We once received a really good question on retirement. You see, most Singaporeans only start to think about retirement at the age of 38 years old. While 38 years old is already quite late an age to start planning, what happens if one starts later than that?

We find out from the community this week.

The context of the question:

- Last month, the member started investing through a well known Independent Financial Advisory (IFA) on Unit Trusts, with an annual management fee of 1.25%.

- The member wishes to have a 4% or slightly higher return per annum for the next 15 to 20 years.

- Due to age, the member is risk averse and do not want to really spend too much time monitoring the investment.

- Ultimately, the aim is to allow the member’s savings to beat inflation.

- Has no idea on how to invest in Index Fund, STI ETF.

Background of the member will be:

- 48 years old and am unfamiliar with investment.

- Helps out with spouse’s business from home and main income comes from the spouse.

Assumptions on retiring in Singapore

- Singaporeans generally need S$1,200 per month for basic monthly expenses after retirement. This amount is going to increase with the incoming Goods and Services Tax (GST) hike.

- Assuming inflation to be 0%, this amount works out to be about $14,669 per year.

- Singaporeans are expected to live up to an average age of 82.9 years old.

- Taking CPF Monthly Payout out of the equation, and targetting retirement age to be at 67 years old, one will need a total saving of $233,205 for retirement.

Should the member be starting his savings from S$0 (which I highly doubt so), that will need a saving of S$12,273 each year. The longer one delays saving up, the higher that number of annual saving is going to get.

For this member’s case, she falls between the age of 40-50 years old. Singaporeans in this group has a few pros and cons when it comes to investing.

Pros of being 40-50 years old

- Hitting the peak of your salary

Cons of being 40-50 years old

- Financial commitment might be high due to children going to college and universities

- Lesser time to plan for retirement

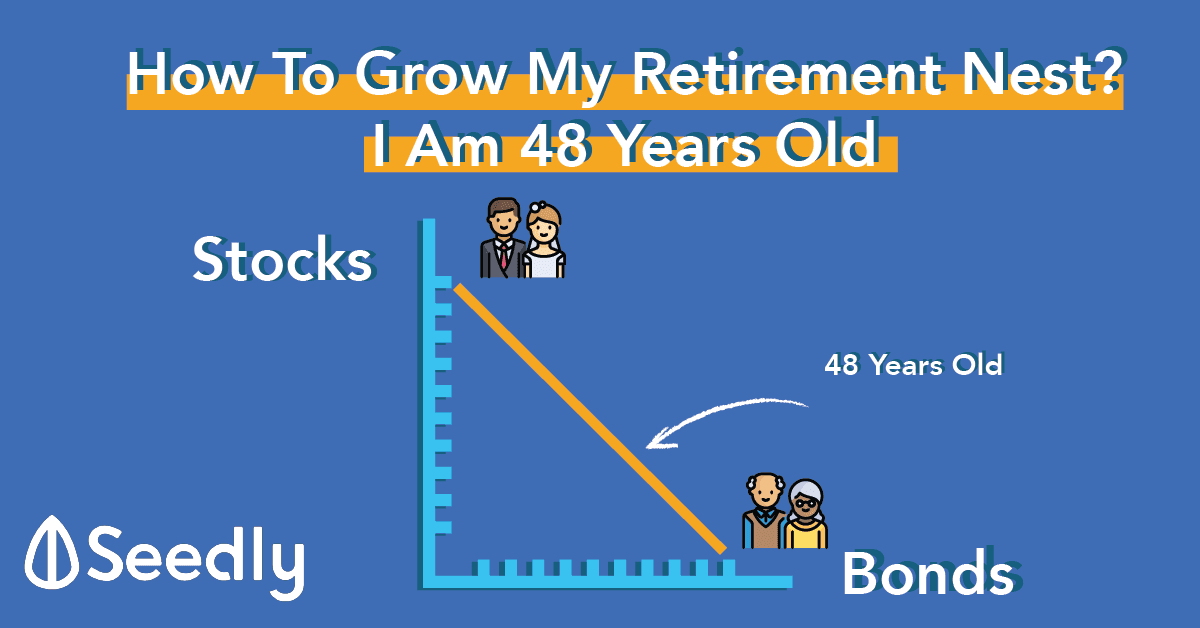

We once covered the different risk one should undertake as one grows older. In this case, depending on how much the member saved over the years, the percentage has to be a balance between high-risk assets such as stocks and low risks one such as bonds.

