Singapore Savings Bond Hack: Should You Switch To An SSB With Higher Interest Rate?

If you’re here, you already know what Singapore Savings Bonds are and have invested in them.

But what if next month’s SSB interest rates are better than the SSB you bought for this month?

How sia.

Let’s find out.

TL;DR: Singapore Savings Bond Hack – Should You Switch To An SSB With a Higher Interest Rate?

- It is worth reinvesting in an SSB issue if the difference in returns is higher than $6.

- There is a $2 transaction fee each time you invest in or redeem an SSB (totaling $6 if you reinvest in an SSB)

So What Are The SSB Interest Rates?

As an investor, your potential returns would be your most immediate concern when deciding if a financial instrument is worth your time.

So if you’re wondering what the interest rates of the outstanding Singapore Savings Bonds are like…

Here’s a brief look at the average interest per annum after 1 year, 5 years, and 10 years:

| Singapore Savings Bond Issued | Avg p.a. return after 1 Year | Avg p.a. return after 5 Years | Avg p.a. return after 10 Years |

|---|---|---|---|

| Apr 2022 | 0.71% | 1.68% | 1.91% |

| May 2022 | 0.86% | 1.91% | 2.09% |

| Jun 2022 | 1.43% | 2.37% | 2.53% |

| Jul 2022 | 1.69% | 2.54% | 2.71% |

| Aug 2022 | 2.00% | 2.82% | 3.00% |

| Sep 2022 | 2.63% | 2.69% | 2.80% |

| Oct 2022 | 2.60% | 2.64% | 2.75% |

| Nov 2022 | 3.08% | 3.16% | 3.21% |

| Dec 2022 | 3.26% | 3.39% | 3.47% |

| Jan 2023 | 2.95% | 3.09% | 3.26% |

| Feb 2023 | 2.84% | 2.84% | 2.97% |

| Mar 2023 | 2.76% | 2.76% | 2.90% |

| Apr 2023 | 3.01% | 3.01% | 3.15% |

You’ll notice that the SSB interest rates have been quite volatile recently.

A Possible SSB Hack To Up Your SSB Investing Game

What happens if you’ve already committed to an earlier SSB but the next issuance promises better returns?

According to the Seedly Personal Finance Community, there was a suggestion to

- Withdraw whatever amount is invested in the bonds which has a lower rate of return, then

- Invest the same amount in a bond with a higher rate of return

The problem here is that there’s a transaction fee of S$2 charged each time you withdraw or invest in SSBs.

When you are reinvesting an old SSB into a new one, you would be incurring a loss of $6. One for your first investment, one for your first redemption, and one more for your reinvestment into the new SSB.

So when will this make sense?

Scenario 1: You Withdraw And Invest In Next Month’s SSB

Let’s say you:

- Are already invested in a March 2023 issued SSB for 2.90% returns

- Realise that the April 2023 issued SSB gives 3.15% returns (0.25% difference in returns)

Should you redeem your March-issued SSB and re-invest that money in the April-issued SSB instead?

| Amount invested | Total Interest from Mar 2023 contract | Total Interest from Apr 2023 contract | Difference in interest | Is the difference more than $6? | Additional returns |

|---|---|---|---|---|---|

| $500 | $145 | $158 | $13 | YES | $7 |

| $1000 | $291 | $316 | $25 | $19 |

As shown in the table above, it’ll only make sense if the difference in returns is higher than $6.

Note: depending on the amount you invested initially, you might receive a healthy sum of pro-rated interest despite the early withdrawal.

