Triple Threat: How to Avoid Getting Crushed by Slower Wage Growth, Higher Inflation & Interest Rates

Joel Koh

Joel Koh●

As a personal finance writer, I am acutely aware of the recent increases in the cost of living in Singapore. But the reality of it really hit home when I saw that the price of my favourite wanton mee at the newly refurbished coffeeshop near my place went up yet again this year.

A bowl of wanton mee that cost only $4 last year became $4.50 after the 2023 GST hike in January. The latest hike brought the price to $5.

Although the price of the wanton mee ‘only’ went up by $1 in absolute terms, this marks a 25% increase in price, which is pretty substantial.

These price increases are happening at a national level as well. If you look at the inflation numbers for February 2023, one month after the GST hike, food prices increased by 8.1% compared to a year ago:

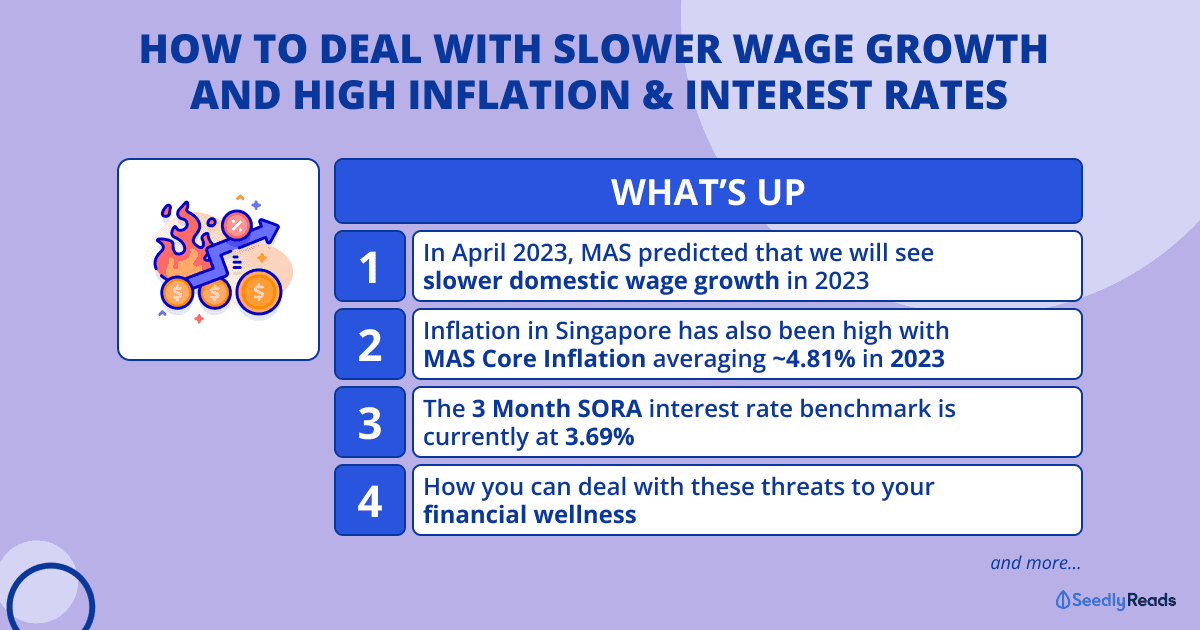

On top of high inflation, we are also contending with high interest rates and slowing wage growth, which can have a negative effect on our financial wellness.

But it’s not all doom and gloom. Here’s how to avoid getting crushed by this triple whammy of high inflation, interest rates and slow wage growth.

TL;DR: How to Avoid Getting Crushed by Slower Wage Growth, Higher Inflation & Interest Rates

The Triple Threat to Our Financial Wellness in Singapore

Before we begin, let’s take a closer look at the threats to our financial wellness in Singapore.

Slower Wage Growth

The Monetary Authority of Singapore (MAS) has forecasted in a policy statement in April that ‘domestic wage growth should also ease as labour demand moderates, especially in sectors more exposed to international trade and finance.’

FYI: If your salary is not increasing at a higher rate than inflation, you are actually taking a pay cut as things are getting more expensive.

