Many students are knee-deep in study loan even before getting their first pay cheque. This usually gives rise to a list of new questions:

- How should I start clearing my education loan as fast as possible?

- Should I still be investing while focusing on clearing my debt?

Most graduates find themselves at a loss when shouldering the burden of their student loan. But one thing’s for sure: The longer one takes to repay his education loan, more interest will be incurred, and one will end up paying more.

Here’s a step-by-step guide to help you kick off your journey to being free from your education debt.

Know How Much You Need

Step 1: How Much You Need To Survive Monthly

The transition from studying to the working world can be a big step, but one can still roughly calculate his expenses. When with the burden of a loan, every dollar counts. Come out with a calculation of your monthly expenses and stick to it!

Make use of tools such as www.mytransport.sg to help you with your calculation. Also, reduce the cost of your mobile plan. The trick here is to be lean.

Make use of tools such as www.mytransport.sg to help you with your calculation. Also, reduce the cost of your mobile plan. The trick here is to be lean.

Step 2: Portion Your Starting Salary

Congratulations! Assuming you managed to secure yourself a job, the first step towards clearing your debt will be to recognise the amount of money you can work around with.

To do so, a few minor calculation is required. In the below example, we will be using a fresh graduate with a $2.5k starting pay to illustrate the calculations.

Now, split your take-home pay into 3 portions using the 50/30/20 rule. The three main accounts are basically for your needs, investing and savings.

Now, split your take-home pay into 3 portions using the 50/30/20 rule. The three main accounts are basically for your needs, investing and savings. Now that you have all these numbers, find out how much you have to pay off your loan monthly using the below method:

Now that you have all these numbers, find out how much you have to pay off your loan monthly using the below method:

Step 3: Run Scenarios For Your Student Loan

How do you eat an elephant? One bite at a time.

Before rushing into any decision, find out the 3 main at the numbers involving your student loan:

- How much is the loan in total?

- What is the interest rate?

- What is the minimum monthly payment?

