Planning to travel?

Gone are the days when we solely rely on foreign currency to spend overseas.

These days, with multi-currency cards and credit cards offering better exchange rates than money changers, and the ability to withdraw cash overseas should you need them, cash is becoming less prevalent, especially if you are travelling to a developed country.

But that’s not all, with credit cards, you have the ability to maximise your spending and even earn rewards such as cashback or miles while overseas!

So which cards should you be spending on to get the best bang for your buck? Here’s the ultimate guide to maximising your spending overseas!

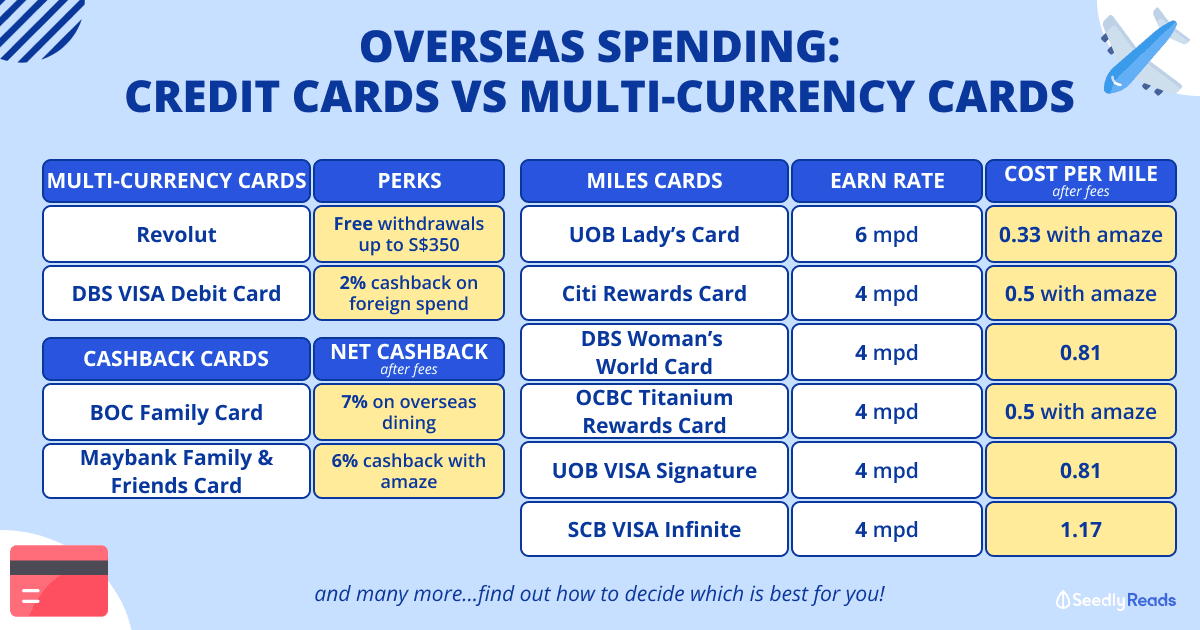

TL;DR: Best Cards For Overseas Spending

When travelling overseas, you’ll be spending in foreign currency, and that means that you will have to deal with foreign currency conversions.

For us, this means two things:

- A foreign currency (FX) spread whereby we are charged a “hidden” fee in addition to the underlying exchange rate.

- Foreign Currency Conversion (FCY) fees whereby we are charged a percentage of the value we intend to exchange.

As consumers, this means that we are paying financial institutions every time we want to convert our currencies. A given, of course.

That’s why I am here to help you find the best way to minimise such costs!

If you prefer a more fuss-free experience with the best exchange rates and no FCY fees, I would highly recommend using a multi-currency card such as Revolut.

But if you’re a miles person or someone who is willing to put in the effort to maximise rewards, credit cards are the better option.

Jump to:

- Best Multi-Currency Cards for Overseas Spending

- Should You Use A Credit Card for Overseas Spending?

- Best Cashback Credit Cards for Overseas Spending

- Best Miles Credit Cards for Overseas Spending

Best Multi-Currency Cards for Overseas Spending

Multi-currency cards are the most fuss-free way to spend overseas as they mostly have ZERO currency conversion fees and the best exchange rates.

Additionally, multi-currency cards allow you to lock in good exchange rates beforehand if you know that the rates are going to be worse closer to your trip.

The winner for this category would be Revolut, not only for its features but also for its competitive exchange rate.

Here is a quick snapshot of how much Japanese Yen I would get when exchanging on the following platforms (taken within minutes of each other):

- Revolut: S$1 = ¥110

- Instarem: S$1 = ¥110

- YouTrip: S$1= ¥111

- DBS: S$1 = ¥110.01

While YouTrip does seem to give the best exchange rate at this point in time, do note that these exchange rates fluctuate and the rankings would change. In our previous version of this article, Revolut gave the best exchange rate for example.

Thus, we should look for features to determine the best card for overseas spending.

