Only Want One Credit Card? Here Are The Ones That Cover The Most Categories!

Seedly

Seedly●

Are you someone who prefers simplicity and would rather just have one credit card to concentrate all your spending on?

Or perhaps you’re just someone who can’t be bothered with all the Merchant Category Codes (MCCs) and all sorts of other Terms and Conditions (T&Cs)?

Well, you’ve come to the right place!

As someone who has a ton of credit cards now, I feel the pain of dealing with all T&Cs, MCCs, and having just one too many CCs (credit cards).

So, if I could only have one credit card, here are my recommendations based on the widest coverage of categories, ease of use, and rewards!

TL;DR: Best Credit Cards With The Most Spending Categories

Disclaimer: This is a non-sponsored article. The information provided by Seedly serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before signing up for any products.

Which Credit Card Suits You?

Before we begin, you’ll need to identify what type of credit card suits you!

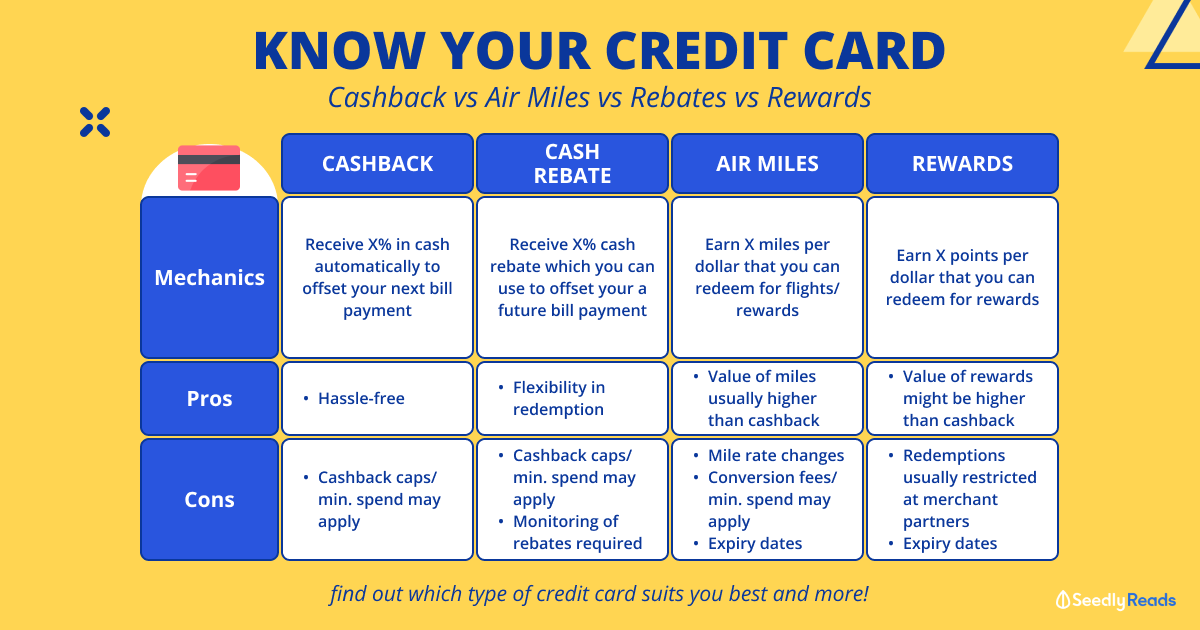

In general, cashback credit cards are less complicated than miles or rewards, but for the full rundown of differences, check out this article:

As always, everyone’s spending habits are different, and other cards may be better suited for you.

However, for this article, I will recommend just two credit cards that most adults should consider having.

Assumptions:

- An adult earning more than $30k annually

- Has good financial discipline to own a credit card

Unlimited Cashback Credit Cards

As mentioned previously, cashback credit cards are some of the simplest credit cards to use. These cards are the most fuss-free but come at the cost of lesser rewards when compared to miles or rewards credit cards.

Then again, you really can’t put a price tag on simplicity!

