When I first graduated, the Central Provident Fund (CPF) was one of the most important topics for me to understand regarding financial planning.

Being one of the core pillars of my retirement planning, I knew I had to master this topic to better plan for my own future.

And it can be very confusing with so many different CPF terms and schemes…

What can I say? Adulting is tough.

Don’t worry if you’re having trouble navigating this confusing adult maze because we’ve got you!

Since we’ve previously touched on CPF interest rates, CPF LIFE, or even how the government manages our CPF money…

Today, we’ll be looking at CPF contribution and allocation rates.

Disclaimer: This is not a sponsored article. The opinions expressed here are based on our understanding of existing CPF policies. Please do your diligence and check with CPF to clarify your questions before doing anything!

TL;DR: CPF Contribution & Allocation Rates in 2024

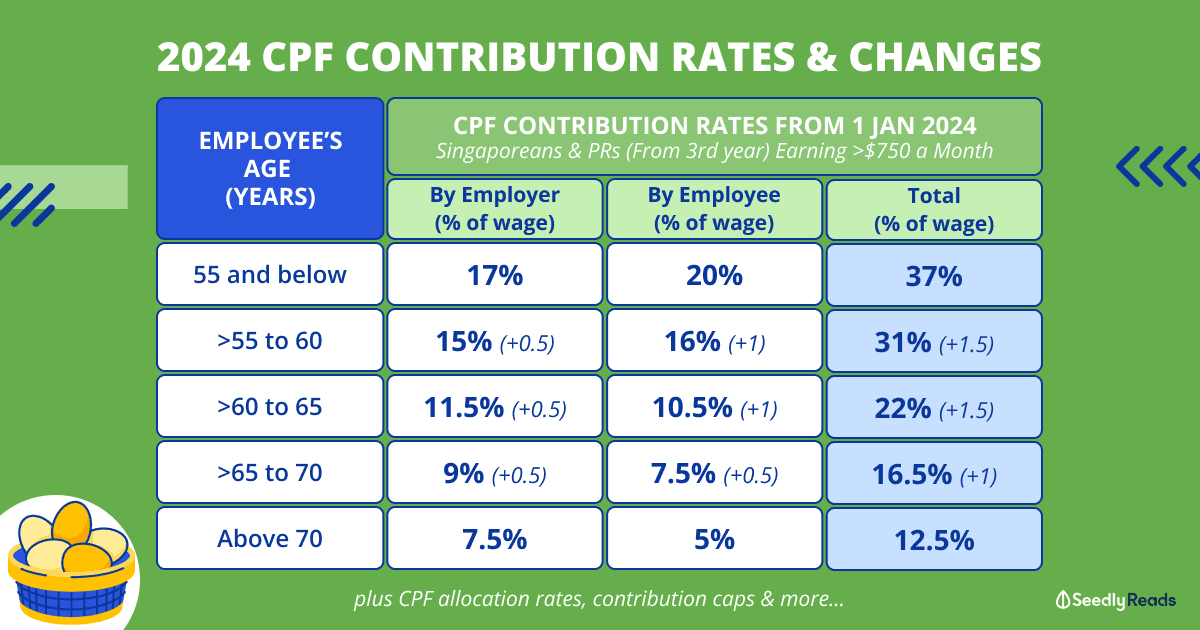

According to CPF, here are the latest CPF contribution and allocation rates for Singapore Citizens (SCs) and Singapore Permanent Residents [(SPRs) from the third year onwards] earning more than $750 a month:

CPF Contribution Rates

Singaporeans & PRs (From 3rd year) Earning >$750 a Month

(From 1 Jan 2024)Allocation Rates (% of Total Wages)

Age

(Years)Employer's Contribution Employee's Contribution Total Ordinary Account Special Account Medisave Account

≤35 17 20 37 23 6 8

>35 - 45 21 7 9

>45 - 50 19 8 10

>50 - 55 15 11.5 10.5

>55 - 60 15

(+0.5)16

(+1)31

(+1.5)12 8.5 10.5

>60 - 65 11.5

(+0.5)10.5

(+1)22

(+1.5)3.5 8 10.5

>65 - 70 9

(+0.5)7.5

(+0.5)16.5

(+1)1 5 10.5

>70 7.5 5 12.5 1 1 10.5

Note: The CPF allocation is first computed for the MediSave Account, followed by the Special Account. The remainder will be allocated to the Ordinary Account.

