How Much do I Really Need? The Full Cost of a HDB Flat (BTO | Resale | E.C.) in 2020

Joel Koh

Joel Koh●

Congratulations! If you are reading this, you are about to embark on one of the major milestones of #Adulting; getting your own home.

But as with all other major milestones of #Adulting, there are big stakes in this game.

Buying a home is a major responsibility and it is important to know what you are really getting into.

A major part of this are the costs involved.

You will need to consider what type of HDB flat you can really afford.

For those who are buying a HDB flat for the first time, there are many HDB grants available if you are looking to buy either a Build-to-Order (BTO) or resale flat or a HDB Executive Condominium (EC)

Next you will need to decide whether a bank loan or HDB loan is better for you.

But first, here is a list of all the fees and costs involved with buying a HDB flat.

Be it BTO, Resale or EC.

We got your covered!

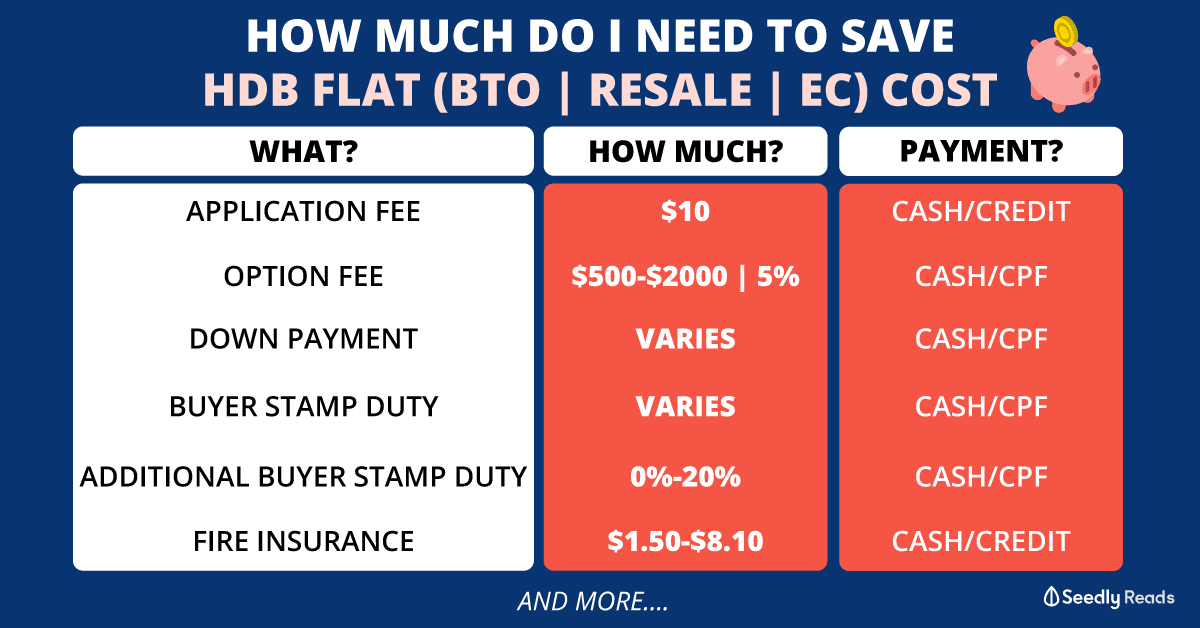

TL;DR: Comprehensive list of all the fees and costs involved with buying a HDB flat and how to pay them

Upfront Payments

- Application fee

- Option fee

- Downpayment – BTO, EC or HDB resale downpayment

- Cpf Valuation Limit and Withdrawal Limit for Balance of Purchase price

- Buyer’s Stamp Duty (BSD) and Additional Buyer’s Stamp Duty (ABSD)

- Legal Fees

- Home Protection Scheme (HPS)

- Fire insurance

HDB Application Fee For BTO | Resale Flat | EC

The first thing you will need to fork out when you buy a HDB flat be it a BTO, resale or an EC is the $10 application fee.

This can be paid via Credit Card (Visa/ Master Card) or DBS PayLah!, NETSPay, OCBC Pay Anyone, POSB digibank or UOB Mighty via

QR code.

HDB BTO Flat or HDB Executive Condominium or HDB Resale Option Fee

After you have found the HDB flat of your dreams, the next step is to pony up the option fee to confirm your flat.

| Type of Flat | BTO 2-Room | BTO 3-Room | BTO 4-Room, 5-Room or Executive | Resale Flats & Resale EC | New EC |

|---|---|---|---|---|---|

| Cost (Cash) | $500 | $1,000 | $2,000 | 5% of flat's cost (capped at $5,000)* | 5% |

*The option fee can be paid via cash, cashier’s order or cheque and is split up into two payments:

- Pay 1% of the purchase price to obtain the Option to Purchase (OTP).

- Pay up the remaining 4% of the purchase price to exercise the OTP

The option fee will first have to be paid in cash.

However, if there is sufficient money in your CPF Ordinary Account (OA) to pay the downpayment, the option fee will be refunded to you.

