Is Grab Becoming a Super App? Exciting New Features We Can Expect as Grab Users

Xue Miao

Xue Miao●

Similar to the word ‘Google’, the word ‘Grab‘ is so present in our lives that it has become a transitive verb instead of a noun.

We now often use phrases like “Wanna grab later?” when we use its ride-hailing services.

Or “Shall we grabfood?” for food delivery.

We also saw Asia’s first numberless Grabpay card, and also new Grab subscription packages.

With a full suite of services under its belt, Grab is still looking to expand its line of products and services.

With that, they have recently announced some exciting new features that we can expect in the upcoming months.

Disclaimer: This is not a sponsored article. We are writing this to inform our readers about the upcoming changes.

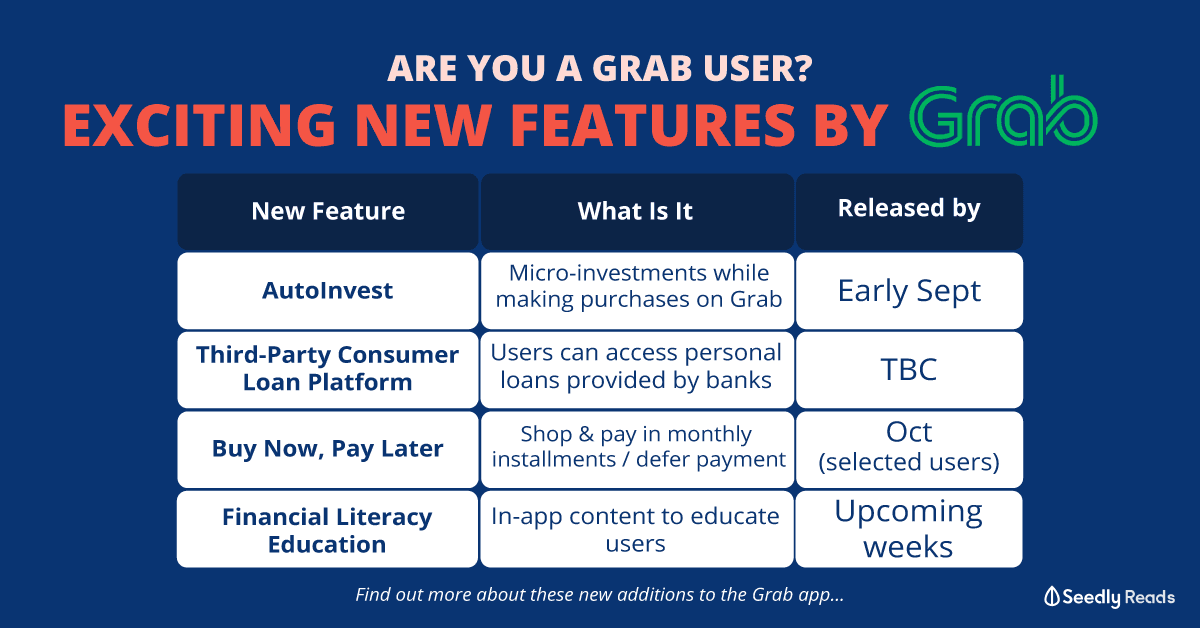

TL;DR: Exciting New Features to Expect on the Grab App

| New Feature | What is it | When is it released? |

|---|---|---|

| AutoInvest | Micro-investments while making purchases on the Grab app | Early September |

| Third-Party Consumer Loan Platform | Users can access to different personal loans provided by licensed banks | TBC after list of bank partners are finalised |

| Buy Now, Pay Later service | Users to shop online and pay in interest-free monthly instalments, or defer payment to following month | October to selected groups |

| Financial Literacy Education | In-app content to help users make smarter financial decisions | In the upcoming few weeks |

1. AutoInvest – Micro-invest while spending on Grab

The Grab Financial Group (GFC) will be launching AutoInvest, which is touted as a micro-investment product.

Through this product, the team hopes to make retail wealth solutions more accessible and easy to understand.

Grab users would get to do ‘micro-investments’ whenever they make eligible transactions on the app.