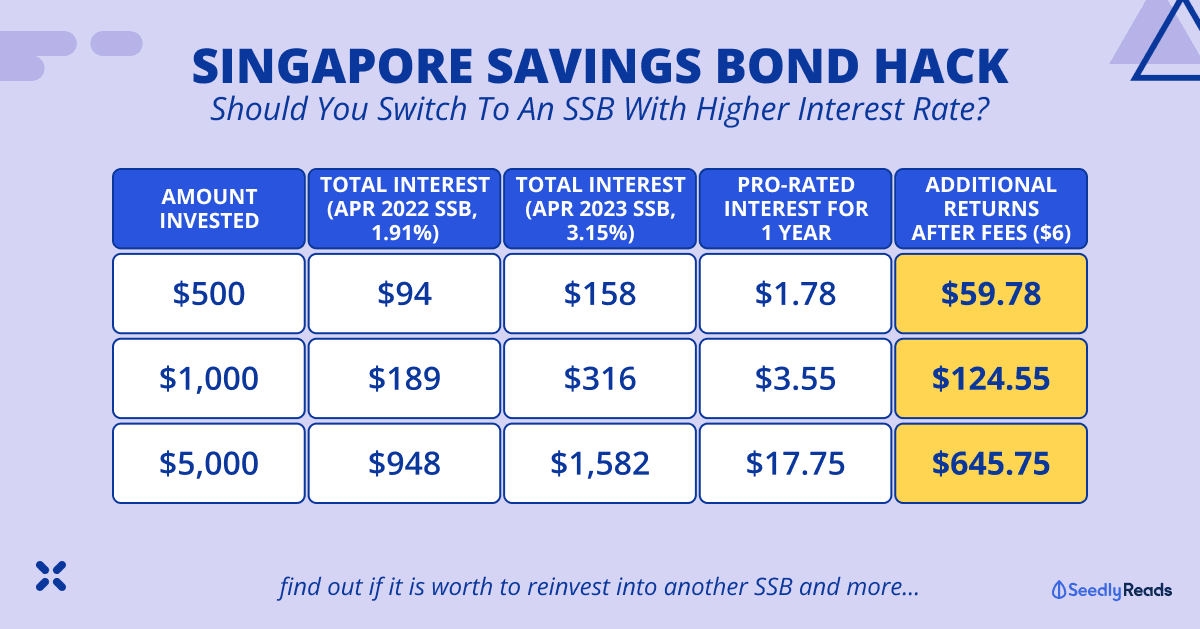

Scenario 2: You Withdraw And Invest In Next Year’s SSB

Now, let’s say you:

- Are already invested in an April 2022 issued SSB for 1.91% returns

- Learn that the April 2023 issued SSB gives 3.15% returns (0.22% difference in returns)

So should you redeem your April 2022 issued SSB, that you’ve already been holding for a year.

And re-invest that money in the April 2023 issued SSB instead?

We ran some numbers and here’s what we found:

| Initial Amount Invested | Apr 2022 SSB if hold till maturity (10 Years) earns: | Apr 2023 SSB if hold till maturity (10 Years) earns: | Pro-rated interest from early redemption of Apr 2022 SSB after 1 Year | Additional returns (after deducting $6 fees) |

|---|---|---|---|---|

| $500 | $94 | $158 | $1.78 | $59.78 |

| $1,000 | $189 | $316 | $3.55 | $124.55 |

| $5,000 | $948 | $1,582 | $17.75 | $645.75 |

Even with the minimum investment of S$500, redeeming your April 2022 SSB a year later and re-investing that same amount into the April 2023 issued SSB will net you an extra S$59.78 interest.

That’s accounting for the loss of $6 (remember the $2 transaction fee?).

However, this really depends on a case-by-case basis so you’ll need to do a little math to figure out if it’s worth redeeming early and re-investing into another SSB issued at a later date.

Creating a Bond Ladder

If you have sufficient funds, you could also use this strategy to do what we call a bond ladder. You could invest in a few SSBs and redeem them early to put them into SSBs with higher interest.

Since your SSBs will have varying maturities, you can create a ‘ladder’ of bonds, which can help you mitigate interest rate changes over time. Similar to dollar-cost-averaging.

The downsides to this are that you must factor in the transaction costs and do some calculations to make this work.

So… How Do I Redeem A Singapore Savings Bond?

When your SSB fully matures – 10 years from its issuance date – your initial principal and accrued interest will be credited to your bank account (DBS/POSB, OCBC, or UOB), which you used to purchase the SSB via Direct Crediting Service (DCS).

If you used your SRS funds to purchase the SSB, the payout will be credited to your SRS account instead.

But if you choose to redeem your SSB early, then you’ll have to submit your redemption request through your bank’s ATM or internet banking service instead.

Similarly for SSBs purchased with SRS, you can submit your redemption request through your bank’s internet banking service.

And as mentioned earlier, a S$2 transaction fee will apply for each redemption request.

Can I Make A Partial Redemption Instead?

Yes, you can!

The minimum redemption amount is S$500.

So you can redeem in multiples of S$500 or up to the amount you invested.

You will receive the amount you requested in full, along with any accrued interest.

Are There Other Alternatives To SSB?

Here are some other alternatives which you can consider depending on whether you want liquidity or higher interest:

Related Articles

Advertisement