Singaporeans Guide To Investments Products That Give Guaranteed Returns

Best Investment In Singapore

Singaporeans got our back against the wall.

Cornered by the ever-increasing cost of living, the only way forward is to increase our returns through investments in the hope of offsetting inflation rate.

Very much like our love for durians, we want our investments to be “Bao Jiak” (guaranteed delicious).

With certain level of risk pegged to various investment products, we went on a journey to look for investments that provide guaranteed returns. If your definition of the best investment is one that does not involve taking up much risk, we have some of these investment options for you.

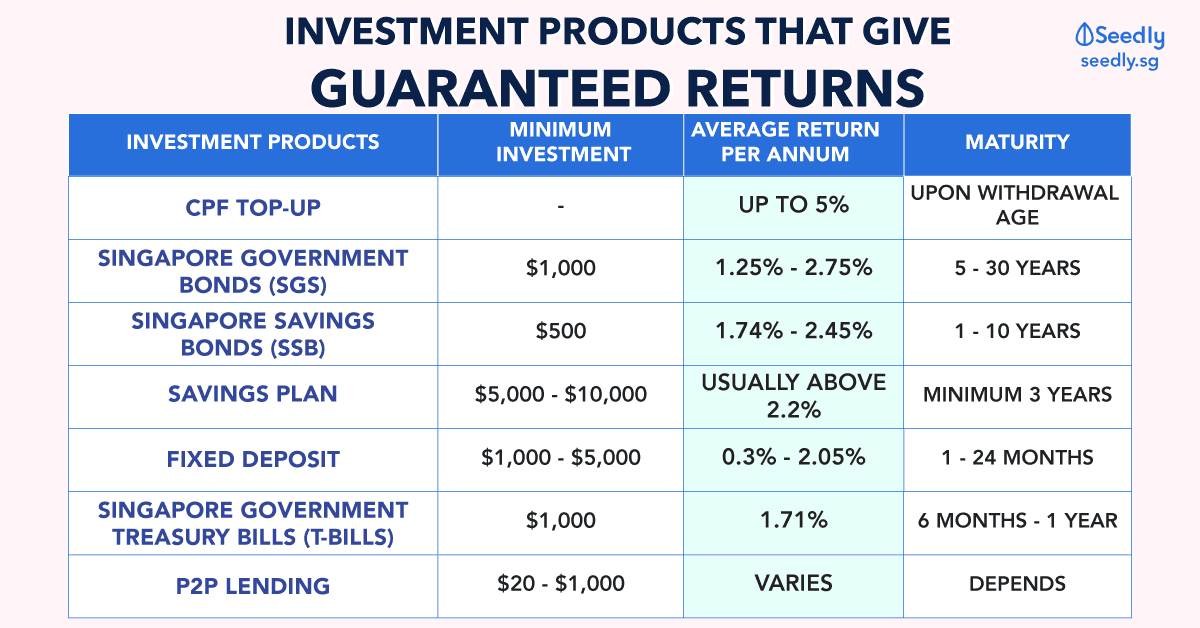

Investments Or Financial Products With Guaranteed Returns

| Products | Minimum Investment | Average Return Per Annum | Maturity |

|---|---|---|---|

| CPF Top-up | - | Up to 5% | Upon withdrawal age |

| Singapore Government Bonds (SGS) | $1,000 | 1.25% - 2.75% | 5 - 30 Years |

| Singapore Savings Bond (SSB) | $500 | 1.74% - 2.45% (Based on SSB issued in 2019) | 1 - 10 Years |

| Savings Plan | $5,000 - $10,000 (Depends on the insurer) | Usually more than 2.2% | Minimum 3 Years |

| Fixed Deposit | $1,000 - $5,000 (Depends on the bank) | 0.3% - 2.05% | 1 Month - 24 Months |

| Singapore Government Treasury Bills (T-Bills) | $1,000 | 1.71% | 6 Months - 1 Year |

| P2P Lending | $20 - $1,000 | Varies | Depends |

Singapore Savings Bond (SSB)

The return on Singapore Savings Bond (SSB) is updated once a month.

It is open to individuals aged 18 years and above, as long as you have a bank account with one of the 3 local banks and an individual CDP Securities account.

The interest rate for Singapore Savings Bond (SSB) is backed by the Singapore Government and investors of SSB can get their investment amount back with little risk of capital loss. It also allows liquidity given that there is no penalty for early withdrawal of the bond.

Probably one of the more “Bao Jiak” product in the market right now.

Here are the average return per annum for the SSB, when held to maturity, in for this year so far:

| SSB Issue Date | Average Return Per Annum (after 10 years) |

|---|---|

| January 2019 | 2.45% |

| February 2019 | 2.20% |

| March 2019 | 2.18% |

| April 2019 | 2.16% |

| May 2019 | 2.16% |

| June 2019 | 2.13% |

| July 2019 | 2.16% |

| August 2019 | 2.01% |

| September 2019 | 1.95% |

| October 2019 | 1.75% |

| November 2019 | 1.74% |

While the interest rate for some of the SSB issue may seem low for some of the investors, taking into account that it provides guaranteed returns, reasonable liquidity and no penalty for withdrawing early, it is still one of the preferred investment options for Singaporeans.