This means that we can ‘invest-as-we-spend’ as we complete our Grabfood or Grab ride transaction, by setting aside small amounts (starting from $1) in our Grab wallets.

This is entirely optional for Grab users, mainly for those who wish to invest in small amounts of money while transacting on the platform.

This money would be invested into fixed-income funds offered by Fullerton Fund Management and UOB Asset Management.

The return is estimated to be at 1.8% p.a..

BUT.

It is important to note that both the capital and returns are not guaranteed, not protected by SDIC.

In addition, there would be fees charged for fund management, which would be slightly below 0.45% (will be reflected in-app).

Can this potentially replace your investments?

Personally, I don’t think so.

As this product does have an investment element and invests only in highly liquid short-term instruments, it behaves similarly to that of a cash management account .

As mentioned above, it is a nice option for users who would like a low barrier of entry to investment products.

The funds are also highly liquid, where users can withdraw the sum anytime into the Grab e-wallets, which can be used on any Grab merchants or places that accept the GrabPay card (which is anywhere that accepts Mastercard).

There will be no hidden or transaction fees.

2. Supporting Third-Party Consumer Loans

Grab will be partnering bank institutions to provide licensed loans to users.

This is after Grab’s expansion of loan offerings to merchants and micro-entrepreneurs earlier last year.

Through this, Grab aims to shift users away from existing loan distribution platforms, by becoming THE platform that makes these loans accessible.

Users would be able to discover different loans through the Grab app, and conveniently access to these loans through a fully digital application.

To ensure responsible borrowing, there will be minimum requirements to be met, such as minimum income, background verifications etc.

BUT.

It is still important to note that there is still a danger of racking up high-interest debts, especially if such loans are not managed properly.

By allowing greater convenience to users, this might potentially increase the risk of bad debts.

This is especially so for an economic climate like the one we are facing right now – where people might be more tempted to taking up loans to ease short-term monetary pains.

3. Expansion of Buy Now, Pay-Later Option

Grab is also expanding their Buy Now, Pay Later option for users, where there is an option to take installments or make postpaid payments.

Eligible users will be able to make payment in interest-free monthly instalments (PayLater Instalments), or defer their payment to the following month (PayLater Postpaid).

This would be available for selected e-commerce sites, and will begin in Singapore and Malaysia in October.

This means that users can now have more flexibility in managing their cash flow, and also have a lower barrier of entry for online purchases.

BUT.

I personally feel that this might open a can of worms for users who are not the best at managing their cash flows.

While brands would love to leverage on such plans to encourage consumers to spend more, some (especially those with tight budgets) might see it as a short-term solution to purchases that are usually out of reach.

By pushing their payment further down the road, this might increase the risk of having bad debts.

This period of economic uncertainty might also increase the likelihood of such occurrences.

4. Offering Financial Literacy Education

In order to help users make smarter financial decisions, Grab is looking to launch a series of financial literacy programmes.

Since the Grab platform is offering services such as personal loans and micro-investments, financial education might come in handy to ensure that users are making responsible decisions.

This would include in-app content that aims to educate users in responsible borrowing, or help them make informed decisions on the different financial products available.

This is an exciting one, because we are also BIG on financial literacy.

With our goals at Seedly aligning with this superpower, does this mean the possibility of future Grab x Seedly collaborations? 😉

(Dearest Grab, notice us please! 👋)

What’s Next for Grab?

In my opinion, Grab seems to be becoming a Super App in Singapore, with its continuous efforts in integrating various new products and services on its platform.

Just like WeChat in China and GoJek in Indonesia, Grab’s services are allowing consumers to make various types of transactions all on ONE platform.

With Grab’s interest in looking into the digital banking space, we can expect more users to hop onto the Grab bandwagon too (building on its already huge consumer base) – if it does win the digital banking license.

Looking at these continuous efforts to deepen its roots in the fintech space, I’m sure we can look forward to more products to be rolled out in the future.

To further expand on Grab’s ecosystem, there are some things I personally hope to further experience on the Grab platform.

Things like tracking and analysing spending trends, or a wider range of investment products.

Or tracking of the supply of parking lots, or even payment of parking fees.

With more features available, there would be no doubt that the Grab app would be a formidable (and super, duper cool) app.

Advertisement