Click here to jump:

- What are the CPF contribution and allocation rates?

- What is the minimum salary for CPF contribution?

- Do Self-Employed Persons need to contribute to CPF?

- CPF Contribution Cap and Max CPF Contribution

What Are The CPF Contribution & Allocation Rates?

Before we begin, let’s start from the basics.

As long as you’re an employed working adult (i.e. a salaried employee), you’ll be required to contribute to your CPF account.

CPF contribution rates refer to the percentage of wages that you and your employer have to contribute toward your CPF account.

Both employer and employee contributions will be paid to your CPF accounts.

Your CPF contributions are distributed to your Ordinary Account (OA), Special Account (SA), and MediSave Account (MA) according to the CPF allocation rates.

CPF Allocation Rates From 1 Jan 2024

| Employee’s Age (Years) | Ordinary Account (Ratio of Contribution) | Special Account (Ratio of Contribution) | MediSave Account (Ratio of Contribution) |

|---|---|---|---|

| 35 & below | 0.6217 | 0.1621 | 0.2162 |

| Above 35 – 45 | 0.5677 | 0.1891 | 0.2432 |

| Above 45 – 50 | 0.5136 | 0.2162 | 0.2702 |

| Above 50 – 55 | 0.4055 | 0.3108 | 0.2837 |

| Above 55 – 60 | 0.3872 | 0.2741 | 0.3387 |

| Above 60 – 65 | 0.1592 | 0.3636 | 0.4772 |

| Above 65 – 70 | 0.0607 | 0.303 | 0.6363 |

| Above 70 | 0.08 | 0.08 | 0.84 |

Source: CPF | CPF Allocation Rates from 1 January 2024 Private Sector / Non-Pensionable Employees (Ministries, Statutory Bodies & Aided Schools)

Note: The CPF allocation is first computed for the MediSave Account, followed by the Special Account. The remainder will be allocated to the Ordinary Account.

Confused by the ratios?

Example of CPF Allocation to the Three CPF Accounts

Let’s take the example of Calmond, a 30-year-old employee and working adult.

If the CPF contribution of an employee (30 years old) is $100, the allocation of his CPF contribution will be computed as:

- Employee’s Age (Years): 35 and below

- Total CPF Contribution Amount: $100

- MediSave Account: $21.62 ($100 x 0.2162).

- Special Account: $16.21 ($100 x 0.1621)

- Ordinary Account: $62.17 ($100 – $21.62 – $16.21)

CPF Contribution Rates (2024): Minimum Salary for CPF Contribution

In total, there are five categories for CPF contribution rates:

- SCs and PRs (third year onwards) who earn ≥$750 a month

- SCs and PRs (third year onwards) who earn <$750 a month

- Self-employed persons (SEPs)

- SPR (first year)

- SPR (second year).

But as most people would fall under the first three categories, we would not cover the CPF contribution rates for the first-year and second-year SPRs. But, you can read all their CPF contribution rates here.

CPF Contribution and Allocation Rates For Singapore Citizens and Permanent Residents Earning ≥$750 a Month

These are the current contribution and allocation rates across different age groups for the first category of people:

CPF Contribution Rates

Singaporeans & PRs (From 3rd year) Earning >$750 a Month

(From 1 Jan 2024)Allocation Rates (% of Total Wages)

Age

(Years)Employer's Contribution Employee's Contribution Total Ordinary Account Special Account Medisave Account

≤35 17 20 37 23 6 8

>35 - 45 21 7 9

>45 - 50 19 8 10

>50 - 55 15 11.5 10.5

>55 - 60 15

(+0.5)16

(+1)31

(+1.5)12 8.5 10.5

>60 - 65 11.5

(+0.5)10.5

(+1)22

(+1.5)3.5 8 10.5

>65 - 70 9

(+0.5)7.5

(+0.5)16.5

(+1)1 5 10.5

>70 7.5 5 12.5 1 1 10.5

Source: CPF

The table above shows that CPF contribution and allocation rates would vary across different age groups.

