When Should You Choose Fixed Deposits over Singapore Savings Bonds (SSB)?

The classic question!

To Singapore Savings Bond, or to Fixed Deposits…

Singapore Savings Bonds (SSB) is classified as one of the lowest risk investment in Singapore, mainly due to the fact that SSBs are offered by the Singapore Government and also backed by them.

On the other hand, a fixed deposit account is also one of the safer options available to grow your money!

TL;DR – Have Both in Your Investment Portfolio

That’s right!

Instead of choosing one over the other option, you can have both fixed deposits and the Singapore Savings Bond in your portfolio.

- SSB – An amount set by your bond allocation in your investment portfolio.

- Fixed Deposits – Your emergency funds.

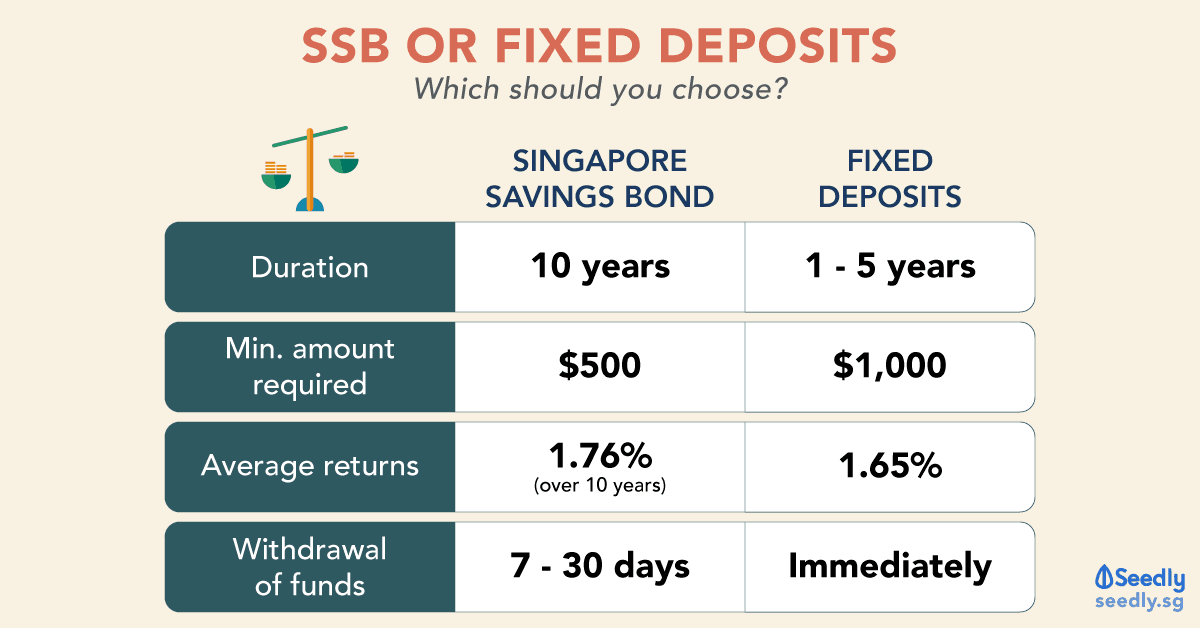

| SSB | Fixed Deposits | |

|---|---|---|

| Duration | 10 years | 1 - 5 years |

| Min. amount required | $500 | $1,000 |

| Average returns | 1.76% (over 10 years) | 1.65% (Offered by UOB) |

| Withdrawal of funds | 7 - 30 days | Immediately |

Fixed Deposits in Singapore

I did a quick search on the current Fixed Deposit rates with the lowest deposit required:

| Banks | DBS | OCBC | UOB |

|---|---|---|---|

| Interest Rate per year | 1.40% | 1.95% | 1.65% |

| Duration (Locked-in) | 1 - 5 years | 4 years | 3 years |

| Min. Deposit amount (S$) | 1,000 | 5,000 | 5,000 |

If you don’t find these rates that attractive, don’t worry, banks are constantly updating their promotional interest rates!

