Age vs Risk Profile: What Investments Should You Be Holding At Your Age?

” How Should I Allocate My Money?” – Everyday Singaporean

Most likely, if you land on this article, there are a few questions bothering you:

- How much of my asset should I be investing?

- Where should I be allocating my money?

- Is that percentage too much for my current age?

The question of asset allocation is a common one. People ask themselves all the time at every stage in life.

Correct Asset Allocation Accounts For 90% Of An Investment’s Return

While many believe that good investment judgement and market timing is the key to an investment’s return, a study on determinants of portfolio performance proves otherwise.

90% of an investment’s return is simply the work of asset allocation and has nothing much to do with investment judgement or market timing. Surprise!

TL;DR – Your percentage of risky assets depend on your life expectancy!

- The rule of thumb to calculate percentage in risky assets: (110 – Current Age) = % of the portfolio in equities

- Your risk appetite should decrease as years past

- Importance of liquidity of assets increases with age

- Female needs fatter retirement sum than their male counterparts

Investment Products In Singapore – According To Risk

Before we break down into details on the percentage one can consider for each asset class, it is good to re-look at the common investment products.

A quick summary:

- High-Risk Products: Cryptocurrencies, Stocks, Unit Trusts and Exchange Traded Funds (ETF)

- Moderate Risk Products: Bonds

- Low-Risk Products: Endowment, Savings in bank

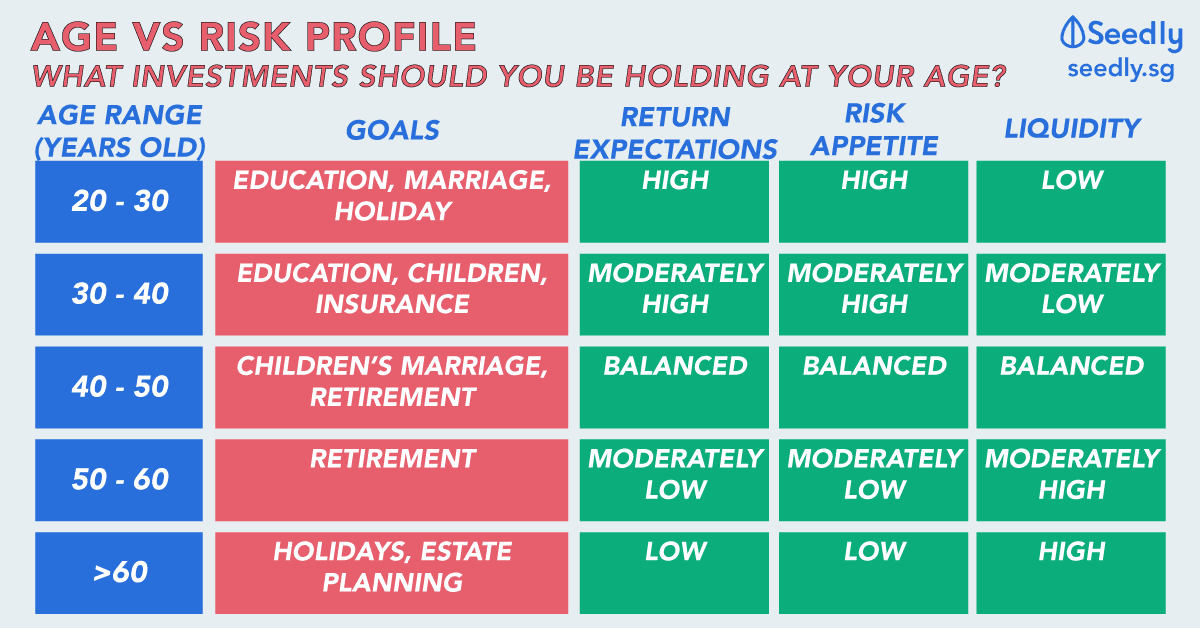

Your Risk Appetite Decreases With Age And Commitment

Your appetite for risk changes over time. At different age range, a typical Singaporean’s goals and priority changes.

