (CBS), credit scores range from 1000 to 2000. The closer you are to 1000 the lower your credit score and the higher you are to 2000, the higher your credit score.

Here’s how you can improve your credit score:

- Pay your bills on time

- Make sure you have lesser debt compared to your credit limit.

- Have a positive credit history: It’s good to show you have a long history of using credit. Whether you have a short or long history, make sure it’s a good one!

- Cut out credit cards you don’t need: Banks see an excessive amount of new credit as a high credit risk.

4. You Have No Emergency Savings

Just like saving money, you want to ensure that you have a certain amount set aside for rainy days. Although there is no specific percentage you should set aside from your salary or some people have different forms of emergency funds, it’s always good to know that you have some extra cash to lean on if times get rough.

Take Responsibility For Your Personal Finance!

Just like it says, it is YOUR personal finance and no one else’s! Keep track of your personal finances to ensure that you are paying your bills on time and also where your money is going. Not only that, join a community where you can learn more about your personal finance and get advice from experienced community members 🙂

Advertisement