GST Hike in 2024 + High Inflation

Speaking of inflation.

Inflation in Singapore has been trending down for the second half of 2023. But, it was still quite high for the first half of the year:

Despite it trending downwards, prices still went up by 3.80% in July 2023 from July 2022.

Higher Interest Rates

Also, high interest rates are occurring in Singapore but worldwide. Most notably, central banks like the U.S. Federal Reserve (Fed) have been raising interest rates aggressively to tame inflation. Whereas for Singapore, the Singapore Overnight Rate Average (SORA), a barometer for the country’s short-term interest rate, has also risen steeply and could remain high in this climate of high interest rates and inflation:

On top of these macroeconomic indicators, you can see the more micro effects of these three factors on the financial wellness of Singaporeans in DBS’s latest study.

DBS’ Between a Rock and a Hard Place Study

In this report, DBS analysed the aggregated and anonymised database of about 1.2 million of their non-wealth customers in May 2023*, relative to May last year, to shed light on the impact of high inflation and interest rates on their customers’ financial wellness.

*Excludes non-wealth salary-crediting customers like work permit holders.

After diving into the report, here are some key findings that I found interesting:

- Boomers and low-income customers saw worsening wallet bandwidth: Contrary to other customers, both groups saw expense-to-income ratios inch up to 86% and 93%, respectively, as expenses grew 5.5x and 1.2x faster than that of income.

- Savings dipped but remained healthy, except for the low income: The median customer saw their savings decline marginally from 3.7 to 3.5 months of expenses. Yet, savings for low-income customers could only last them 1.5 months, which may be concerning.

- Gig workers are the most financially stretched: Their expense-to-income ratio of 112% in May 2023 was significantly higher than that of the median customer. Their savings of just 1.7 months of expenses are deemed too low.

- Watch for further impact on mortgages as higher rates linger: Additional stresses could come when mortgages are refinanced on higher interest rates, as more than half of customers earning below $5,000 have mortgage loans under floating rates.

*Figure is based on individual and will be lower for a dual-income household

Unfortunately, these groups are facing some issues with high inflation and interest rates. The slowing wage growth in Singapore does not help either.

FYI: If you need help or know someone who does, check out DBS and POSB’s suite of offerings that were launched to help low-income households deal with the rising cost of living.

How to Deal With Threats to Your Financial Wellness

Let’s keep it real. These threats to your financial wellness are not new and will not go away.

Today, it might be slower wage growth, high interest rates and unemployment. Tomorrow, it may be a recession.

There’s no telling what the future will look like.

Thus, it is important to properly equip yourself to deal with any potential threats to your financial wellness and reach your financial goals with better financial planning.

A possible solution came to me when I somehow chanced upon a press release in my crowded inbox about DBS’ new and improved financial planning tool, Plan tab with digibank

For those of you already familiar with the bank’s digital financial planning tool NAV Planner, this is where it now resides.

To access the Plan tab, you can simply log in to your digibank app and click on the ‘Plan’ tab at the bottom of the navigation bar:

Once there, you can check out the enhanced features of the Plan tab on digibank. This is where you can craft your unique dashboard tailored to your life stage and aspirations.

Whether you’re planning to Save, Invest or Retire, the Plan tab on digibank has you covered:

After inputting your financial focus, the Plan tab on digibank will help you create a customised dashboard tailored to your current financial situation and show you in detail how you can get there:

You’ll enjoy a personalised view of your finances plus receive curated content, recommendations and actionable tips based on your financial focus.

That’s not all.

When life gets in the way, you can actually switch your focus anytime. Click ‘Edit your plan’ to switch to either Save, Invest, or Retire and DBS will automagically adjust the plan for you:

Source: DBS

But for now, I’ve decided to hone in on planning for my Retirement as my financial focus.

Why retirement specifically?

Well, it’s on almost everyone’s mind. According to the latest Manulife Asia Care Survey 2023, approximately 63% of participants expressed that their top financial goal is to save money for their retirement:

FYI: The survey was conducted with 1,037 Singapore respondents aged 25 to 60 years old who either own insurance or intend to buy. Respondents were surveyed between end December 2022 – early January 2023.

