How do most people react when something bad happens? They hope for the best.

Well, this is exactly how insurance buyers feel when they have a pre-existing condition.

I’m not just talking about long-time ailments such as heart disease, I’m also referring to temporary circumstances such as pregnancies.

If you have a pre-existing condition, don’t lose hope yet.

While it’s true that some pre-existing conditions may prevent you from getting the protection you might need, the good news is that there are more and more policies that are catered to those with pre-existing conditions.

But, they don’t come cheap.

So, what insurance can you get if you have a pre-existing condition, and at what cost? Let’s find out!

TL;DR: Insurance That You Can Get Even With Pre-existing Conditions

Click here to jump:

- What is a pre-existing condition?

- Types of insurance suitable for individuals with pre-existing conditions

Disclaimer: Do note that the information provided by Seedly serves as an educational piece and does not constitute an offer or solicitation to buy or sell any investment product(s). It does not consider the specific investment objectives, financial situation, or particular needs of any person. Readers should always do their own due diligence and consider their financial goals before investing in any investment product(s).

What Is A Pre-existing Condition?

The Ministry of Health (MOH) has identified several pre-existing conditions that are covered by MediShield Life, which is the basic healthcare insurance provided by the government.

| Broad categories | Indicative examples (not exhaustive) |

|---|---|

| Cancer | Lung cancer, colorectal cancer, breast cancer, stomach cancer |

| Blood disorders | Aplastic Anaemia, Thalassemia Major |

| Degenerative diseases | Parkinson’s Disease, Muscular Dystrophy, Amyotrophic Lateral Sclerosis (ALS) |

| Heart or other circulatory system diseases | Heart attack, Coronary artery disease, Chronic ischaemic heart disease |

| Cerebrovascular diseases | Stroke |

| Respiratory diseases | Chronic obstructive pulmonary disease |

| Liver diseases | Alcoholic liver disease , Chronic hepatitis, Fibrosis or cirrhosis of liver |

| Autoimmune/ Immune System diseases | Systemic lupus erythematosus, Human Immunodeficiency Virus/ Acquired Immune Deficiency Syndrome (HIV/ AIDS) |

| Renal diseases | Chronic renal disease, Chronic renal failure, Chronic nephritic syndrome |

| Serious congenital conditions | Congenital heart disease, Congenital renal disease, Biliary atresia |

| Psychiatric conditions | Schizophrenia |

| Chronic condition with serious complications | Hypertensive heart disease, Hypertensive kidney disease, Diabetes with kidney complications, Diabetes with eye complications |

Will Insurance Cover Pre-existing Conditions Singapore?

It’s not uncommon to see insurers stating “No coverage or benefits for pre-existing conditions the person insured is reasonably aware of”.

The hard truth is that rare diseases might not be included into this list as treatment options are often limited or highly expensive.

Still, there are insurers that who cater to the those with pre-existing conditions and probably has a checklist of health conditions to determine if the application is acceptable.

Depending on the insurer, it might not be a hard-no if conditions are well-managed.

Can Insurers Deny Me for Pre-existing Conditions?

Yes, they can reject your application if your pre-existing condition does not fall under their list of consideration.

That’s why, early clarification with your prospective insurer is ideal, especially those with rare conditions.

Read more:

- Insurance Policies You Need in Singapore For Each Age Group

- Best Insurance Savings Plans in Singapore (2022): Dash PET vs Singlife Account vs Dash EasyEarn vs GIGANTIQ

- Insurance: How To Review & Why You Should

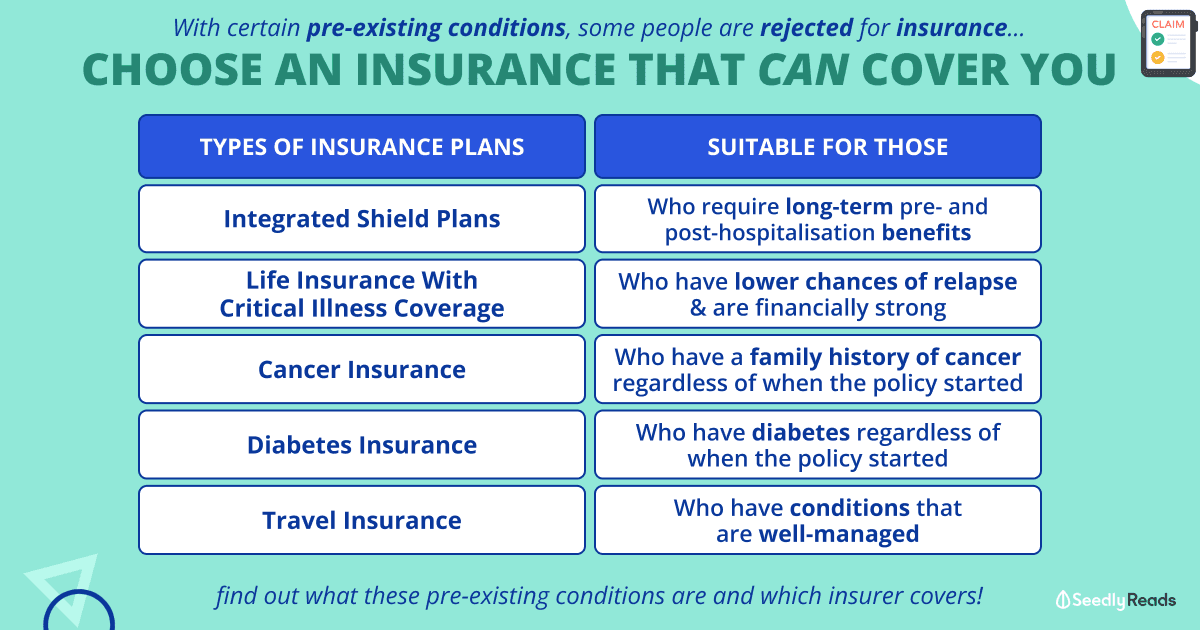

Types of Insurance Suitable For Different Pre-existing Conditions

Now, let’s move on to the insurance available to those with pre-existing conditions.