Along with the adjustments to the retirement age, CPF contribution rates will also be raised gradually over the years for older workers in tandem with the ageing workforce.

CPF Contribution and Allocation Rates For Singapore Citizens and Permanent Residents Earning <$750 a Month

| Employee’s Age (Years) |

Employee’s total wages for the calendar month |

Total CPF contributions (Employer’s & Employee’s share) |

Employee’s share of CPF contributions |

|

55 & below

|

$50 or less | Nil | Nil |

| > $50 to $500 | 4% (TW) | Nil | |

| > $500 to $750 | 4% (TW) + 0.15 (TW – $500) | 0.15 (TW – $500) | |

| > $750 | [9% (OW)]* + 9% (AW) * Max. of $612 |

[5% (OW)]* + 5% (AW) * Max. of $340 |

|

|

Above 55 – 60

|

$50 or less | Nil | Nil |

| > $50 to $500 | 4% (TW) | Nil | |

| > $500 to $750 | 4% (TW) + 0.15 (TW – $500) | 0.15 (TW – $500) | |

| > $750 | [9% (OW)]* + 9% (AW) * Max. of $612 |

[5% (OW)]* + 5% (AW) * Max. of $340 |

|

| Above 60 – 65 | $50 or less | Nil | Nil |

| > $50 to $500 | 3.5% (TW) | Nil | |

| > $500 to $750 | 3.5% (TW) + 0.15 (TW – $500) | 0.15 (TW – $500) | |

| > $750 | [8.5% (OW)]* + 8.5% (AW) * Max. of $578 |

[5% (OW)]* + 5% (AW) * Max. of $340 |

|

|

Above 65

|

$50 or less | Nil | Nil |

| > $50 to $500 | 3.5% (TW) | Nil | |

| > $500 to $750 | 3.5% (TW) + 0.15 (TW – $500) | 0.15 (TW – $500) | |

| > $750 | [8.5% (OW)]* + 8.5% (AW) * Max. of $578 |

[5% (OW)]* + 5% (AW) * Max. of $340 |

|

| Notes: For Private Sector / Non-Pensionable Employees (Statutory Bodies & Aided Schools) OW: Ordinary Wages (capped at OW Ceiling of $6,800) AW: Additional Wages TW: Total Wages = OW + AW Max: Maximum contribution on OW Steps to compute CPF contribution: 1) Compute the total CPF contribution (rounded to the nearest dollar). Cents should be dropped for an amount less than 50 cents. An amount of 50 cents and above should be treated as an additional dollar. The maximum contribution on OW is computed and rounded based on the OW ceiling. If there is AW in the same month, the CPF contributions are to be computed based on total wages (OW + AW) subject to CPF before applying the rounding rules. 2) Compute the employee’s share of CPF contribution (cents should be dropped). 3) Employer’s share = Total contribution – Employee’s share There are no changes to the graduated employer and employee rates since 1 January 2016. |

|||

Source: CPF Contribution Rate

CPF Contribution Calculator: How to Calculate CPF Contribution

CPF Contributions for Self-Employed Persons (SEPs)

For a self-employed person (SEP), CPF contributions are voluntary, while Medisave contributions are compulsory.

Any self-employed persons who are Singapore Citizens or Permanent Residents and earn an annual Net Trade Income (NTI) of more than $6,000 would need to contribute to MediSave.

