On 22 January 2020, CapitaLand Mall Trust (CMT) (SGX: C38U) and CapitaLand Commercial Trust (CCT) (SGX: C61U) announced a proposed merger by way of a trust scheme arrangement.

The news should not come as a big surprise to many as there had already been three REIT mergers in Singapore in 2019 alone, and CMT-CCT’s announced merger looks set to become the fourth.

Both CMT and CCT can be considered behemoths in their own right.

The former owns 15 quality shopping malls in Singapore located in strategic suburban and downtown areas, with a total property value of S$11.8 billion and a market capitalisation of S$9.55 billion.

The latter is Singapore’s first listed commercial REIT with a total of 10 properties (eight in Singapore and two in Germany), with a total property value of S$11.1 billion and market capitalisation of S$8.22 billion.

This merger will create an even bigger giant in the REIT space, with a merged property value of close to S$23 billion consisting of 24 properties (Raffles City is shared between both CMT and CCT).

The merged entity will be known as CapitaLand Integrated Commercial Trust or CICT.

Mechanics of the Deal

The mechanics of the deal will be as follows: CMT will acquire all the issued and paid-up units of CCT, and all CCT unitholders will receive 0.72 new CMT units plus S$0.259 in cash per CCT unit.

CMT’s issue price for new shares will be fixed at S$2.59 per consideration unit, which means each CCT unitholder will receive S$1.8648 in value in CMT shares (S$2.59 x 0.72).

When added to the S$0.259 in cash, the total consideration that each CCT unitholder will receive is S$2.1238 per unit.

This works out to be a gross exchange ratio of 0.82 times (calculated as the consideration amount of S$2.1238 divided by CMT’s issue price of S$2.59). CMT and CCT will hold their respective extraordinary general meetings (EGMs) in May 2020 and there will also be a scheme meeting to approve the merger.

The expected delisting of CCT is expected to take place in June 2020.

Benefits of the Merger

There are quite a number of benefits arising from this transaction, and I will be pointing out the key pros of the deal before diving into the cons later on.

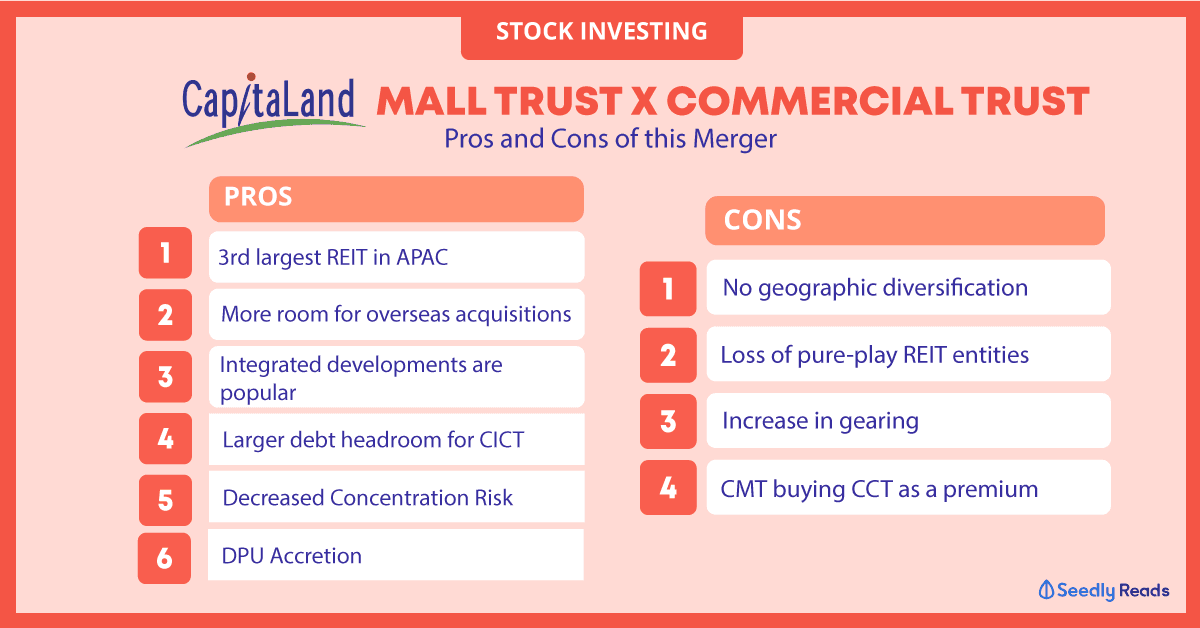

1. Creation of the third-largest REIT in the Asia Pacific region

Bigger is always better when it comes to negotiations and financial clout.

This is especially so in the REIT space after witnessing three REIT mergers last year. Larger REITs have more bargaining room for better deals and on more favourable terms. If the merger is approved, CICT will be the largest REIT in Singapore and third largest in Asia-Pacific.

CICT’s larger size will, hopefully, attract fund flows and higher liquidity, leading to potential positive re-rating and an increase in its share price post-merger.

2. More room for overseas acquisitions

Assuming a 20% overseas exposure, CICT can undertake overseas acquisitions of up to S$4.6 billion.