Integrated Shield Plans

Integrated Shield Plans (IPs) are essentially insurance plans that work in conjunction with the national healthcare system to provide coverage for pre-existing conditions and other medical expenses.

In other words, the IP provides additional coverage beyond MediShield Life, and for those with IP plans, you get to have the combined benefits of MediShield Life, and the additional private insurance coverage for Class A/B1 and private hospital stays.

For the benefit of everyone, do you know that MediShield Life, which is the basic healthcare insurance provided by the government and run by the Central Provident Fund (CPF), will cover all pre-existing conditions?

Even if these conditions are excluded by your private insurer from the additional private insurance coverage of your IP, should you decide to drop your IP cover one day, you will remain covered by MediShield Life.

There are two types of IP in Singapore:

- Standard IP provides coverage for Class B1 and B2 wards in public hospitals

- Private IP offers coverage for Class A wards and private hospitals.

It’s important to note that the better the coverage, the higher the premium.

For the uninitiated, the Raffles Shield Insurance covers 3 pre-existing chronic conditions (Hypertension, Hyperlipidaemia and Diabetes) subject to review if the conditions are well-managed.

Policyholders with these pre-existing conditions will have to enrol in their Raffles Care Management Programme and the doctors will help to manage patient’s health.

In the event that other pre-existing conditions (glaucoma, kidney disease, cancers etc), the application will be subject to underwriting.

Life Insurance with Critical Illness Coverage

In general, it is difficult to find life insurance plans that offer critical illness coverage for pre-existing conditions, but there are some that include such coverage.

But, they may charge a higher premium, and may come with certain conditions and limitations.

This type of policy typically pays out a lump sum of money if the policyholder is diagnosed with a specified critical illness, such as cancer, heart attack, or stroke.

Some of these plans may include what is called, a Multi-pay feature which pays out in stages and ensures policyholders are covered in the event of multiple critical illness diagnoses.

The Seedly community has asked if this is a necessary feature.

There are various school of thoughts and some insurers might already auto-include this feature in their life insurance plans.

Some people have also suggested that it would be good to have both a Whole Life and also a Term so that you have coverage during every phase of your life, or to look at a higher coverage during active years.

This is because you may claim from the multi-pay plan first, leaving your Whole Life plan to continue to build bonuses for the future.

That said, you should consider the chances of relapse and if you could stay financially strong during the treatment process.

Read more:

- Key Types of Insurance Policies You Should Get In Singapore (2023)

- The Ultimate Female Insurance Plans Comparison (With Free Health Checkup)

Cancer & Diabetes Insurance

Almost 1 in 4 people may develop cancer in their lifetime, and in an unfortunate event where such news had to be dealt with, the least we would want to worry about is the medical treatment costs.

Cancer insurance is a type of insurance policy that provides coverage for medical expenses related to the diagnosis and treatment of cancer. It is designed to help individuals and their families cope with the financial burden of cancer treatment, which can be very expensive.

There are some insurance plans such as the Income Cancer Protect that has a 30% success signed up rate. According to their website, a 30-year-old male non-smoker, looking for $50,000 sum assured, can enjoy that coverage from just $14.40 per month.

Similarly, the Income Silver Protect also offers protection against early and advanced stage cancers.

On a related note, there are also Diabetes Insurance that you can purchase after you get diabetes, such as the AIA Diabetes Care.

Travel Insurance

Some travel insurance policies provide coverage for pre-existing conditions, although this is usually limited to emergency medical expenses incurred during a trip.

Nonetheless, it’s good to know that you can still get yourself covered in case something happens overseas.

If you’re looking for extensive coverage, we’ve previously covered their benefits and premiums.

Read more:

- Travel Insurance Claim Guide: From Baggage Loss, Trip Cancellations to COVID-19

- Things To Look Out For When Buying Travel Insurance

Afterthoughts

I may sound like I’m promoting insurance here, but I’m setting the record straight that I’m not.

It’s actually more common than you think that someone has got their insurance applications rejected because they have a pre-existing condition.

In cases like that, you can be a helpful peer to inform them that they should:

- Check insurer’s list of pre-existing conditions

- Ensure medical records are updated

- Check the chance of getting their applications approved

That said, do you know anyone who has successfully applied for a health or life insurance even thought they have a pre-existing condition?

Share them with the Insurance Group on Seedly!

Related Articles:

- Insurance Policies You Need in Singapore For Each Age Group

- Insurance: How To Review & Why You Should

- Travel Insurance Claim Guide: From Baggage Loss, Trip Cancellations to COVID-19

- Best Travel Insurance in Singapore (2023): Travel With a Peace of Mind

- Best Pet Insurance in Singapore For Your Best Friend (2022)

Advertisement