The MediSave contribution rates for SEPs are as follows:

| Yearly Net Trade Income | Age as at 1 Jan 2022 | |||

|---|---|---|---|---|

| Below 35 | 35 to below 45 | 45 to below 50 years | 50 years and above | |

| Above $6,000 to $12,000 | 4% | 4.5% | 5% | 5.25% |

| Above $12,000 to $18,000 | 4% to 8% | 4.5% to 9% | 5% to 10% | 5.25% to 10.5% |

| Above $18,000 | 8% | 9% | 10% | 10.5% |

| Maximum | $5,760 | $6,480 | $7,200 | $7,560 |

Example: 37 year-old with a net trade income of $65,000 in 2022

| Age as at 1 Jan 2022 | 37 years old |

| Net Trade Income in 2022 | $65,000 |

| MediSave Contribution Rate | 9% |

| Maximum Cap for Age Group | $6,480 |

| Amount of MediSave Contribution Payable | $5,850 Lower of $6,480 or (9% x $65,000) |

Alternatively, you can use this Self-Employed MediSave Contribution Calculator to calculate the amount of MediSave you need to contribute.

CPF contributions to the other CPF accounts for self-employed persons can be made via the following methods:

- Cash top-ups to all three accounts (CPF OA, SA, and MA)

- Transfer CPF OA to CPF SA or RA

- Cash top-ups via the Retirement Sum Topping-Up Scheme (RSTU).

CPF Contribution Cap and Max CPF Contribution

In addition, there is a cap on the CPF amount employers and employees can contribute:

There are mainly three CPF limits to take note of.

Ordinary Wage (OW) Ceiling

Ordinary Wages (OW) exclusively refers to employees’ wages in return for their employment in a month.

The OW ceiling, which is currently $6,800, is a cap on employees’ CPF contributions in a calendar month and will be gradually increased in four phases to $8,000 by 2026 as follows:

Additional Wage (AW) Ceiling

Additional wages (AW) are the compensation given to employees made at intervals of more than a month. This would include your bonuses, commissions, allowances, leave pay, and other forms of compensation given at intervals of more than a month. The AW ceiling is a cap on the amount of AW that attracts CPF contributions on a per-employer per calendar year basis.

The AW ceiling is currently:

$102,000* – total OW that is subject to CPF for the year

*Equivalent to 17 months x Ordinary Wage ceiling of $6,000

CPF Annual Limit

This is the maximum amount of mandatory and voluntary contributions CPF members can make to their Ordinary Accounts (OA), Special Accounts (SA), and Medisave Accounts (MA) in a calendar year.

The CPF Annual limit is currently $37,740. As the name suggests, this limit is per calendar year.

Note: The maximum amount you can voluntarily top up to your three CPF accounts is the difference between the CPF Annual Limit of $37,740 and the mandatory CPF contributions made for the calendar year.

CPF Working for More Than One Employer

If you are all about the hustle and work for more than one employer, take heart, as all your employers are required to pay CPF contributions based on the wages payable to you. This is due to the fact that the OW celing of $6,800 a month works on a ‘per employment basis‘. In other words, your employer will need to pay their employer’s share of CPF contributions even if the total pay you receive a month from all your jobs exceeds the OW ceiling.

For example, you earn $6,000 a month at two separate jobs. Even though you earn $12,000 a month from both jobs, you will still receive Employer CPF contributions on the full $12,000 a month salary from both jobs, as each individual job’s salary does not exceed the OW ceiling.

But if your total OW from all your employers from multiple jobs is higher than the prevailing OW ceiling, you can actually apply to limit your employee CPF contributions.

Read more:

- CPF LIFE VS Retirement Sum Scheme (RSS): Which One Are You On? What’s the Difference?

- CPF Investment Guide: Ultimate Compilation of CPF Investment Scheme Investment Products (OA + SA)

- CPF Matched Retirement Savings Scheme (MRSS): Get Dollar-To-Dollar Matching for Cash Top-Ups

Got Any Questions About CPF?

Feeling lost about CPF?

Fret not!

You can start with our own Seedly’s Ultimate Guide to CPF:

Or if you do have any burning questions, just hop on over to get them answered!

Related Articles:

Advertisement