DBS, OCBC and UOB: How Did They Perform in the 2021 Third-Quarter?

Sudhan P

Sudhan P●

DBS, OCBC and UOB Financial Performance

Financial updates for the 2021 third-quarter (three months ended 30 September 2021) from Singapore’s listed banks have been filed with the Singapore Exchange.

For the uninitiated, those banks are — DBS Group Holdings Ltd (SGX: D05), Oversea-Chinese Banking Corporation Limited (SGX: O39) and United Overseas Bank Ltd (SGX: U11).

The banks, which make up around 43% of the Straits Times Index, are certainly recovering from the economic headwinds brought about by the COVID-19 pandemic.

Here’s a closer look at how the Singapore banking giants performed financially in the third quarter of 2021.

DBS, OCBC and UOB: How Did They Perform in 3Q 2021?

Despite ongoing challenges such as global supply chain disruptions, inflation fears, and COVID-19 virus resurgence, the three local banks posted better financial performance.

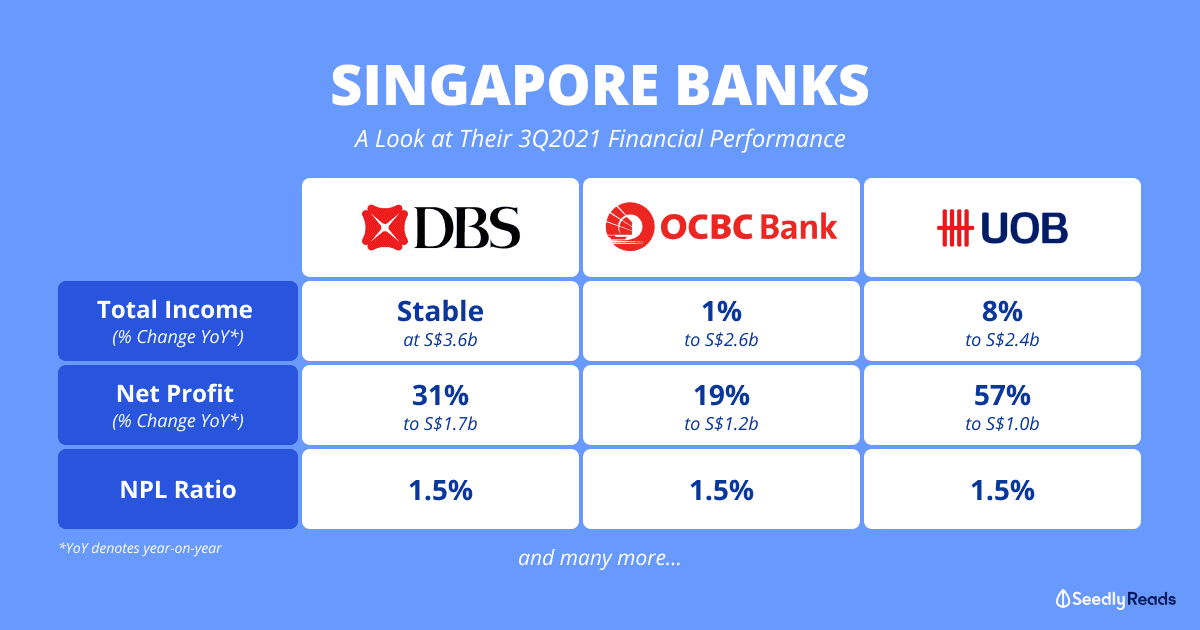

Singapore’s biggest bank DBS saw its 2021 third-quarter net profit increase by 31% to S$1.7 billion, up from S$1.3 billion a year ago.

Stable total income and resilient asset quality helped to improve DBS’ business.

Overall, the three Singapore-listed banks continued to march on strongly, building on the momentum seen over the past few quarters.

DBS OCBC UOB

Figure Change year-on-year (YoY) Figure Change year-on-year (YoY) Figure Change year-on-year (YoY)

Total income S$3,561 million - S$2,560 million 1% S$2,453 million 8%

Profit before allowances S$1,893 million -7% S$1,372 million -5% S$1,381 million 10%

Net profit S$1,700 million 31% S$1,224 million 19% S$1,046 million 57%

Net asset value per share S$21.43 7% S$11.28 7% S$23.56 5%

Net interest margin (NIM) 1.43% -0.1 percentage point 1.52% -0.02 percentage point 1.55% -0.02 percentage point

Return on equity 12.1% 2.1 percentage points 9.5% 0.8 percentage point 10.4% 3.5 percentage points

Non-performing loan (NPL) ratio 1.5% 0.1 percentage point 1.5% 0.1 percentage point 1.5% -

Common Equity Tier 1 capital adequacy ratio 14.5% 0.6 percentage point 15.5% 1.1 percentage points 13.5% -0.05 percentage point

DBS, OCBC, and UOB recorded strong earnings growth mainly due to lower credit allowances.

In particular, UOB emerged as the best-performing bank.

UOB’s bottom-line surged 57% year-on-year to S$1.0 billion compared to a year ago figure of S$668 million.

All three banks also saw stability in their non-performing loan (NPL) ratios.

The NPL ratio compares the amount of loan which borrowers are unable to pay off interest or the principal amount to the total loan book.

DBS, OCBC, and UOB continued to maintain robust Common Equity Tier 1 capital adequacy ratios of at least 13%, which were double that of the regulatory limit of 6.5%.

This ratio is a critical measure of a bank’s financial strength.

It is encouraging to see the banking trio improve their return on equity (ROE) on a yearly basis.

The ROE ratio shows how effective a bank’s management is in maximising the profits earned from shareholders’ capital.

DBS came out on top with an ROE ratio of 12.1%, up from 10% in the previous year.

In terms of net interest margin (NIM), UOB was again the best-performing bank with a figure of 1.55%.

The NIM is the average interest margin that a bank earns from its borrowing and lending activities.

DBS is the only bank that pays a quarterly dividend, and it declared an interim dividend of 33 cents per share, up from 18 cents per share in the 2020-third quarter period.

The scrip dividend scheme will not be applied to DBS’ 2021 third-quarter interim dividend.

The bank will go ex-dividend on 12 November 2021 while the payment date for the dividend will be on 26 November 2021.

In July last year, the banks had to curb their dividend payout after the Monetary Authority of Singapore (MAS) called on the local banks to cap their total dividends per share for 2020 at 60% of 2019’s dividends.

But on 28 July 2021, the Singapore central bank lifted the dividend restrictions on local banks and finance companies.

The MAS said in a media release then that the global economic outlook has since improved.

This is indeed the case as seen from the banks’ latest earnings results.

To wrap things up, let’s hear what OCBC’s group chief executive Helen Wong has to say about her bank’s 2021 third-quarter financial performance:

“Our third quarter results were resilient, despite the challenging conditions associated with the Delta virus variant. This quarter, the momentum across our banking, wealth management and insurance business has continued to grow, as reflected by loan, net new money, fee and insurance sales growth. … Asset quality is stabilising as the economic situation improves and we remain committed to supporting our customers to tide over this difficult period.”

She added that OCBC remains “positive on the long-term outlook but are watchful of the near-term headwinds from the pandemic”.

Have Burning Questions Surrounding The Stock Market?

You can participate in the lively discussion regarding stocks here at Seedly and get your questions answered right away!

Disclaimer: The information provided by Seedly serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any stock. The writer doesn’t own shares in any companies mentioned.

Advertisement