Unlike YouTrip, Revolut allows you to withdraw any spare cash you have post-trip back into your bank account! Plus, it has virtual cards that you can delete immediately after your trip for more security.

Last but not least, Revolut now has a huge edge over its competitors with its limit/stop order feature. To put it simply, you can set a target exchange rate and the app will automatically convert your money for you when it hits that specified rate!

However, do note that you may be hit with the 1% currency conversion fees during the weekend (between Friday 5pm (New York time) and Sunday 6pm (New York time)).

A close runner-up would be DBS’ new DBS VISA Debit card. This card gives an awesome 2% cashback, but only if you hit the minimum spend requirement of S$500 and a cash withdrawals limit of S$400 and below in the same month. If you are able to hit the cashback, it will completely offset the FX spread loss you will incur compared to Revolut, and you can earn about 0.8% net cashback.

Do note that this is only the case for a Japan trip at the time of writing and your results may differ depending on where you’re heading to!

The only reason it isn’t at the top is that it charges you up to S$7 for overseas cash withdrawals and only supports 11 currencies compared to Revolut’s 150+.

| Multi-Currency Card/Account | Currency Conversion Fees | No. of Supported Currencies (Exchange & Store Currencies) | No. of Currencies Available for Overseas Spend | Overseas ATM Withdrawal Fees | Note |

|---|---|---|---|---|---|

| Revolut Apply Now | 0% - 1% Weekdays: 0% Weekends (between Friday 5pm (New York time) and Sunday 6pm (New York time): 1% | 33 (AED, AUD, BGN, CAD, CHF, CLP, COP, CZK, DKK, EGP, EUR, GBP, HKD, HUF, ILS, INR, JPY, KRW, KZT, MXN, NOK, NZD, PHP, PLN, QAR, RON, SAR, SEK, SGD, THB, TRY, USD, ZAR) | 150+ | Free for first S$350 or first five withdrawals (Standard members) per rolling month 2% thereafter or $1.49 whichever is higher | Expensive to use on the weekends |

| YouTrip | 0% | 10 (SGD, USD, EUR, GBP, JPY, HKD, AUD, NZD, CHF, SEK) | 150+ | Free cash withdrawals of up to S$400 per calendar month, 2% thereafter | Unable to transfer money out |

| DBS Visa Debit Card | 0% | 11 (AUD, CAD, EUR, HKD, JPY, NZD, NOK, GBP, SEK, THB, USD) | 11 (AUD, CAD, EUR, HKD, JPY, NZD, NOK, GBP, SEK, THB, USD) | Up to S$7 per cash withdrawal depending on ATM | 2% cashback on all foreign spend with S$500 min. spend and cash withdrawals limit of S$400 and below in the same month. |

| amaze wallet (Instarem) Apply Now | 0% | 10 (SGD, EUR, USD, JPY, THB, GBP, AUD, CHF, NZD, and CAD.) | 150+ | 2% | 0.50% cashback in InstaPoints |

| Wise | From 0.43% (dynamic, depends on forex market and currencies) | 51 (AUD, GBP, HRK, HUF, JPY, MYR, NOK, NZD, PLN, RON, SEK, SGD, TRY, USD and more) | 150+ | Free for first S$350 & the first 2 withdrawals per 30-day cycle 1.75% thereafter for amounts >S$350 + S$1.50/transaction fee after first two free withdrawals | $8.33 - $8.55 card issuance fee |

| WireX | 0% | 12 (AUD, CAD, CHF, CZK, USD, EUR, GBP, HKD, JPY, MXN, NZD, SGD) | 150+ | Free for first S$200 per 30-day cycle 2% thereafter | 2% cashback in WXT (cryptocurrency) $5 card delivery fee via SingPost |

For a more in-depth look at multi-currency cards, check out this article:

Should You Use A Credit Card for Overseas Spending?

If you want to further maximise your spending overseas and have better fraud protection, here’s where credit cards come into play.

FCY Fees

![]()

However, when spending overseas with credit cards you will be charged an FCY fee typically between 3% – 3.5% (they have been increasing over the years too).

Not to mention, banks also have a terrible FX spread or exchange rate. Yes, that’s how they make money “secretly” from us when we use credit cards overseas. Based on my calculations above, the FX spread loss for DBS at least is about 1%. So for the following tables below, do know that you are also losing about 1% in value that is not included in the calculations.

How can us consumers even earn rewards then if we are being charged such fees? The answer is in the magnitude of the rewards and the calculations.

Let’s take a simple unlimited cashback card that gives us 1.5% cash back on virtually everything. With an FCY fee of let’s say 3%, we are basically giving the banks free money.

However, this completely if the cashback percentage or value goes the FCY fees and FX spread. We can also use the amaze card by Instarem which gets rid of FCY fees!

For the uninitiated, the amaze card converts our foreign currency spending to local currency spending for up to 5 MasterCards that you link with it. Yep, only MasterCards. While it is still a superb card for overseas spending, there is an implicit FX spread loss of about 2% now (according to online forums). So technically, the amaze card is just making it about 1% – 1.5% cheaper when you can use it overseas compared to just using the bank’s credit cards itself.

