Medisave Limit 2024

If you’re reading this, you’re probably (somewhat) familiar with CPF (Central Provident Fund) and the various Sums like the Basic Retirement Sum, Full Retirement Sum and Enhanced Retirement Sum.

But I bet there’s one Sum you don’t know much about!

It’s… the Basic Healthcare Sum (BHS)!

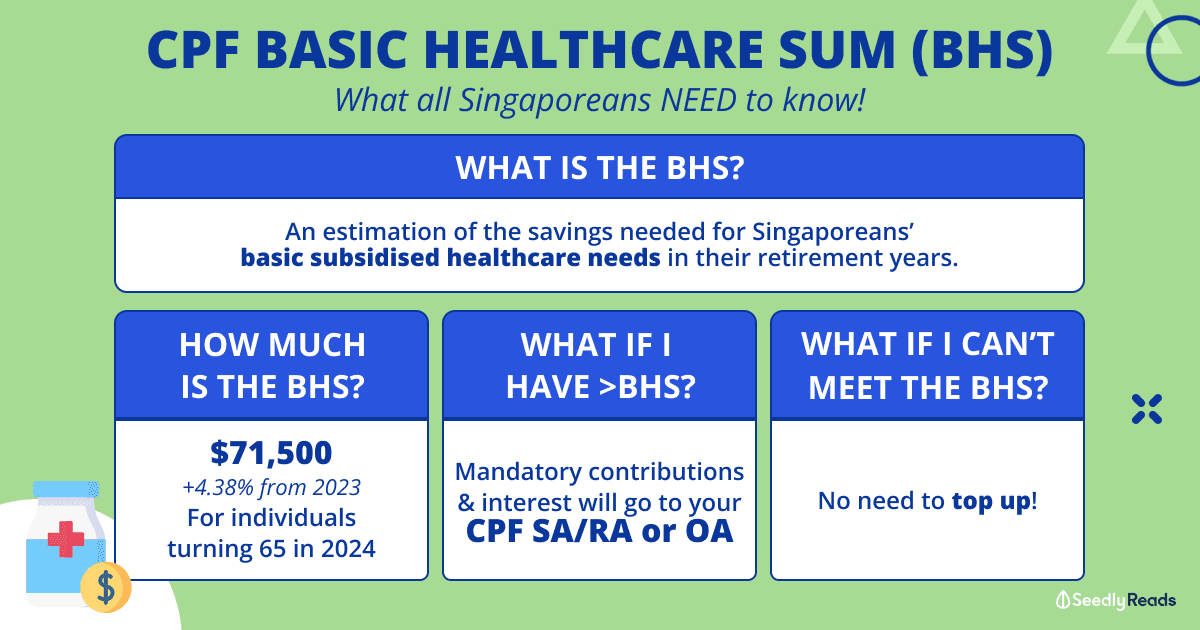

FYI: CPF has just announced the latest Basic Healthcare Sum for individuals turning 65 in 2024, and it’s currently set at $71,500.

Mmhmm, I see question marks popping around you…

So here’s a quick summary of the Basic Healthcare Sum and what it means to you!

TL;DR: Ultimate Basic Healthcare Sum Guide (2024) — What Happens if My MediSave Is Full?

The Basic Healthcare Sum (BHS) is the estimated savings needed for basic subsidised healthcare in old age and is adjusted yearly for members below 65 years old to keep pace with the growth in MediSave use.

But once you hit 65 years old, your BHS will be fixed for the rest of your life.

From 1 January 2024,

- For members below 65 years old, their BHS will be raised from $68,500 to $71,500, a ~4.38% increase.

- For members who turn 65 years old in 2024, their BHS will be fixed at $71,500 and remain fixed for the rest of their lives.

CPF MediSave Cap

FYI: the BHS is the cap to the MediSave Account (MA), so any excess will be automatically transferred to your other CPF accounts. In other words, the BHS is a CPF MediSave cap of sorts.

If you have less than the BHS, you don’t need to top up your MA.

And you can still withdraw from your MA to pay for approved medical expenses.

Click to Teleport

- What Is The Basic Healthcare Sum (BHS)?

- How Much Is The Basic Healthcare Sum? CPF MediSave Cap Explained

- What Happens When MediSave is Full, and I Hit The Basic Healthcare Sum?

- What Is the Minimum Sum for Medisave Account?

- Should I Top Up MediSave to Hit the BHS / CPF MediSave Cap?

What Is The Basic Healthcare Sum (BHS)? What Is the Cap for Medisave in 2024?

Don’t worry; this is not another milestone in CPF that you must hit by hook or by crook.

The Basic Healthcare Sum (BHS) is simply an estimate of an amount you should keep handy in your CPF MediSave account to care for your healthcare needs in your retirement years.