Source: Seedly CommunitySome of the risks of investing in SSB includes:

- Default risk of the government

- Low returns which can barely beat inflation

- One month is required to withdraw the money. It is not 100% liquid.

Fixed Deposits

Fixed deposits are a low-risk investment that gives guaranteed returns on the money you put in it. Fixed deposit is an instrument that was really popular with the older generation, back when there were fewer investment instruments to look at.

Fixed deposit still serves its purpose today as a safe viable option for Singaporeans to park their money, do note that most fixed deposit has early withdrawal fees, minimum lock-in period and minimum deposit amount.

Savings Plan By Insurance Companies

Savings plans, also commonly known as short-term endowment savings plans, are recently gaining a huge amount of popularity amongst Singaporeans.

From the looks of some of these short-term endowment plans such as the AVIVA MySecureSaver, NTUC Income Capital Plus (CSN2), Singapore Life’s Endowment Series Four and GREAT220 by Great Eastern, we noticed that these plans usually get fully subscribed really fast.

The benefits of these saving plans are that they offer quite a good return of more than 2.2% per annum with a short tenure of 3 years. The investment capital for some of these plans is also protected by SDIC up to $100,000 of the surrender value which makes it even more attractive.

The downside of a savings plan is:

- The risk of the insurer defaulting

- The lack of liquidity

- It is only limited in terms of the quantity available for the consumers to invest in

Singapore Government Bonds (SGS)

The Singapore Government Securities (SGS) bonds pay a fixed interest rate with a maturity date that stretches from 2 to 30 years. These bonds are issued by the Singapore Government and pay a fixed coupon every 6 months.

The SGS bond is given AAA credit ratings across international credit rating agencies such as Moody’s, S&P, Fitch and R&I indicating the chance of it defaulting is low.

Here’s what the average returns for SGS Bond prices for October 2019:

| Maturity | Coupon Rate |

|---|---|

| 5 Years | 1.25% - 2% |

| 10 Years | 2.125% - 2.75% |

| 15 Years | 2.875% - 3.25% |

| 20 Years | 2.25% - 3.5% |

| 30 Years | 2.75% |

Like the SSB, SGS is regarded as a low-risk investment.

P2P Lending

This might be of a stretch, but some P2P lending platforms are adopting this concept of guaranteed returns on investments.

This means that investors will no longer be undertaking the risk when borrowers default. The risk of default is transferred to the P2P Lending company, and investors will continue to receive returns for his investments.

In this case, the risk of the investor is pegged to the strength of the P2P lending company.

Central Provident Fund (CPF) Top-Ups

Have as much disagreement you want about the CPF you want, but one thing for sure is the interest you will get from the Central Provident Fund (CPF).

Other than the bad part about only being able to withdraw your CPF savings at age 55, topping up your Special Account (SA) gives you a minimum return of 4.0% per annum. This return is backed by the Singapore government and one get to enjoy tax relief along with the voluntary contribution too.

The interest rate for CPF is as follows:

| CPF Account | Interest Rates* |

|---|---|

| Ordinary Account | Up to 2.5% |

| Special Account | Up to 4% |

| MediSave Account | Up to 4% |

| Retirement Account | Up to 4% |

The table includes the additional 1% per annum extra interest on the first $60,000 of combined CPF balances, of which up to $20,000 comes from the Ordinary Account (OA).

The maximum amount of tax relief for topping up your CPF is at $7,000 per the calendar year. You can also receive an additional $7,000 in tax reliefs when you top-up cash into the CPF SA of your Spouse, Parents, Grandparents, Siblings, Parents-in-law, Grandparents-in-law.

Singapore Government Treasury Bills (T-Bills)

The Singapore Government T-bills are short-term securities issued by the government. These are securities issued at a discount to their actual face value.

Like the SGS, these are some of the risk-free products available to Singaporeans.

Here’s what you need to know about SGS T-bills:

| SGS T-bills | Details |

|---|---|

| Who issues it? | The Singapore's Govenment |

| Sovereign credit rating | AAA |

| Tenor | 6 months or 1 Year |

| Interest Rate | Unlike bonds, the T-bills are issued at a discount to the face value. Hence, no coupon. |

| How to receive interest payments? | Upon maturity, investors will receive the full face value of the T-bills |

| Minimum amount required to invest | Minimum $1,000 investment amount |

The return is determined during the auction application for the Treasury bill.

One of the latest 6-Month T-bill that was announced has an average yield of 1.71% per annum.

Safe Investment Options In Singapore

While the above are some products that provide guaranteed returns, it is important that consumers assess the risk of each product before investing in them. A good guideline will be to use the credit rating available if there is any, as a benchmark for how safe the product is.

One may also notice that the interest rate and return can be relatively low when compared to a lot of other products out there, but that is just the price of the low risk some of these products provide.

Advertisement