But an important thing to note regarding retirement is that you must account for inflation.

FYI: Inflation measures the rate at which the price levels of goods and services in the economy increase over time. This causes a decrease in the purchasing power of the currency as more money is needed to buy the same product now compared to the past.

For context, here is the CPI and MAS Core Inflation data for the past 30 years:

| Average Headline Inflation Rate (CPI All-Items) | Average Core Inflation Rate (MAS Core Inflation) |

|

|---|---|---|

| Over the last 10 years (2013 to 2023) | 1.44% | 1.65% |

| Over the last 20 years (2003 to 2023) | 2.08% | 1.86% |

| Over the last 30 years (1993 to 2023) | 1.73% | 1.67% |

Source: SmartWealth Singapore

There are other cost of living pressures like the upcoming GST hike in 2024, where GST will go up another 1% from 1 Jan 2024 to 9%. Let’s keep that in mind when looking at retirement.

How to Account For Inflation in Retirement Planning

To illustrate, I’ll refer to the latest Lee Kuan Yew School of Public Policy (LKYSPP) study about how much a family needs for a basic standard of living:

The researchers have also updated their previous study about how much the elderly need to meet their basic needs after taking into factors like inflation.

The study found that single elderly aged 65 and older in Singapore need about $1,421 monthly for their basic needs. Their budget is divided into 29.20% for basic needs like Food (Hawker food, food courts, restaurant food and non-alcoholic beverages) and 11.90% for housing-related costs.

In addition, the elderly spend about 20% on lifestyle expenses like recreation, cultural activities and holidays.

I can imagine the budget breakdown for the elderly will not be too different from the younger single people living in Singapore as they do not have to contend with the cost of raising a child in Singapore.

Let’s assume you want a simple life and retirement income of $1,500 (rounded up for simplicity). Based on the study, $1,200 a month will be spent on basic needs and $300 will be spent on wants.

Given Singapore’s headline inflation rate of 1.65% for the past 30 years, you’ll want to play it safe by rounding up to a 2% inflation rate.

Now that you have an idea… set a retirement goal within digibank and see if you are on track to meet your dream retirement when you turn 63.

Here’s how you can do so!

Retirement Planning With the Plan Tab on digibank

Alongside the personalised dashboard, DBS has also made some changes to their Retire feature:

FYI: you can actually manoeuvre to the Retire Feature via the top navigation bar even if you didn’t choose Retire as your financial focus.

To illustrate how it works, I am assuming the profile of an average working Singaporean who is:

- Receiving the median income of $5,070 (including employer CPF) with a take-home pay of $3,600

- A salary rate increase of 3.30% p.a. (based on annualised changes in nominal wage data from 2015 – 2020)

- Spending $1,500 a month

- Have to contend with inflation of 2.00% p.a.

You can insert all these assumptions into the Plan tab on digibank:

It will do the heavy lifting and churn out a detailed breakdown of your projected assets at your current age, retirement age and live-till age when you turn 63, and identify gaps to plug to stay on track towards your dream retirement:

digibank Plan Tab Consideration

Full disclosure. I am a user of the Plan tab on digibank myself; I found the new features really helpful as I could easily visualise and plan how much I need for retirement with it. Plus, I am able to input multiple data points and receive an easy-to-digest output.

Not to mention that the User Interface is intuitive as well.

However, I am well aware that in exchange for this benefit, I am providing additional financial information about my cash, investments and investment risk profile via SGFinDex or other forms of input to DBS.

But on balance, DBS takes data protection very seriously. Also, US-based financial publication Global Finance has accorded DBS the ‘Safest Bank in Asia’ award for 13 consecutive years from 2009 to 2021.

Conclusion

Overall, I feel that this is a good trade-off as although slower wage growth, high inflation and high interest rates are still a thing, I’ve charted a course to tackle these financial challenges and boost my financial well-being with the Plan tab on digibank.

If you’re aiming to enhance your financial wellness as well, feel free to explore the Plan tab on digibank:

Your journey towards a brighter, financially empowered future awaits!

Read More

Advertisement