Could Grab Singapore’s Cash Advance Scheme Cause More Problems Than Solve Them?

Earlier this year, ride-hailing giant Grab quietly unrolled a scheme for selected employees – the so-called Upfront Cash Programme.

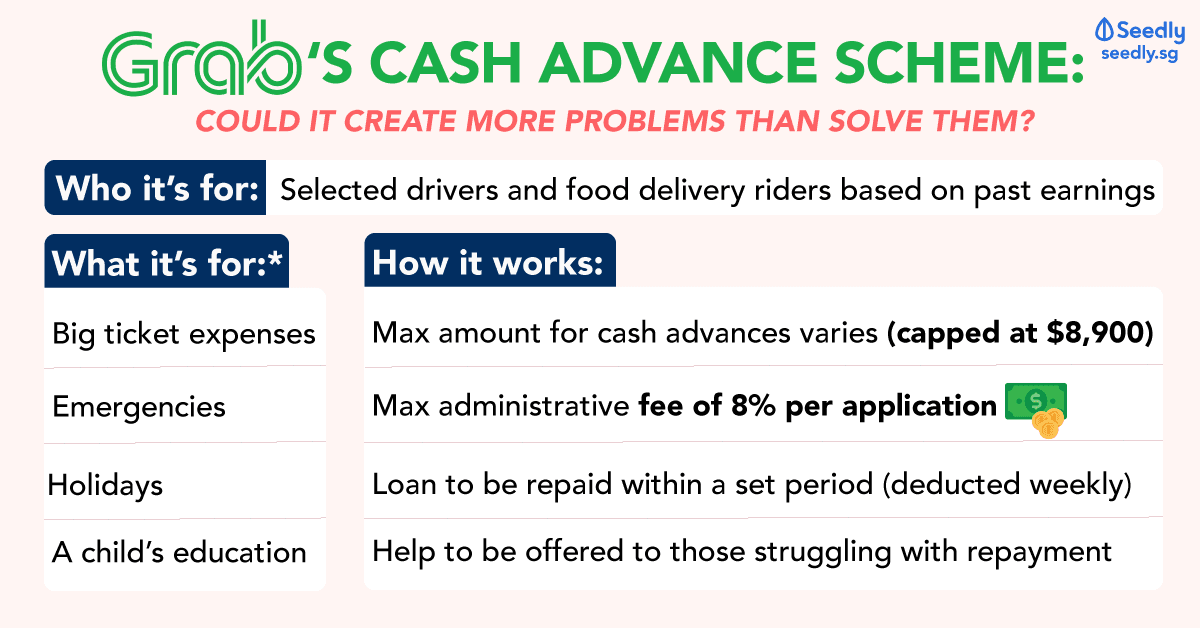

Under this, certain driver-partners and food delivery riders are offered the opportunity to take a cash advance of up to $8,900 on their salaries.

Apart from a one-time administrative fee of up to 8% per cash advance requested, there aren’t hidden fees or penalties.

Enticing as it may sound in theory, naysayers are likening it to a loan scheme, despite Grab’s insistence that it isn’t.

But let’s first lay the groundwork, by way of facts.

What Is A Cash Advance?

A cash advance is a short-term loan that is charged to your bank account. Banks offer this through credit cards, although interest rates and fees are typically higher than that of a regular credit card transaction.

Local banks charge a cash advance fee of around 5% (or $15, whichever is higher) – in addition to a minimum daily interest of 24% on the Average Percentage Rate (APR) of your loan amount.

A Money-Making Opportunity?

Unlike banks, though, Grab’s Upfront Cash Programme is only open to selected driver-partners and food delivery riders whose historical earnings are satisfactory.

These employees can then secure an advance on their projected future earnings, which must be repaid within 52 weeks.

Let’s assume Sophie – a GrabFood Delivery Rider – decides to apply for a cash advance for a family trip.

Here’s how it works exactly:

- Sophie applies for a cash advance of $8,900 (the maximum amount allowed) through the Grab Driver app. No supporting documents are required, since the scheme was offered based on her past earnings.

- The requested money is credited into her Cash Wallet, subject to a one-time administrative fee of 8% of the loan amount.* That takes her total loan amount to $9,612*.

*[$8,900 loan] + [(8% admin fee x $8,900 loan)] = $8,900 + $712 = $9,612 - Sophie transfers the $8,900 into her bank account for use.

- Under her agreement with Grab, she chooses to repay the loan within 26 weeks.** This amount is deducted once-weekly from Sophie’s earned incentives in her Cash Wallet over the agreed period. Alternatively, she can choose to place a lump sum in her Credit Wallet for auto-deduction.

**[$9,612 owed] / 26 weeks = ~$369.70/week - To fund the repayment of her loan, Sophie continues taking more jobs through the Grab Driver app.

It seems straightforward enough; bank interest rates are significantly steeper, so why not a cash advance through Grab?

The practice is hardly a new one. Companies in the United States, too, offer a similar scheme with the purported intent of easing the financial pressure off employees.

From emergencies to big ticket purchases, a salary advance seems an easy answer, given it works within a regulated framework. Yet the introduction of the programme possibly spell the beginnings of a Pandora’s box.

Fair Game

In my (admittedly pessimistic) eyes, the scheme presents employees the opportunity to take unnecessary loans, given how streamlined the application process is. It’s almost too easy to secure money, which is the point of a cash advance.

It also raises the question of how Grab hopes to benefit from the Upfront Cash Programme, or if it’s genuine in its intent to help employees enjoy “better cashflow for a better everyday” – whether for emergencies, white goods purchases or a child’s education.

At least, that’s what’s stated upfront (ha, ha) on its website.

If this is to be believed, a larger issue remains: that the company could alter its cash advance terms at any point.

Last month, a Grab driver claimed some incentives were revised shortly after his application through the Upfront Cash Programme, effectively removing some 30% of his income.

That’s because loan repayments are made through Cash Wallet deductions, which are directly earned from driver/rider incentives.

In an email to Mr Zainal Bin Sapari – the deputy chairman for the Government Parliamentary Committee for Manpower – the Grab employee expressed his unhappiness over how the changes have affected his livelihood.

The above gripe highlights the detriments of taking a cash advance through your employer – and, at its core, is a classic example of a catch-22.

Such a scheme could discourage employees from turning to predatory loans or bank loans, yet taking a payroll advance inevitably binds you to the company (and its possibly fluid terms and conditions) until you’ve repaid the full sum.

In a sense, it increases the chances of employees falling into a vicious cycle of debt and struggling to pay off a loan, particularly if they fall short of their projected incentive earnings.

On this, Grab maintains that driver-partners and delivery riders will be able to seek help on a case-by-case basis – although how exactly remains opaque.

Employees that fall in this camp won’t be able to cancel their Grab Driver Accounts until outstanding payments have been cleared, either, but do have the option of repaying the sum through the GrabApp or bank transfers.

It remains to be seen whether the Upfront Cash Programme will do more harm than good, or work in the reverse.

At time of writing, though, the Ministry of Law is looking into the scheme to determine if it requires similar regulations to licensed money-lending firms.

Advertisement