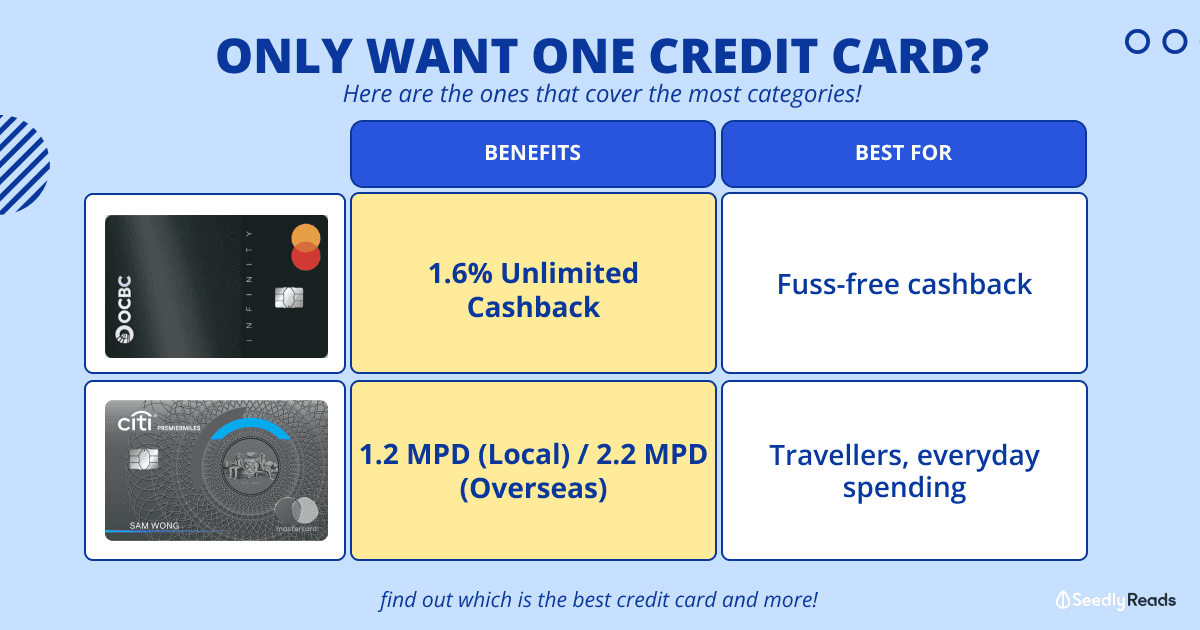

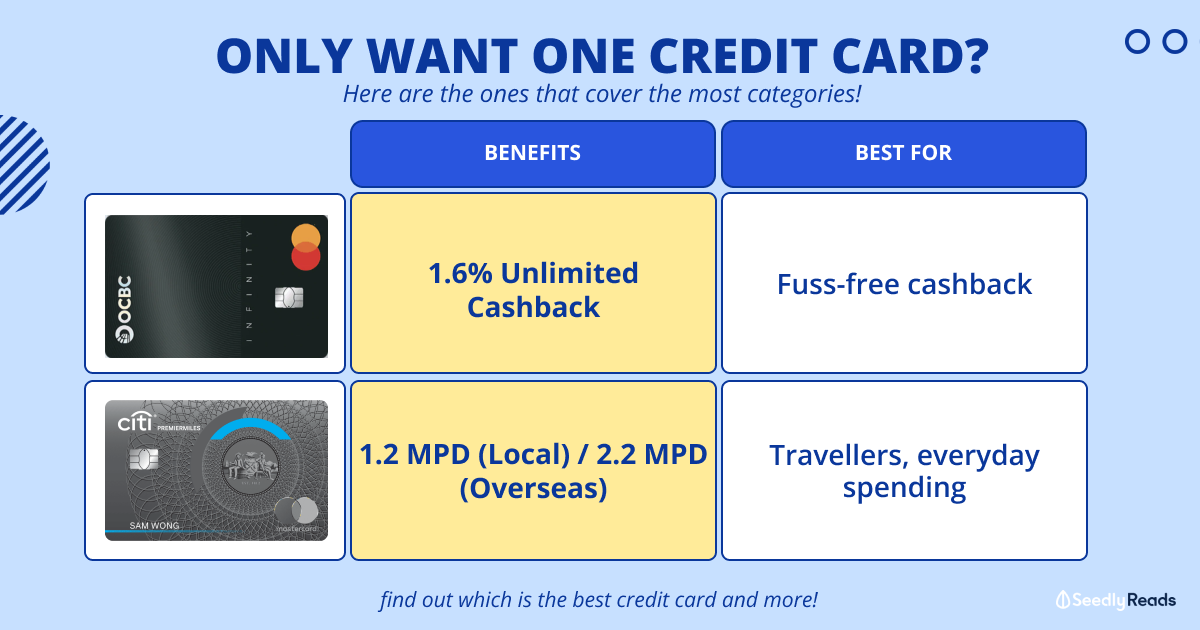

The best unlimited cashback card currently is the OCBC INFINITY Cashback credit card

Apply Now

OCBC INFINITY Cashback Credit Card:

- Cashback: 1.6% on eligible spending

- Minimum monthly spend: None

- Cashback cap: None

- Principal-card annual fee: S$192.20

- Annual-fee waiver: First year free

- Minimum age: 21

- Minimum annual income:

- S$30,000 for Singaporeans and PRs aged 21 to 55

- S$15,000 for Singaporeans and PRs above 55

- S$45,000 for foreigners

Furthermore, OCBC credits the cashback automatically. As a result, you do not have to monitor a rewards catalogue or convert points before receiving value.

SingSaver promotion

Eligible new OCBC cardmembers who apply through SingSaver from 1 July to 2 August 2026 and spend at least S$400 in qualifying transactions within 30 days of approval may qualify for SingSaver rewards such as S$400 Cash via PayNow, 25,000 Max Miles by HeyMax (worth S$600+ in travel value) or Dyson Airstrait™ straightener (worth S$799)!

Available reward choices and stock may change during the campaign. Therefore, check the live SingSaver product page before applying and review the eligibility and fulfilment conditions carefully.

Is OCBC INFINITY the best credit card for everything?

It is a strong choice for simplicity, but it is not automatically the best card for every person.

For example, the UOB Absolute Cashback Card advertises a higher baseline rate of 1.7%. However, it operates on the American Express network. Therefore, you should consider whether the merchants you use regularly accept Amex.

