Having children’s never easy, especially with Singapore’s high cost of living.

To mitigate some of the costs, our Government rolled out the Baby Bonus scheme: a scheme where cash rewards are given to encourage Singaporeans to have more children.

With the Baby Bonus, parents will need a Child Development Account (CDA) to receive grants and cash rewards from the government.

So you might be wondering…

How does the CDA work? Is there a way to optimise it?

We got you!

Here’s a quick guide on how to maximise your child’s CDA account and to get the most out of your Baby Bonus rewards!

Disclaimer: The information provided by Seedly serves as an educational piece and is not intended to be personalised financial advice. Readers should always do their own due diligence and consider their financial goals or engage a financial advisor before purchasing any financial products.

TL;DR: Baby Bonus Singapore Guide — Here’s How To Maximise Your Child’s CDA Account

- Open your CDA with a bank that offers high interest rates

- Max out the government’s dollar-for-dollar match

- Buy an Integrated Shield Plan that is MediSave-approved for your child

- Use your child’s CDA to pay for the bulk of his/her expenses

Want to discuss parenthood hacks to save money? You can do so on Seedly!

17 September 2021 Update: $200 Child Development Account Top-Up

As part of the Household Support Package announced at Budget 2021, all Singaporean children who are aged zero to six years old in the year 2021 will get a $200 CDA account top-up from mid-September 2021.

About 250,000 Singaporean children will be benefiting from this top-up.

In addition, Singaporean children who are aged 7-20 years in 2021 also received a $200 top-up to either their Edusave account or Post-Secondary Education Account (PSEA) in May 2021.

The $200 CDA account top-up will be directly deposited into your child’s CDA account from mid-September 2021 or after your child’s CDA account is open; whichever is later.

If you have yet to open a CDA account for your child, you will have to open it by 30 Jun 2022 in order for your child to receive the top-up.

If your child is eligible and has a CDA account, you will receive a notification informing you of the successful top-up.

What Is The Child Development Account (CDA)?

The CDA is a special savings account for children that can be opened with either POSB/DBS, OCBC or UOB to help build up the savings that can be spent on approved uses.

The CDA account comes under the Baby Bonus scheme, which is part of the Marriage and Parenthood Package.

Under this scheme, there’s a Baby Bonus Cash Gift component and a Baby Bonus CDA component.

What Does My Child Get For Opening A CDA Account?

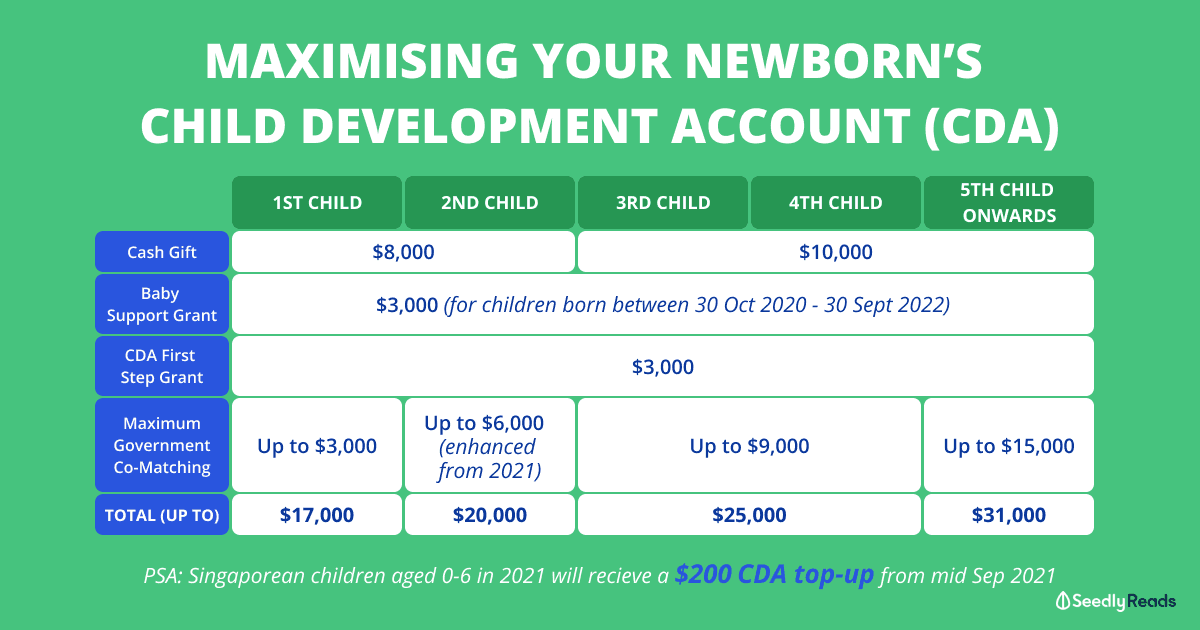

When you open a CDA account for your child, your child will receive the following benefits under the baby bonus scheme:

Baby Bonus Payout (1st Child) Payout (2nd Child) Payout (3rd, 4th Child) Payout (5th Child Onwards)

One-Off Baby Support Grant (Nuclear Family)

for Singaporean children born between 1 Oct 2020 & 30 Sep 2022$3,000

Cash Gift (Nuclear Family) $8,000 $8,000 $10,000 $10,000

CDA First Step Grant

(Nuclear Family + Unwed Parents)$3,000 $3,000 $3,000 $3,000

CDA Dollar-for-Dollar Matching

(Nuclear Family + Unwed Parents)$3,000 $6,000

(enhanced from Jan 2021 was $3,000)$9,000 $15,000

Total Up to $17,000 Up to $20,000 Up to $25,000 $31,000

Source: Ministry of Social and Family Development

Unfortunately, unwed parents (e.g. single parents) in Singapore are disqualified from the Baby Support Grant and the Baby Bonus Cash Gift Component as a whole.