| Age Range | Goals | Return Expectations | Risk Appetite | Liquidity |

|---|---|---|---|---|

| 20-30 Years Old | Education, Marriage, Holiday | High | High | Low |

| 30-40 Years Old | Children, Education, Insurance | Moderately High | Moderately High | Moderately Low |

| 40-50 Years Old | Children's Marriage, Retirement | Balanced | Balanced | Balanced |

| 50-60 Years Old | Retirement | Moderately Low | Moderately Low | Moderately High |

| More than 60 Years Old | Holidays, Estate Planning | Low | Low | High |

Singaporean’s Priority at 20 to 30 years old ( High returns expectations, High risk appetite, Low liquidity)

One basic rule of thumb that was recommended is:

(110 – Your Age) = % of the portfolio that should be in equities

The formula used to be (100- Age), but some experts have altered the number to cater for longer life expectancy. You can also change the number to (120-Age) should you have a larger appetite for risk.

Singaporeans at this age have a few pros and cons when it comes to investing.

Pros at this age range:

- Less commitment

- More years to recover any possible losses due to inevitable events

Cons at this age range:

- Low Salary

- Little experience when it comes to investing

If you fall into this age group, investing will come in 2 phases.

Assuming you have saved up enough for your rainy day funds, Pitzl Financial suggests that new investors in this age range can start off with less than 60% in high-risk investment (mainly stocks) with the remaining of his investment funds in bonds. Once he gained enough experiences and confidence in the market, he will then move on to 70% to 80% in high-risk investment and the remaining in bonds.

Singaporean’s Priority at 30 to 40 years old ( Moderately High Returns Expectations, Moderately High-risk appetite, Moderately Low liquidity)

Pros of this life stage:

- Getting a better salary

- Enough number of years to recover any possible losses due to inevitable events

- Enough experience in investing

Cons of this life stage:

- Higher responsibilities: Starting a family, factoring mortgage and children’s expenses

This age range sees the need for more liquidity, especially if they were to start a family. The cost of raising a child till secondary school is an estimated S$276,400 (about $1,400 per month).

Despite the rule of thumb on (110- Your Age) = % of the portfolio in equities, one may wish to change that a little for this age range as due to a few reasons:

- The need to save up for children’s education

- Singaporeans have to deal with mortgage loan

It is only right to ignore the rule for once and cut down on his allocation on risky assets until he is settled the money required in years to come.

Singaporean’s Priority at 40 to 50 years old ( Moderately High Returns Expectations, Moderately High risk appetite, Moderately Low liquidity)

Pros of this life stage:

- Hitting the peak for your salary

Cons of this life stage:

- Financial commitment might be high due to children going to college and universities

- Lesser time to plan for retirement

Middle age is the time to work backwards to find out how much more you need before you can retire. It is said that Singaporeans will need about S$376,270 to retire. This is based on expenses of about S$1,200 per month.

Depending on how much you have saved up over the years, the percentage will be balanced between high risks assets such as stocks and low risks one such as bonds.

The risk appetite should depend on how close you are to your retirement plan. Always ensure that you have a good plan to secure the retirement amount in your CPF and savings before putting a higher percentage into risky assets.

Singaporean’s Priority at 50 years old onwards ( Moderately Low returns expectations, Moderately Low risk appetite, Moderately High liquidity)

Pros of this life stage:

- Children might be old enough to provide you with allowance

- Accumulated a good amount of savings

Cons of this life stage:

- Possible health problems, increasing medical cost

- Lesser time to plan for retirement

For Singaporeans, age 55 is the age of which your Ordinary Account and Special Account will combine to form your Retirement Account. Singaporeans will then make a decision to withdraw the difference after setting aside his Basic Retirement Sum or to keep the savings in CPF to earn interest.

This is the transition phase of taking up as little risk as possible, and have cash readily available, in a case of emergency.

The Need For More Retirement Fund

While asset allocation encourages investors to reduce risk over time, it is important to take note of a few factors:

- Female Singaporeans have a life expectancy of 86.1 Years Old while male Singaporeans at 80.6 Years Old. This indicates the need for females to have a fatter retirement sum based on statistics.

- While life expectancy has a chance of increasing due to the advancement of technology, medical inflation should not be overlooked. Medical inflation rate of Singapore stood at a high 15% in the year 2015 and 10% in the year 2016. Both numbers exceeded the global rate.

Advertisement