Manulife Goal 7: 3-Year Endowment Plan with 1.39% p.a. Guaranteed Returns

Xue Miao

Xue Miao●

We’ve reached the point in life where any further drops in the interest rates for savings accounts are no longer surprising to us.

Our wildly popular Singapore Savings Bonds (SSB) have been taking the hit as well.

Which is why most of us have been looking for alternatives to park our savings at.

If cash management accounts are not your thing, short-term endowment plans can be considered if you’re looking for somewhere to place your money for a short period of time.

Disclaimer: The Information provided by Seedly does not constitute an offer or solicitation to buy or sell any insurance product(s). It does not take into account the specific objectives or particular needs of any person. We strongly advise you to seek advice from a licensed insurance professional before purchasing any insurance products and/or services.

TL;DR: Is the Manulife Goal 7 Endowment Plan Worth It?

![]()

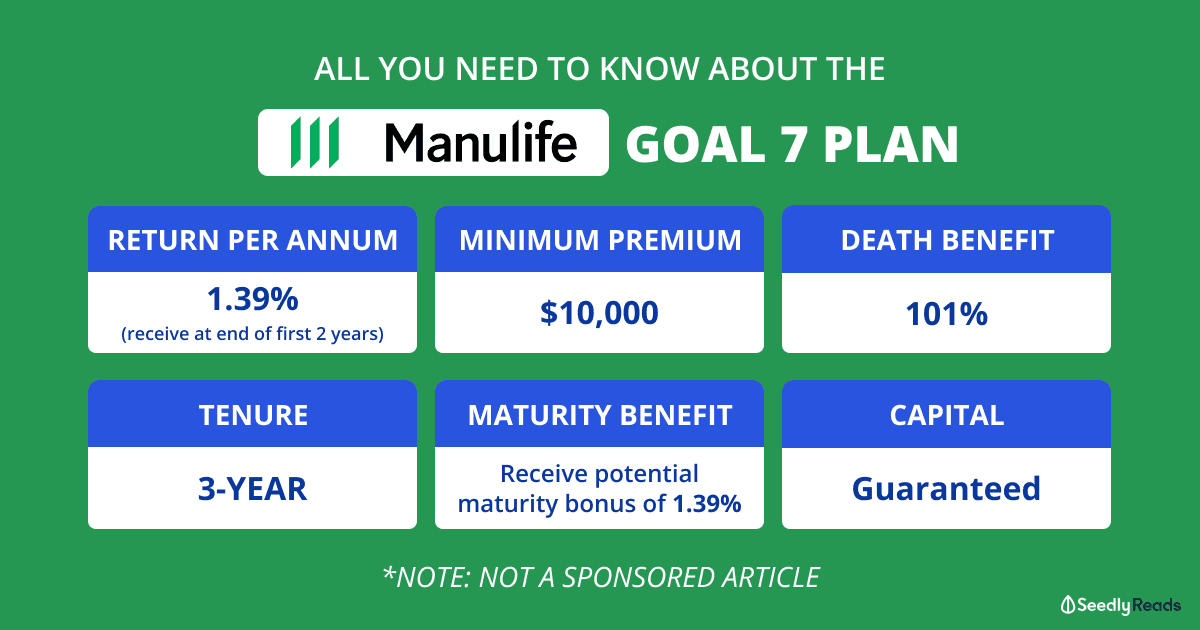

The Manulife Goal 7 is a three-year single premium endowment plan which provides a guaranteed fixed yearly income of 1.39% for the first two policy years.

Here’s a quick breakdown of Manulife Goal 7:

| Manulife Goal 7 | |

|---|---|

| Coverage | 3 Years |

| Premium | Single premium (one lump sum) From S$10,000 Payment by Cash or SRS |

| Death Benefit | 101% of single premium paid |

| Guaranteed Maturity Benefit | 1.39% p.a. |

| Possible Bonuses | Receive potential maturity bonus of 1.39% from third year (based on illustrated investment rate of return of 1.71% p.a.) |

| Issuance | Guaranteed acceptance regardless of health condition |

| Policy Protection | Up to specified limits by SDIC |

| Credit Rating of Insurance Company | AA- |

What is an Endowment Plan?

An endowment plan is a life insurance policy that gives you a death benefit and helps you save at the same time.

Once your policy matures, you’ll be able to collect your principal plus any accrued interest.

For such plans, you usually either pay regularly or make a lump sum payment (aka “single premium”).

The Manulife Goal 7 plan is a good example of a single-premium endowment plan.

Endowment plans are usually used for people to have ‘forced savings’ in the short term.

All You Need to Know About the Manulife Goal 7 Endowment Plan

1. Guaranteed Issuance

The issuance of the Manulife Goal 7 Plan is guaranteed as no medical underwriting is required.

2. Guaranteed Capital

The capital is guaranteed at 1.39% p.a., which is payable as guaranteed yearly income at the end of the first two years.

This adds up to a total of 2.78% over two years.

Policyowners can choose to withdraw these guaranteed yearly income payouts, or choose to accumulate them at a non-guaranteed interest rate.

These withdrawals can be done either in full or partially.

The minimum withdrawal amount is S$500 or the balance available.

In addition, get to receive a potential maturity bonus of 1.39% of your single premium from your third year onwards.

However, do note that this is non-guaranteed.

Note: The potential maturity bonus of 1.39% p.a. is based on a higher illustrated investment rate of return of 1.71% p.a.. Based on the lower illustrated investment rate of return of 1.15% p.a., the potential maturity bonus will be 0%.

3. Death Benefit

This policy also covers death, with a 101% payout of your single premium.

4. Invest with Cash or SRS Funds

If you’re interested in applying, you can do so via your trusted financial adviser, or do it at a bank branch.

The minimum single premium starts at $10,000.

You can choose to use either cash or your Supplementary Retirement Scheme (SRS) funds to invest in this plan.

However, if you’re thinking of doing a lump sum top-up for payment via SRS, you might want to note that the maximum yearly contribution limit for SRS is $15,300 for Singapore citizens and PRs.

As such, please ensure that there is sufficient balance in your SRS account before proceeding with this.

An Example of How Manulife Goal 7 Can Help You and Your Savings

Should I Invest In the Manulife Goal 7 Plan?

If you have been on a lookout for somewhere to place your savings and don’t mind the short-term lockup period, this endowment plan can be added to your list for consideration.

If you might need that sum of money within the next two years, this would not be the most ideal option.

If you’re looking at it for insurance coverage, this might be a little too basic for that.

Do ensure that you’re adequately covered by having policies that meet your insurance needs.

Do note that this plan is available on a limited tranche and is of a first-come, first-served basis.

Despite that, please do sufficient homework before diving into it, and also read through the terms and conditions carefully.

Please don’t get it just because you’re feeling the FOMO (fear of missing out).

Advertisement