Your child will only receive the First Step Grant and Dollar for Dollar Matching of Savings if they are deemed to be a nuclear family by the Ministry of Social and Family Development (MSF).

Here are the requirements:

- Your child is a Singapore Citizen; and

- The child’s parents are lawfully married.

Also, here are more details about the benefits.

1. Baby Bonus Cash Gift: $8,000 to $10,000 (Nuclear Family)

Parents who form nuclear families with their children can apply to receive the Baby Bonus Cash Gift for every child they have.

They can apply as early as eight weeks before the birth of their child.

The money, which is given in cold hard cash will be credited to the parents’ selected bank account and can be used without restrictions.

2. Baby Support Grant: $3,000 (Nuclear Family)

In addition, a one-off Baby Support Grant will be given to parents of children Singaporean children born between 1 Oct 2020 to 30 Sept 2022.

Also, parents of Singaporean babies born before 1 Oct 2020 with an estimated delivery date between 1 Oct 2020 to 30 Sept 2022 will now be eligible for the grant.

Each couple will get $3,000 for each child born during this time period.

The money will be credited into the same bank account which parents used to receive the Baby Bonus Cash Gift and will be credited from 1 Apr 2021, or within the first month of enrolment into the Baby Bonus Scheme; whichever is later.

You’ll be happy to know that there are no restrictions on the use of the Baby Support Grant.

For information on the Baby Support Grant and Baby Bonus Cash Gift amount, eligibility, and disbursement schedule for your child, please use this Baby Bonus Online Eligibility Check tool

3. CDA First Step Grant: $3,000 [(Nuclear Family + Unwed Parent(s)]

You will be getting $3,000 that will be deposited into your child’s CDA under the government’s CDA First Step Grant.

The good thing about this grant is that there is no initial deposit from parents required.

4. CDA Dollar-for-Dollar Matching of Savings: $3,000 – $15,000 (Nuclear Family + Unwed Parent(s)]

For those who didn’t know, the government also matches every dollar you save into your child’s CDA account.

Meaning if you deposit $3,000 into your child’s CDA account, the government will deposit $3,000 into the same account as well!

There are however caps on the dollar to dollar matching scheme depending on how many children you have.:

- First Child: Up to $3,000

- Second Child: Up to $6,000*

- Third and Fourth Child: Up to $9,000

- Fifth Child Onwards: Up to $15,000.

Also, MSF announced in end-February 2021 that the dollar-for-dollar matching cap for the second child has been increased to $6,000 from $3,000 previously.

Thus if your child is a Singaporean whose date of birth or estimated date of delivery (EDD), is on or after 1 January 2021; he/she will be eligible for the higher matching amount of $6,000.

How To Maximise Your Child’s CDA Account?

There are a few banks that you can choose to open a CDA account for your child.

It is wise to compare these different bank accounts so that you will choose one that reaps the highest interest rates for your child.

Check out our quick comparison of POSB, OCBC and UOB’s CDA accounts.

2. Max Out the Government’s Dollar-For-Dollar Match

As mentioned above, the government does dollar-for-dollar matching when you top up your child’s CDA account. Here’s the maximum you can top up to maximise this benefit:

Maximum Amount You Can Deposit To Receive Dollar-For-Dollar Matching Dollar-For-Dollar Matching By Government Total (Excluding Cash Gift and CDA First Step)

1st Child $3,000 $3,000 $6,000

2nd Child $6,000 ^$6,000

(increased from $3,000)$12,000

3rd, 4th Child $9,000 $9,000 $18,000

5th Child Onwards $15,000 $15,000 $30,000

^All Singapore Citizen children who are the second child, and whose date of birth or Estimated Date of Delivery is on or after 1 Jan 2021, will be eligible to receive the higher maximum amount of dollar-for-dollar matching.*Applicable to a child born from Jan 2015.

3. Buy an Integrated Shield Plan That Is Medisave-Approved for Your Child

An integrated shield plan is an add on to your MediShield Life insurance plan. It offers additional benefits from private insurers that can help cover large hospital bills and selected costly outpatient treatment.

Having your child covered at a young age is beneficial, as he/she will not be excluded from any pre-existing conditions. With the dollar-for-dollar matching, you are essentially only paying for half the premiums!

So why not use MediSave to pay for an Integrated Shield Plan?

Of course, your child will also receive his/her MediSave account with $4,000 given by the government.

While you can use your child’s MediSave pay for the integrated shield plan, it is much better to use his/her CDA account, as keeping your money in your MediSave account reaps you a higher interest rate (5%) as compared to the CDA account (2%).

4. Use your child’s CDA to pay for a bulk of his/her expenses

If you decide to max out the dollar-to-dollar matching scheme, you will be having $9,000 in your child’s CDA (assuming this is your 1st child).

Your child’s CDA can only be used in a list of approved expenses, some of which include:

- Paying for approved Childcare Centres and Kindergartens

- Medical-Related Expenses for your child

- Multi-Vitamins, health supplements

- Optic care, spectacles, and contact lenses for the child.

What Happens To My Child’s CDA Account After He/She Grows Up?

When your child turns 13, whatever money that was not used from his/her CDA account will be automatically transferred to their Post-Secondary Education Account (PSEA)!

This account can be used for their post-secondary related school activities.

Want to Learn How Fellow Parents Navigate the World of Parenthood?

You can check out the community at Seedly and participate in the lively discussion about parenthood and all things money!

Advertisement