Otherwise, the option fee fulfils the cash portion of the downpayment (5% – 10%).

BTO | Executive Condominium | HDB Resale Downpayment Cost

The amount that you will be paying for the downpayment is dependent on three factors:

- Valuation of the property

- The loan to valuation (LTV) limit (loan ceiling) of the property

- Existing housing loan and the tenure of the new loan

What is the Valuation of the Property

For HDB flats, HDB will provide a valuation report that is an estimation of what the property is worth.

It is an essential part of the property transaction when it comes to making the downpayment and applying for a HDB loan or Bank loan.

For BTOs, the price is set by HDB during BTO sales launches.

For resale flats, it is slightly different from the concept of Cash Over Value (COV).

Do take note that if you bid over the odds for the HDB/bank determined valuation for a resale property, you will have to pay the COV in cash.

For example, you may have bid $800,000 for a HDB resale flat or HDB EC. However, when the HDB valuation report came out, the flat was only valued at $760,000 by HDB.

You will then have to make up the $40,000 COV in cash.

If you have questions about how to navigate the house buying process, you can reach out to our friendly Seedly community!

What is the Loan to Valuation (LTV) Ratio?

Essentially, the LTV ratio is a percentage value that determines how much you are allowed to borrow from the banks or HDB.

For example, if you are granted an LTV ratio of 90%, you can borrow up to 90% of your property’s valuation or purchase price (lower price will be taken).

This is the most ideal situation. Do take note that HDB might not give you the 90% LTV ratio.

They will also consider your credit score, Mortgage Servicing Ratio (MSR) and the Total Debt Servicing Ratio (TDSR).

HDB Loan Downpayment

| Type of Flat | Downpayment Amount (%) | Payment Method |

|---|---|---|

| BTO | 10% of purchase price (inclusive of booking fee and balance) | Can be paid entirely using CPF OA and/or cash |

| Resale | 10% of purchase price (inclusive of booking fee and balance) | Can be paid entirely using CPF OA and/or cash |

Bank Loan Downpayment

Since you won’t be able to take an HDB Housing Loan for your E.C., you will need to apply for a bank loan to finance your future home.

As for BTOs or HDB resale downpayment, you have the option of taking up either a HDB loan or bank loan.

You can pay the downpayment via cash, cheque or cashiers order. Here is how much the downpayment will cost.

| First Housing Loan (No prior housing loans) | Second Housing Loan Onwards | |

|---|---|---|

| Minimum downpayment (Cash) | 5% of purchase price (LTV of 75%) 10% of purchase price (LTV of 55%) | 25% |

| Remaining Downpayment | 20% Cash or CPF (LTV 75%) 35% Cash or CPF (LTV 55%) | Cash or CPF |

This is subject to bank approval. They will also consider factors similar to what HDB considers.

To help you with that decision, we have created a guide and comparison to HDB Loans and Bank Loans.

HDB BTOs – The Staggered Downpayment Scheme

You can also apply for the Staggered Downpayment Scheme. This allows you to split the downpayment into two payments

For example, if you bought a HDB BTO with a bank loan and LTV ratio of 75%,

You will need to pay the first 10% with 5% in cash + 5% using CPF OA savings or cash after signing the lease agreement.

The next half will be collected when you sign the Terms of Agreement and collect your keys.

You can pay the remaining 15% using CPF OA savings or cash.

Cpf Valuation Limit and Withdrawal Limit HDB Loan & Bank Loan

When paying off with the rest of the purchase price, this is what you’ll need to consider with regards to CPF.

- The Valuation Limit is the lower of the valuation price and purchase price at the time of purchase.

- The Withdrawal Limit is the amount of CPF OA you can use for your house, it is currently capped at 120% of the Valuation Limit.

| Loan Type | Type Flat | Applicable limits | The Amount of CPF-OA Usable for Home Loan Repayment |

| HDB | BTO Flat | No Limits | Full OA |

| Resale HDB flat | Valuation limit | Age <55

You will need to have the Basic Retirement Sum (BRS) amount in your CPF Ordinary Account(OA) and Special Account (SA) Age >55 You will need to have the BRS amount in your CPF Retirement Account (RA), SA (inclusive of withdrawn investments) and OA. |

|

| Bank | BTO Flat Resale Flat EC |

Valuation and Withdrawal limit |

For a more specific answer to your situation, please use the CPF Housing Limits calculator to see if you exceeded the CPF Withdrawal Limit.

Buyer’s Stamp Duty (BSD) and Additional Buyer’s Stamp Duty (ABSD)

The BSD and ABSD are applicable to BTOs, Resale and ECs.