Meanwhile, Citi Cash Back+ also offers 1.6% unlimited cashback with no minimum spend or cashback cap. In addition, eligible Citi Plus customers may receive an extra 0.4% bonus cashback, subject to the account requirements and monthly bonus cap.

The American Express True Cashback Card is another option. It offers 3% cashback on up to S$5,000 of spending during the first six months, followed by 1.5% unlimited cashback on subsequent eligible purchases, with no minimum spend.

Consequently, the best option depends on your priorities:

| Card | Baseline benefit | Best suited for |

| OCBC INFINITY | 1.6% cashback | Readers who want simple Mastercard cashback |

| UOB Absolute Cashback | 1.7% cashback | Readers whose regular merchants accept Amex |

| Citi Cash Back+ | 1.6% cashback | Existing Citi users or eligible Citi Plus customers |

| American Express True Cashback | 1.5% ongoing cashback | Readers who prefer Amex and want a temporary introductory earn rate |

Higher Cashback/Miles/Rewards Credit Cards

You may prefer a rewards or miles card if you are willing to track eligible transactions and monthly caps.

These cards can offer higher returns. However, they may exclude certain merchants, transaction types or payment methods. Therefore, always read the card’s rewards terms rather than assuming every transaction will earn the advertised rate.

Citi PremierMiles Card

Apply Now

The Citi PremierMiles Card is designed specifically for general-spend simplicity. Instead of making you cross-reference merchant category codes, it offers a clean, uncapped earning structure:

- 1.2 Citi Miles per S$1 on all local spending.