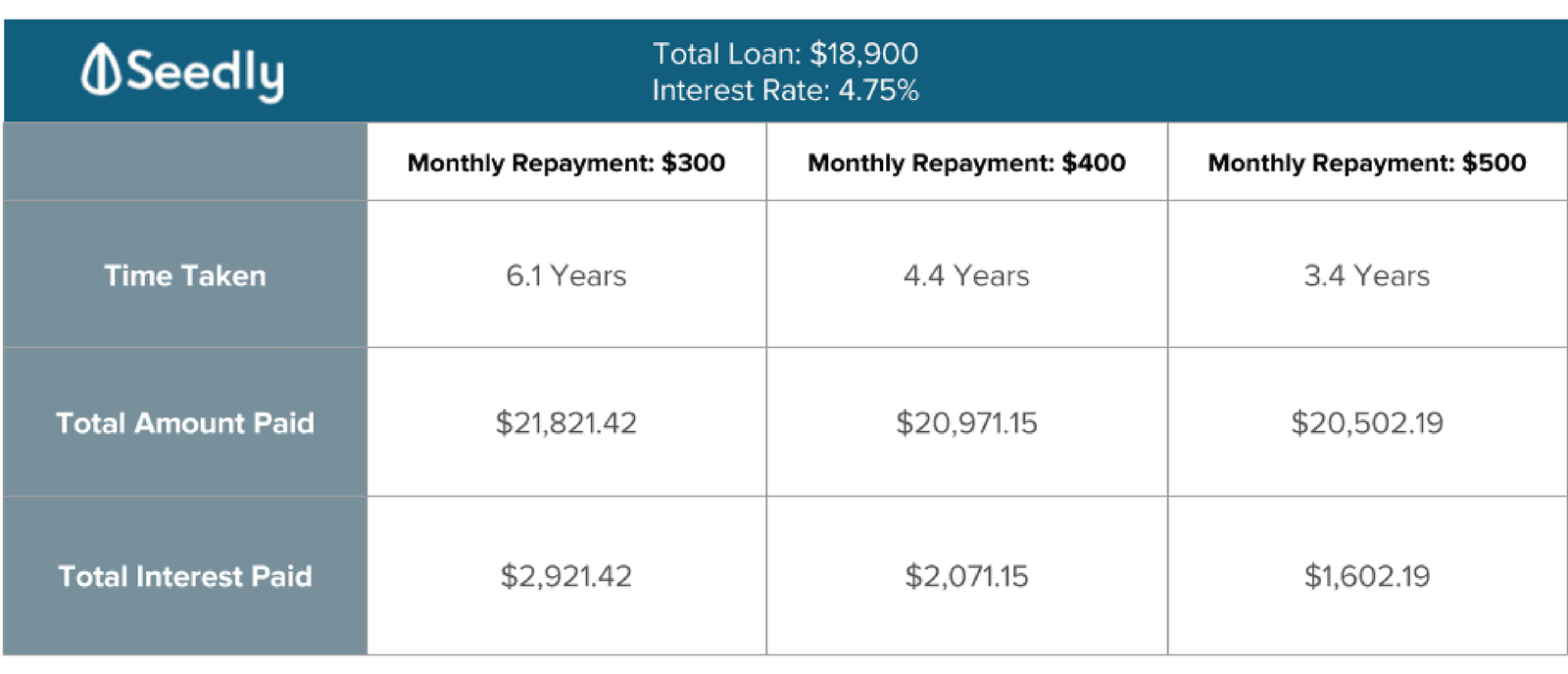

We use an example of a Tuition Fee Loan of $18,900 with interest rate at 4.75% per annum. The monthly repayment is at $100.

Simply run this through a Loan Repayment Period Calculator and you will notice why it makes sense to clear your loan as soon as possible to reduce total interest paid.

Now set a target and work towards it. Do not worry if your repayment amount from “your needs” account is not enough, we will guide you to unlock more money further down the article.

Now set a target and work towards it. Do not worry if your repayment amount from “your needs” account is not enough, we will guide you to unlock more money further down the article.

Safety Net

It is always important to get your safety net up before channelling the rest of your money to your monthly repayment of loans.

Your safety net will be made up of 2 components, your insurance and your emergency fund.

Step 4: Health Insurance

Always get yourself insured first, to kick off your financial planning journey. Insurance helps provide a financial support and reduce uncertainties in your life. An insurance will be the first level of your safety net. While clearing your student loan might be important, the last thing you want is to let a pile of hospital bills hinder your debt clearing process.

Step 5: 3-6 Months Emergency Fund:

Another part of your safety net will be an emergency fund of 3-6 months. Ensure that this fund is readily available so that it can be used to pay off your student monthly loan should some unforeseen circumstances occur.

Invest or Increase Monthly Repayment of Loan

You now have your safety net set up, you will make a decision on what to do with the money from the “hobby/investing” and “savings” portion of your salary.

Scenario 1: Invest

If you are ready to invest, list out the investment products you are familiar with, and planning to invest in.

From here, one can make a decision based on these factors.

The best instrument will be one with returns higher than the loan’s interest at low risk but we know that such instruments may not be available. It ultimately depends on the risk profile of the investor to form his own portfolio.

We personally believe in taking up a tiny bit of risk on instruments in an attempt to beat the loan’s interest and channel the remaining back to repaying your education loan. For every amount repaid, no matter how small the amount is, is a battle won again the interest rate set by the student loan provider.

Scenario 2: Increase Monthly Repayment of Loan

Unless you are confident of achieving a portfolio that can beat the interest rate of the loan (4.75% in the above example), you can reward yourself a little before using the rest to repay the loan.

Pamper yourself once in a while to give yourself a little morale boost in this tough journey to being education loan free!

Conclusion- Set up your safety net ASAP

Most fresh graduates tend to dive into clearing their loan without a structure or a plan in mind. We can’t emphasise enough on the importance of having your safety net set up. It provides one with the freedom to channel as much of his salary into his personal investment or to increase repayment of his loans.

Advertisement