Singapore Savings Bonds

This Month’s SSB (January 2020)

| Year From Issue Date | Interest (%) | Average Return Per Year (%) |

|---|---|---|

| 1 Year | 1.52 | 1.52 |

| 2 Years | 1.52 | 1.52 |

| 3 Years | 1.52 | 1.52 |

| 4 Years | 1.73 | 1.57 |

| 5 Years | 1.82 | 1.62 |

| 6 Years | 1.82 | 1.65 |

| 7 Years | 1.86 | 1.68 |

| 8 Years | 1.92 | 1.71 |

| 9 Years | 1.98 | 1.74 |

| 10 Years | 2.04 | 1.76 |

The average interest rate for SSB would be 1.76%.

Now, if you need to cash out your SSB, having invested $10,000, at the end of your third year, the interest that you have earned on average is 1.52% p.a. which amounts up to $456.

SSB VS Fixed Deposits

| SSB | Fixed Deposits | |

|---|---|---|

| Duration | 10 years | 1 - 5 years |

| Min. amount required | $500 | $1,000 |

| Average returns | 1.76% (over 10 years) | 1.65% (Offered by UOB) |

| Withdrawal of funds | 7 - 30 days | Immediately |

Using the Fixed Deposit rates offered by UOB above at 1.65% for 3 years, your $10,000 would have earned you an additional $503.21 on interest instead.

That is an opportunity cost of $47.21, that is about 9% (9.38%) on your potential return if you have chosen the Fixed Deposit.

Other Products Similar to the SSB

There are other products similar to SSB,

- Short-term endowment plans

- High interest yielding savings account

| Products | Investment Horizon | Flexibility | Returns |

|---|---|---|---|

| Singapore Savings Bond (SSB) | Long / 10 years | Yes | Around 1.7% |

| Short Term Endowment (e.g. HSBC, NTUC Income, FWD and Great Eastern) | Short / 3 years | No | Around 2% |

| CIMB Fast Saver (Savings Account) | None | Yes | 1% |

Since there’s liquidity restriction with short-term endowment plans, I feel that opening a high interest yielding savings account would be a better option, even though some of them have specific requirements.

Since there’s liquidity restriction with short-term endowment plans, I feel that opening a high interest yielding savings account would be a better option, even though some of them have specific requirements.

When Should You Choose One Over the Other?

Whenever this topic gets discussed in our Seedly Community, the majority of us would choose to place our money in SSB over FD. With only a handful of people, would opt for the latter.

Choosing Fixed Deposits

When you need to withdraw the money immediately.

- Fixed Deposits allows you to withdraw your money immediately.

- SSB requires about 7-30 days to withdraw your money.

When you have a big amount, amount big enough that you are able to negotiate with the bank a higher fixed deposit rate.

- The maximum amount of SSB you can hold is $200K across all SSB issues.

- For SSB, you might not be allocated the entire amount you opted for.

– Meaning, although you have opted for $10,000 SSB, you might receive only $6,000 worth of SSB allocation. - There is no limit to how much you can hold in Fixed Deposits – however, only $75,000 of your deposit is covered under SDIC.

In the event a Deposit Insurance Scheme member bank or finance company fails, all of your eligible accounts with that member are aggregated and insured up to S$75,000. Trust and client accounts held by non-bank depositors are insured up to $75,000 per account.

Choosing Singapore Savings Bonds

Due to bonds having an inverse relationship with market interest rates, the interest rates offered by the SSB every month are irregular, and because of that sometimes you might feel “short-changed” by your investments.

There are a few ways that you can hack your SSB investments like withdrawing your existing SSB investment to invest in the current month’s SSB if the interest rate offered is higher.

With liquidity being the only disadvantage when it comes to investing the Singapore Saving Bonds, you should have set aside at least 6 months worth of your salary as emergency funds before embarking on your investment journey.

The SSB x FD Strategy

Answering to the title, I feel that you should not choose one over the other but have both in your portfolio working hand in hand.

How much to place in your Fixed Deposit?

- 6 months worth of your salary = Your Emergency Fund

In any case of an emergency, you are able to withdraw your emergency fund immediately whenever you need them. If you don’t need them, you get to enjoy higher interest on your deposit.

If you have a high interest yielding savings account like DBS Multiplier, OCBC 360, UOB One etc., you may use them as well to hold your emergency fund to earn yourself that additional interest!

How much to place in Singapore Savings Bond?

- The percentage set by yourself to hold bonds in your investment portfolio.

It depends if you are a risk-averse investor or an aggressive investor. - With SSB being an almost risk-free form of investment here in Singapore, it is your choice how much SSB you would like to hold in your investment portfolio to balance them out.

Advertisement