Working Adults: The Ultimate Guide To Understanding Your Endowment Plan

Insurance Savings Plan (Endowment Plan)

Commonly marketed as Insurance Savings Plan, getting an Endowment Plan are commonly being marketed to help Singaporeans save.

- A total number of 239,487 Endowment Insurance policies were sold during the year ended 31st December 2016.

- Endowment accounts for 48.8% of annual premiums in the industry for non-linked policies.

- This is despite non-linked Endowment policies only accounting for 16.2% of the number of policies sold in the year 2016.

- For linked Endowment policies, it accounts for 22.6% of linked policies sold and account for 11.4% of annual premiums.

TL;DR: Get an Endowment only after you have settled the rest of your insurance planning

- The par fund new investment returns according to Straits Times

- Always do your own due diligence when coming to returns on the Benefit Illustration (BI). The policy usually has a more optimistic approach to their portfolio’s return.

- One is recommended to look to get Endowment Policies after getting the necessary Health (Hospitalisation & surgical) and Term insurance.

This is further illustrated by our Seedly Personal Finance Community:

Basics Types Of Endowment

Endowment Policies are usually categorised into 3 different types:

| Types of Endowment | What does it mean? |

|---|---|

| Participating (par) | Upon the death of the policy holder, the sum assured plus any accumulated bonuses will be paid out. |

| Non-participating (Non-par) | Upon the death of the policy holder, the sum assured will be paid out. |

| Investment Linked (ILPs) | Upon death of policy holder, the value of the ILP units at that time will be paid out. (May include sum assured plus value) |

How Endowment Plan Works?

- Policyholder pays for his policy by a monthly/quarterly/yearly/lump sum fixed contribution.

- Upon maturity, the policyholder will receive a payout.

- Time to maturity can range from less than 10 years to the more common 15,20 or 30 years.

Editor’s note: To be honest, I hate going through information when it comes to insurance. They always appear complicated for a simple fundamental behind it, as if their mission is to confuse instead of educating.