Some of you may not be that familiar with MediSave.

And I’d say that’s a good thing because it means you’re safe and healthy.

But just in case you ever need to use it (touch wood), your MediSave can be used for the following:

- A range of approved treatments and healthcare needs

- Paying for various healthcare insurance such as MediShield, Integrated Shield Plan, Eldershield and CareShield.

How Much Is The Basic Healthcare Sum? What Is the Minimum Sum for Medisave Account?

It works differently from the three Retirement Sums in your Retirement Account, allowing you to purchase your CPF LIFE plan.

You need to maintain no minimum balance in your MediSave Account.

“So… the sky’s the limit,” you ask?

Nope.

For your MediSave Account, the Basic Healthcare Sum is your cap.

Just like the Retirement Sums, CPF adjusts the Basic Healthcare Sum regularly as it has to consider inflation and the rising cost of healthcare.

Since it’s for healthcare needs post-retirement, your BHS will be fixed when you turn 65 years old.

The BHS for individuals turning 65 years old in 2024 is set at $71,500.

| Age in 2024 | Year when cohort turned age 65 | Cohort BHS (fixed for life) |

|---|---|---|

| 65 | 2024 | $71,500 |

| 66 | 2023 | $68,500 |

| 67 | 2022 | $66,000 |

| 68 | 2021 | $63,000 |

| 69 | 2020 | $60,000 |

| 70 | 2019 | $57,200 |

| 71 | 2018 | $54,500 |

| 72 | 2017 | $52,000 |

| 73 and above | 2016 or earlier | $49,800 |

Looks pretty manageable, right?

But just like the FRS, by the time you turn 65, the Basic Healthcare Sum will definitely be way higher.

“So… how much higher,” you ask?

| 65th Birthday in | Basic Healthcare Sum (BHS) | Percentage Increase |

|---|---|---|

| 2016 | $49,800 | - |

| 2017 | $52,000 | 4.42% |

| 2018 | $54,500 | 4.81% |

| 2019 | $57,200 | 4.95% |

| 2020 | $60,000 | 4.90% |

| 2021 | $63,000 | 4.87% |

| 2022 | $66,000 | 4.65% |

| 2023 | $68,500 | 3.78% |

| 2024 | $71,500 | 4.38% |

| 2030 | $92,258 | Projected 4.60% increase p.a. |

| 2040 | $151,746 | |

| 2050 | $219,656 | |

| 2060 | $307,524 |

Looking at the current rate of increase, we’re looking at an average increase of ~4.60% per annum.

Disclaimer: This is JUST a projection; I’m sure the government will adjust accordingly.

What Happens When MediSave is Full, and I Hit The Basic Healthcare Sum?

Topping up your CPF to meet the Full Retirement Sum or other reasons is always a hot topic amongst Singaporeans.

Even if you choose not to make top-ups and keep working after your CPF savings are more than sufficient.

It’ll come to a point where you’ll STILL be making mandatory CPF contributions.

So what happens to the money that’s supposed to go into your MediSave?

What if You Have More Than the Basic Healthcare Sum?

Where do they all go now that you’ve hit your Basic Healthcare Sum?

| Age | Condition | Account that Mandatory Contributions & Interest Goes To |

|---|---|---|

| Below 55 years old | If you've not met the prevailing FRS in your Special Account | Special Account |

| If you've already met the prevailing FRS in your Special Account | Ordinary Account | |

| 55 years old & above | If you've already met your FRS (or BRS with a property) in your Retirement Account | Ordinary Account |

Don’t worry, guys; your money won’t disappear!

However, it seems like letting your MediSave savings (which gets a 4.08% interest) go to your Ordinary Account (which only gets 2.5% interest) instead appears like you’re being shortchanged…

What Is the Minimum Sum for Medisave Account? What Happens If I Don’t Meet The Basic Healthcare Sum?

Remember that you can withdraw some monies from your CPF accounts when you turn 55, depending on your CPF balances?

While the Retirement Sum is something you must hit for your CPF LIFE plan, the Basic Healthcare Sum is more of a good to have…

It’s NOT a must for you to meet it.

So it’s OK if you can’t hit the BHS for your cohort!

Should You Do a MediSave Contribution and Top Up MediSave to Hit the BHS?

You’re not required to top up with cash to fulfil the BHS when you make your first withdrawal at age 55 or when the BHS is fixed for you at age 65.

Should I Top Up MediSave to Hit the BHS / CPF MediSave Cap?

Now, just like how we’ve always been saying that you shouldn’t let CPF LIFE be your entire retirement portfolio, the same goes for your healthcare expenses!

Treat the Basic Healthcare Sum like a bonus to supplement the safety nets you’ve set to take care of yourself if you fall sick.

Read More

Advertisement