All this after one manages to secure the retirement amount in the CPF.

Read more: Age vs Risk Profile: What Investments Should You Hold At Your Age

Seedly Community’s help on what you can do

- Focus on what your goal is, in this case, it is growth

“Actually what you want can be achievable through Unit Trust too. Actually, do not be over concern about the management fee as your goal is the growth. As long as the product does its job by helping you achieve your goal, it is not a bad choice.”

– Soon Xiaohui

- Using Robo-advisory platforms to invest in index funds could be an option

“Invest in index funds effortlessly using robo-advisory platforms. Some examples will be Autowealth, Stashaway etc. On top of that, there is little for you to monitor as the software does the monitoring for you.”

– Lim Chun Long JimmyNote: You can also read real user reviews on robo-advisory platforms here.

- Alan Kor

Central Provident Fund (CPF) members currently earn interest rates of up to 3.5% per annum on their Ordinary Account (OA) monies and up to 5% per annum on their Special and Medisave Account (SMA) monies. Retirement Account (RA) monies currently earn up to 5% per annum.

These interest rates include an extra 1% interest paid on the first $60,000 of a member’s combined balances (with up to $20,000 from the OA).

CPF members aged 55 and above will also earn an additional 1% extra interest on the first $30,000 of their combined balances (with up to $20,000 from the OA). As a result, CPF members aged 55 and above will earn up to 6% interest per year on their retirement balances.

This is part of the Government’s efforts to enhance the retirement savings of CPF members. - Ronald Wong

Depending on your capital sum required at retirement, and the amount you have to invest today and over the next 15 years.

It is probably best to max up your CPF-SA first (with its statutory limitations), at 55 opt for Enhanced Retirement Sum (ERS) and the Escalating option to hedge inflation during your retirement. Do so before considering other forms of investment.

The investment might not suit you since you mentioned you are risk averse, and requiring 4% is in no way easy. So max out the risk-free options first via CPF, then look at investing the rest into ETF/index or other trackers. Do note that they are not without risks especially when the market experienced significant drawdown closer to your retirement.

You need to structure a liquidity plan closer to retirement, so your actual investment time frame might actually be shorter. Do not discount retirement income plans from insurers also, for safe and guaranteed income payout at retirement. - As Df

Unless your IFA is guaranteeing the returns, you will still need to monitor your own investment unless you’re prepared to risk “waking up” in a couple of decades to significantly lower than projected returns. Given that unit trusts are actively managed in a bid to ‘beat the market”, I don’t see how that is supposed to be less risky than an index fund. - Xue Yuan

2-cents on a possible investment portfolio.

Since you are currently at age 48, using a simple rule of thumb:(110 – Your Age) = % of the portfolio that should be in equities

62% of your investments should be in stocks and 38% in bonds. Increase the allocation into bonds every year following the same formula.

Some suggestion will be:

31% into the STI ETF

31% into iShares Core MSCI World UCITS ETF Fund

Remaining 38% into ABF SG Bond ETF - Colin Lai

Let me be frank.

CPF SA grows at 4%. When you want to draw out the money you can but need to leave minimum sum intact. The extra you can take out.

Note that no endowment plan out there can provide CPF Life monthly payouts for life. You need to maximise this avenue.

Next, unit trusts cannot beat robo’s ETFs simply on the basis of the number of charges for Unit Trusts.

With agent fee at 1%, 1.5% management fee and sales charge if any means that you are 2.5 to 3 % down per year already. This steepens the returns your fund needs to grow by 4% + additional 2.5% = 6.5% to get your 4% target you want.

If you use robo advisers, you can get 6.6% but with fees of 0.5%, the remaining 6% is all yours. My recommendation:

1. CPF first

2. Robo ETFs.

3. REITS and

4. Gold.

Consider all 4. If your Financial Advisor can only do Unit Trusts, then be very careful. Remember that you are losing 2-3% annually to charges. When you compound it, it comes to tens or hundreds of thousands depending on your investment amount. - Siti Putri

If you have at least $300k lump sum depending on which bank, you may be considered high-net-worth individuals and considered Accredited Investor if u have annual salary of $300k or $2mil in assets (including property) so, consider approaching your bank because they may offer more attractive lump sum investment proposal that is not open to other retail investors. As usual, money makes more money, and the ‘rich’ typically gets ‘richer’. Do note that high risk may not always be high returns too. So do own diligence

Advertisement