This is important as CICT will still be predominantly Singapore-focused (96%) after the merger. The aim is to grow the overseas portion to the target of 20%.

3. The popularity of integrated developments

The merger will lead to an integrated REIT featuring both office and retail components.

This is in line with future real estate trends that focus more on integrated developments as they offer a venue for both work and play.

Two recent examples are Funan and CapitaSpring.

The former was a pure retail mall with a gross floor area of 482,000 square feet but has now been redeveloped into a retail and office development with a total gross floor area of 889,000 square feet.

This is also in line with the government’s push for more efficient land use, with many more Singapore government land sale sites earmarked for mixed-use developments rather than for single use.

4. Larger debt headroom for CICT

The funding capacity of S$2.9 billion allows CICT to undertake larger transactions that may not have been possible for either CMT or CCT alone.

This is an example where ‘bigger is better’ as a larger size allows the REIT to target larger dollar-value transactions that it would not otherwise be allowed to consider.

5. Decreased concentration risk

The net property income (NPI) contribution of CICT’s top five assets decreases to 43%, versus 51% for CMT and 83% for CCT.

This reduction is important as it means that unitholders of CICT will be less exposed to the risk of tenant concentration, though 43% still represents a fairly large portion of the merged entity. For CCT unitholders, the risk that they use to face (at 83%) has been dramatically reduced by almost half once they become unitholders of CICT.

6. Distribution per unit (DPU) accretion

For CMT unitholders, there will be a DPU accretion of 1.6% to pro-forma FY2019 DPU, from 11.97 cents to 12.17 cents. For CCT unitholders, the DPU accretion is even greater at 6.5%, from 8.88 cents to 9.46 cents.

Negatives of the Merger

As with every transaction, there will be some negatives, so here are some of the cons of the CMT-CCT merger.

1. No improvement in geographic diversification

Though the merged CICT has reduced its tenant concentration risk as stated above.

There is still significant geographic concentration within Singapore, as it makes up 96% of CICT’s property value.

Contrast this with the most recent announced merger of Frasers Logistics & Industrial Trust (FLT) and Frasers Commercial Trust (FCOT).

FLT originally owned properties in Australia, Germany, and the Netherlands, but the merger increased its geographic exposure to Singapore and the UK as FCOT has exposure to these regions.

2. Loss of pure-play REIT entities

Unitholders who were happy holding onto ‘pure-play’ retail or commercial REITs now must contend with a merged entity containing both asset classes.

This grouse was brought up by some of my friends and peers who remarked that they either wanted to own a retail or a commercial REIT, but now had to own a merged REIT with both retail and commercial features.

They did not view this as a positive aspect as they preferred a clear delineation for the REITs they own.

3. An increase in gearing

Leverage will increase post-deal for CICT to 38.3% (assuming the draw-down of S$1.02 billion by CMT to fund the cash consideration and transaction costs).

This is an increase from 35.1% for CCT and 32.9% for CMT (as of 31 December 2019).

Though the total debt headroom has increased in dollar-value terms, it’s strange that the combined entity’s gearing has actually increased and is now closer to the regulatory limit of 45% than before.

4. CMT buying CCT at a premium

CMT unitholders will be paying a total of S$2.1238 for each unit of CCT.

With CCT’s FY2019 NAV of S$1.8625, CMT will be buying the units at a price to NAV of around 1.14.

This is a slight premium to what CCT is trading now at S$2.06 (at 31 January 2020), implying a current P/NAV of around 1.11.

A minority of CMT unitholders may complain about coughing up a slightly higher valuation than what CCT is currently trading at in the open market.

The Fifth Perspective

Though I’ve highlighted some negative aspects of this deal, the overall benefits seem to outweigh the costs.

CICT should be able to resolve the concentration risk by adding on properties in other regions or countries over time, and the REIT managers may already be eyeing something.

The DPU accretion is also something that unitholders for both REITs can look forward to, as it represents a better return on the money they invested.

Though there may be some unhappiness arising from the slight premium that CMT will be paying, as well as the larger DPU accretion for CCT unitholders compared to CMT’s.

I believe that most unitholders would look at the bigger picture and not split hairs over the small premium paid or the higher DPU accretion for CCT versus CMT.

The deal confers positive benefits to CMT in diversifying its portfolio away from being purely retail-focused and strengthens the case for CICT to be able to grow through larger and more targeted acquisitions in the integrated developments space.

Editor’s note: if you’re interested to learn more about the merger, be sure to check out Seedly’s take on the Capitaland Mall Trust and CapitaLand Commercial Trust Merger and what it means for investors.

This article first appeared on The Fifth Person and is part of a content syndication agreement between The Fifth Person and Seedly.

For our Stocks Investing and Stocks Analysis articles, the Seedly team worked closely with The Fifth Person, who is an expert in the field to curate unbiased, non-sponsored content to add value back to our readers.

The Fifth Person believes in spreading a message – that sound investment knowledge, financial literacy and intelligent money habits can help millions of people around the world achieve financial security, freedom, and lead better lives for themselves and their loved ones.

If you have any questions regarding investments, feel free to discuss them with the friendly SeedlyCommunity.

Advertisement