Moreover, the amaze card also gives an additional 0.5% cashback on overseas spend when you use it as a credit card (the wallet feature doesn’t count) in the form of Instapoints. However, it is a bit restrictive when it comes to the conditions you need to fulfill and you can only redeem in blocks of S$20, which is why I won’t be considering it on top of the existing credit card rewards.

Avoid DCC!

When spending with credit cards overseas, you will need to be wary of Direct Currency Conversion. This service basically charges you a whole lot more than FCY fees and is something you want to avoid at all costs.

How? Make sure that you are being billed in the local currency of the country that you are in. This is something that merchants may try to cheat you with and profit from if you are unlearned.

The following tables will only include some of the top credit cards for each category. If your card isn’t listed, you’ll have to do your own calculations to find out if you will be earning if at all!

If the card is applicable to be used with amaze for lower fees, it will be included in the calculations as well.

Best Cashback Credit Cards for Overseas Spending

| Cashback Credit Card | Cashback Rate | FCY Fees | Net Cashback |

|---|---|---|---|

| Bank of China Family Card Apply Now | 10% on overseas dining | 3% | 7% cashback on overseas dining |

| Maybank Family & Friends Card Apply Now | 8% with S$800 min spend | Pair with amaze (~2% FX spread loss) / 3.25% | 6% cashback with amaze capped at $25 for each category (up to 5) / 4.75% cashback capped at $25 for each category (up to 5) |

| OCBC FRANK | 8% with S$800 min spend | Pair with amaze (~2% FX spread loss) / 3.25% | 6% cashback capped at $25 for Amaze pairing, 4.75% cashback capped at $25 for FX transactions |

| OCBC 365 Apply Now | 6% on overseas dining with S$800 min spend | 3.25% | 2.75% cashback on overseas dining |

| NTUC/Trust Link Card | 0.22% in Linkpoints on overseas spend | 0% | 0.22% in Linkpoints on overseas spend |

NTUC/Trust Link card is only included as it is special with 0% FCY fees. You may find other credit cards with much better cashback rates.

Best Miles Credit Cards for Overseas Spending

For miles players, using miles credit cards will only make sense depending on how you value a mile and how much you’re paying for miles overseas. I have included the cost per mile for the best miles credit cards and when paired with amaze for easy reference.

| Miles Credit Card | Earn Rate | FCY Fees | Cost Per Mile |

|---|---|---|---|

| Specific Overseas Spending | |||

| UOB Lady’s Card Apply Now | 6 mpd (Pick 1 category from beauty & wellness, dining, entertainment, family, fashion, transport, travel) | Pair with amaze (~2% FX spread loss) / 3.25% | 0.33 with amaze / 0.54 |

| UOB Lady’s Solitaire Card | 6 mpd (Pick 2 category from beauty & wellness, dining, entertainment, family, fashion, transport, travel) | Pair with amaze (~2% FX spread loss) / 3.25% | 0.33 with amaze / 0.54 |

| Citi Rewards Credit Card Apply Now | 4 mpd on online shopping, retail purchases, rides, online groceries and food delivery | Pair with amaze (~2% FX spread loss) / 3.25% | 0.5 with amaze / 0.81 |

| DBS Woman's World Mastercard Apply Now | 4 mpd on online purchases | 3.25% | 0.81 |

| OCBC Rewards Card Apply Now | 4 mpd on online transactions | Pair with amaze (~2% FX spread loss) / 3.25% | 0.5 with amaze / 0.81 |

| UOB Preferred Platinum Visa Card | 4 mpd on online transactions | 3.25% | 0.81 |

| HSBC Revolution Credit Card Apply Now | 4 mpd on online transactions and contactless payments | 3.25% | 0.81 |

| General Overseas Spend | |||

| UOB Visa Signature | 4 mpd with S$1k min. spend in foreign currency and S$1k min. spend in local currency | 3.25% | 0.81 |

| Maybank Horizon Visa Signature Card Apply Now | 3.2 mpd (valid till 31 Jan 2024) | 3.25% | 1.02 |

| SCB Visa Infinite Credit Card | 1 + 2 mpd with S$2k min. spend | 3.50% | 1.17 |

| SCB Rewards+ Card Apply Now | 2.9 mpd | 3.50% | 1.21 |

| UOB PRVI Miles Mastercard Apply Now | 2.4 / 1.4 with Amaze | 3.25% / Pair with amaze (~2% FX spread loss) | 1.35 / 1.43 with amaze |

| UOB PRVI Miles Visa Card Apply Now | 2.4 | 3.25% | 1.35 |

| UOB PRVI Miles AMEX Apply Now | 2.4 | 3.25% | 1.35 |

What cards are you using when spending overseas? Let us know in the comments below!

Related Articles

Advertisement