BSD

The BSD based on the selling price of the flat. The amount payable is calculated as such:

- First $180,000: 1%

- Next $180,000: 2%

- Next $640,000: 3%

- Remaining amount: 4%

ABSD

You are liable to pay ABSD on in addition to BSD residential property purchases if you are a:

- A Singapore Citizen (SC) who is buying his/her’s second residential property

- Singapore Permanent Resident (PR)

- Foreigner

Here’s how much you have to pay:

| Status | ABSD rate |

| SC purchasing your first residential property | 0% |

| SC purchasing a second residential property | 12% |

| SC purchasing a third residential property | 15% |

| PR purchasing your first residential property | 5% |

| PR purchasing a second residential property | 15% |

| Foreigner resident buying any property | 20% |

Pro tip: No need to do this manually, use the Stamp Duty Calculator from the Inland Revenue Authority of Singapore (IRAS) website to calculate the stamp duty payable for your flat purchase.

You can use your CPF to pay the BSD and ABSD.

But, you will first have to fork it out in cash and then seek a reimbursement from your CPF account.

For more information, you can check out the IRAS website and the CPF website.

HDB Home Loan Legal Fees

These are the legal fees you’ll need to pay if you are buying a HDB flat using a HDB loan.

Most people will appoint the HDB solicitor to act on your behalf of the sale as it is usually more affordable.

HDB Conveyancing Fee

The conveyancing fee is charged when HDB is acting for the buyer in the mortgage based on the mortgage loan of the flat. This can be be paid with cash/CPF.

Conveyancing fees are calculated as such:

- First $30,000: $0.90 per $1,000

- Next $30,000: $0.72 per $1,000

- Remaining Amount: $0.60 per $1,000

Please note that the minimum conveyancing fee chargeable is $20 and that conveyancing fees are subject to GST.

Registration fees

- Lease In-Escrow registration fee of $38.30 (fixed amount): Paid if HDB acts for you in the flat purchase

- Mortgage In-Escrow registration fee of $38.30 (fixed amount): Paid if HDB acts for you in the mortgage

HDB Caveat Registration Fee

The caveat registration fee of $64.45 (inclusive of GST) is payable when you sign the Agreement for Lease.

With it, a caveat is lodged with the Singapore Land Authority to protect your interest in the flat.

This is done by giving notice of your interest pending the Lease registration. This can be paid with cash/CPF.

Survey fee

The survey fee amount is based on your flat type. Please note that the survey fee is subject to GST. This can be paid with cash/CPF.

Flat Type Survey Fee (Before GST):

- 1-Room: $150

- 2-Room: $150

- 3-Room: $212.50

- 4-Room: $275

- 5-Room: $325

- Executive Flat: $375

Calculation of Stamp Duty on Deed of Assignment

The stamp duty on Deed of Assignment is payable if you are taking a housing loan. It is calculated at 0.4% of the loan amount, subject to a maximum of $500. This can be paid with cash/CPF.

Title Search Fees

The title search fees cost $10.40 and can be paid with cash/CPF.

Pro tip: You can get an estimate of all the legal fees involved on HDB’s Legal Fees Enquiry Facility Page.

Bank Loan Legal Fees

If you are getting a bank loan, you will have to get an external lawyer who will help you through the whole process.

They will charge about $2,500 – $3000 for their services.

If you taking a bank loan, banks will usually have a set of law firms they prefer to deal with, you can approach you banker for the list of law firms and enquire with the law firms for pricing.

This can be paid via cash or CPF. However, you will have to ask the law firm if the fees can be paid via CPF.

Home Protection Scheme

The Home Protection Scheme (HPS) is an insurance policy that protects CPF members and their families from losing their HDB flat in the event of death, terminal illness or total permanent disability.

The premium is paid annually using your CPF savings or cash. The premium amount depends on factors such as your declared percentage of coverage, loan amount, age, and gender.

The CPF Board website also has a Home Protection Scheme Premium Calculator you can use to estimate the HPS premium amount.

HDB Fire Insurance

After 1 September 1994, HDB has made it mandatory for homeowners to buy and renew the HDB fire insurance for your homes as long as you have an outstanding HDB loan.

This HDB fire insurance is underwritten by FWD Singapore.

The cost ranges from $1.50 to $8.50 (inclusive of GST) for 5 years and is dependent on the size of your flat.

| Flat Type | 5-Year Premium (Including 7% GST) | Sum Insured |

|---|---|---|

| 1-room | $1.62 | $29,000 |

| 2-room/ 2-room Flexi | $2.71 | $48,700 |

| 3-room | $4.87 | $60,400 |

| 4-room/ S1 | $5.94 | $82,000 |

| 5-room/ S2/ 3-Generation | $7.13 | $97,300 |

| Executive/ Multi-Generation | $8.10 | $106,200 |

| Studio Apartment (Type A/ B) | $2.71 | $48,700 |

Additional Recurring Charges

On top of the monthly home loan instalments, please budget for other recurring costs that arise from homeownership.

These include:

- Maintenance, conservancy charges and utilities

- Property tax

- Home-related insurance (Optional but recommended to protect your house)

There you have it. All you need to know costs wise about buying a BTO flat, Resale flat or Executive Condominium in Singapore.

If you have any other additional questions, do reach out to our friendly Seedly community!

You can also head there to answer questions and share your newfound knowledge with them!

Advertisement