- 2.2 Citi Miles per S$1 on foreign currency spending overseas.

- Up to 10 Citi Miles per S$1 on dedicated online partner bookings like Kaligo.

The absolute best part? Your miles never expire. This makes it an incredibly forgiving “everything card” because you can accumulate your rewards slowly over several years without worrying about a looming deadline. It also comes with 2 complimentary airport lounge visits per year via Priority Pass.

Key Parameters:

- Minimum Annual Income: S$30,000 for Singaporeans and PRs (S$42,000 for foreigners).

- Principal-card annual fee: S$196.20 (First year free).

SingSaver Promotion

Because this card is a mainstay on SingSaver, new-to-bank applicants who apply via the platform, opt-in for marketing consent, and hit a minimum spend of S$500 within 30 days of approval can secure major sign-up perks.

Depending on the active flash deal window, rewards range from upsized cash payouts (via PayNow) to premium tech gadgets like a Dyson Airstrait™ or Apple ecosystem devices. Always check the live product link to lock in the current month’s inventory.

Here are other cards you can consider for travel-related expenses:

| Credit Card | Earn Rate | Min. Annual Income |

|---|---|---|

| Citi PremierMiles Mastercard Apply Now | 10 mpd on hotel transactions at Kaligo (Valid till 31 December 2026) Up to 7.2 Citi Miles per S$1 on Agoda bookings till 31 Dec 2026, for stays till 30 Apr 2027 | $30k |

| Citi PremierMiles Visa Card Apply Now | 10 mpd on hotel transactions at Kaligo (Valid till 31 December 2026) Up to 7.2 Citi Miles per S$1 on Agoda bookings till 31 Dec 2026, for stays till 30 Apr 2027 | $30k |

| UOB PRVI Miles Mastercard Apply Now | Up to 8 mpd on Agoda bookings till 31 Aug 2026, for stays till 30 Nov 2026; up to 8 mpd on selected Expedia hotel/activity bookings and 3 mpd on eligible flights till 31 Mar 2027 | $30k |

| UOB PRVI Miles Visa Card Apply Now | Up to 8 mpd on Agoda bookings till 31 Aug 2026, for stays till 30 Nov 2026; up to 8 mpd on selected Expedia hotel/activity bookings and 3 mpd on eligible flights till 31 Mar 2027 | $30k |

| UOB PRVI Miles AMEX Apply Now | Up to 8 mpd on Agoda bookings till 31 Aug 2026, for stays till 30 Nov 2026; up to 8 mpd on selected Expedia hotel/activity bookings and 3 mpd on eligible flights till 31 Mar 2027 | $30k |

| DBS Altitude Visa Signature Card Apply Now | Up to 1.3 mpd local and up to 2.2 mpd overseas | $30k |

| DBS Altitude American Express Card Apply Now | Up to 1.3 mpd local and up to 2.2 mpd overseas | $30k |

| UOB Lady's Card Apply Now | 4 mpd (up to 10 mpd when you save with UOB Lady's Savings Account. Travel must be chosen as a preferred category, capped at S$1k per month) | $30k |

| UOB Lady's Solitaire | 4 mpd (up to 10 mpd when you save with UOB Lady's Savings Account. Travel must be chosen as a preferred category, capped at S$1.5k per month) | $120k |

| HSBC Revolution Apply Now | Up to 4 mpd for regular cardholders, or up to 8 mpd with qualifying HSBC Everyday Global Account relationship, on eligible online/contactless spend including travel | S$65,000 for new/most customers; lower threshold only for selected existing HSBC customers |

| DBS Woman’s World Card Apply Now | 4 mpd (Limit S$1k per month) | $80k |

Afterthoughts

Again, I would like to stress that everyone’s preferences for credit cards are different. But for most Singaporeans who only want to use one credit cards, the above are the recommended cards!

Are you using just one credit card? Comment below and tell us why it is the best credit card for you!

Related Articles

Advertisement