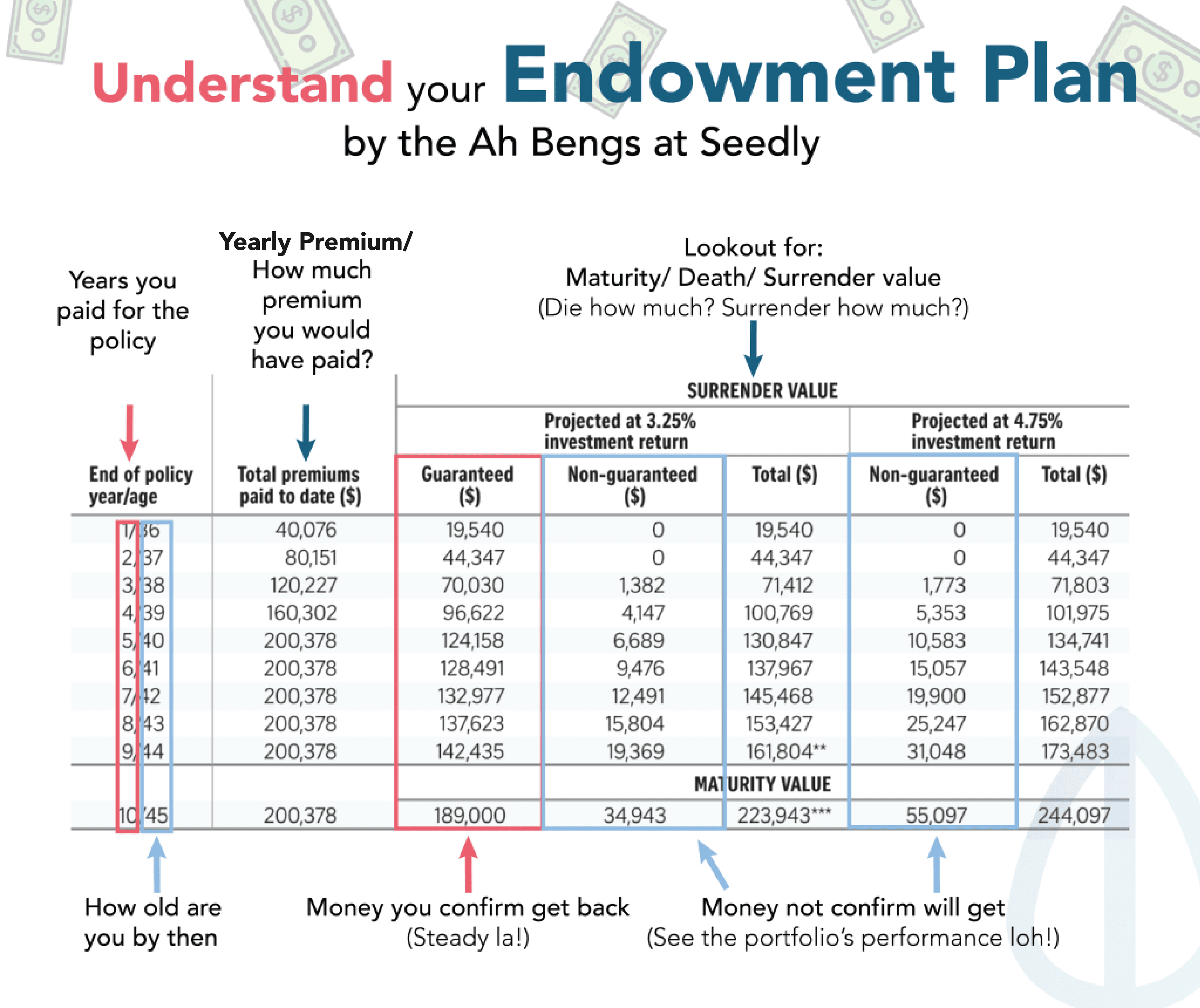

Things to look out for when going through your policy

Guaranteed Capital

The sum of money one will definitely get back upon maturity of his policy.

Payment Term

The duration of which one will need to pay for his policy.

Policy Term

The period of coverage provided by an insurance policy

Projected rate of return

The Benefit Illustration of Endowment Policy is usually projected at 3.25% and 4.75% as set by the Monetary Authority of Singapore (MAS). It is a benchmark measurement to determine how much will an Endowment policyholder get, should the funds behind the policy obtain a certain return.

To note: One should not think that, 3.25% or 4.75% is what his policy will actually earn him! The actual number is lower due to

- mortality cost

- management expenses

- distribution costs

- Basically, a lot of other costs

Maturity Benefit (Maturity Value)

The sum of money one will definitely get back upon maturity of his policy.

Death Benefit

The sum of money the policyholder’s beneficiary will definitely receive upon the death of policyholder.

Total Surrender Value

The sum of money one receives should policyholder terminate/cancel his policy.

Actual Return of Endowment Plan

While it is very common to be presented with a optimistic view on projected return of 3.25% and 4.75%, it is important to note that this WILL NOT be the kind of returns you will be getting!

A quick rule of thumb will be that the policyholder’s return will always be lower than that of the Projected Investment Return shown on your Benefit Illustration.

Surrender value can also be affected by

- the amount of Death Benefits

- Period of the Endowment policy

- Mode of paying the premium

- Possible Annual payout system for the policy

- Age when you bought the policy

A few example to further illustrate the point:

Example 1:

Assuming the below policy and policyholder would like to find out more about the actual returns they will be getting.

Using the XIRR Calculator, we calculated that

- If projected returns is 3.25%, the above policyholder’s returns when he held to maturity will be 1.40%

- If projected returns is 4.75%, policyholder’s return when he held to maturity, would be 2.49%

Example 2:

Retire Happy By AXA

- Pays 15 years of premium

- Rest of premium payment for 8 years

- After which, choose between annual payouts for 20 years or lump sum on 20th year

source: Seedly Personal Finance Community

Using the XIRR Calculator, we calculated that

If the policyholder went ahead with the lump sum payment,

- If projected returns is 3.25%, and the above policyholder’s returns when he held to maturity will be 2.92%

- If projected returns is 4.75%, policyholder’s return when he held to maturity, would be 3.75%

Editor’s note: Do note that early redemption of Endowment policy usually comes with heavy penalty.

Further Reading: Case study of various Endowment Plan

To better illustrate how Endowment works, we use a few products available in the market to walk you through. This should give a good insight on how Endowment Plan works in general.

Case study 1: NTUC Income Endowment

- One can choose a premium payment term of 10, 15, 20, 25 or 30 years for NTUC Income Endowment. One can also opt for the policy to mature when you are age 54, 59, 61 or 64.

On top of that, it covers:

- Total and permanent disability (TPD), and death benefit

If the insured becomes totally and permanently disabled (before the age of 70) or dies during the term of the policy, the policy will pay the sum assured and bonuses.

- Maturity benefit

If the insured is still alive at the end of the policy term without ending the policy early, we will pay the sum assured and bonuses.

Case study 2: Prudential PRUwealth

- One can choose a premium payment term of 5,10 or 20 years for PRUwealth.

* Project returns are based on 20 years after premium payment term!

- Death Benefits: The higher of:

- 105% of the total premiums paid (excluding premiums for supplementary benefits (if any) less any bonus surrendered or

- 101% of the surrender value

Advertisement