Medishield Life: Premiums To Be Deferred for Some Policyholders Till End-December 2021 (Update!)

When it comes to health insurance, we’re pretty lucky as Singaporeans.

Because even if we don’t know anything about it and didn’t buy any of our own.

We’re all covered by MediShield Life.

A basic health insurance plan that protects all Singapore Residents against large hospital bills for life.

Regardless of age or health condition!

Recently, the MediShield Life Council announced that MediShield Life is undergoing a review to enhance its benefits.

But at the same time, premiums might increase.

Wondering how this affects you?

Let’s find out!

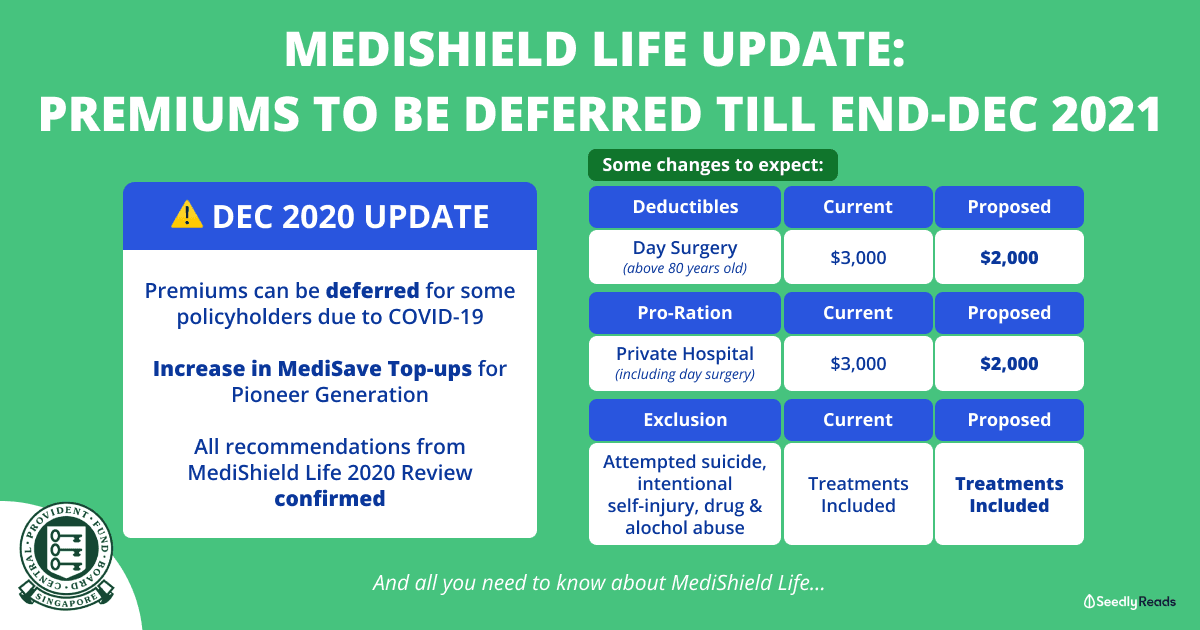

[Dec 2020 Update] MediShield Life Premiums for Some Policyholders To Be Deferred Till End-December 2021

Due to COVID-19, the Government will be deferring the MediShield Life premium payment for those who have insufficient MediSave balances.

As premiums are usually deducted at the start of the policy year (which varies depending on the date of renewal), they will be deferred to end-December 2021 instead.

In addition, there will be an increase in the yearly MediSave top-ups for the Pioneer Generation (those born in 1949 or earlier).

| MediSave Top-Ups (Now) | MediSave Top-Ups (from 2021) |

| S$200 to S$800 | S$250 to S$900 |

These measures are part of the aim to keep the net premium increases for Singaporeans to be within 10%, after the proposed changes from the MediShield Life Review mentioned that it would come with an increase in coverage and higher premiums.

The changes from the review have been confirmed and will be rolled out in March next year.

If you’re interested to find out what changes there will be from the MediShield Life Review, we explained it in detail below!

TL;DR: What to Expect From the MediShield Life 2020 Review

As part of MediShield Life Review 2020, a number of enhancements have been proposed to ensure that a greater proportion of subsidised medical bills are covered.

If you’re interested, you can read the Public Consultation Paper for the MediShield Life 2020 Review.

There are two key considerations for the recommendation:

- Provide effective protection against large subsidised bills

- Keep premiums affordable

Here’s a summary of what the MediShield Life Council is proposing:

- Changes to Claim Limits

- Changes to Deductibles

- Removal of Standard Exclusions

- Changes to Premiums

- Why the Increase in Premiums?

- Why Still Increase Premiums When Medishield Life Has So Much Reserves?

- How Will the Government Help With the Premium Increases?

- Further Support Due To COVID-19 Impact

Disclaimer: The Information provided by Seedly does not constitute an offer or solicitation to buy or sell any insurance product(s). It does not take into account the specific objectives or particular needs of any person. We strongly advise you to seek advice from a licensed insurance professional before purchasing any insurance products and/or services.

Changes to Claim Limits

Claim limits are to be reviewed to factor in inflation and medical advancements.

At a glance, here are the proposed changes to various claim limits:

Recommended Changes to MediSave Life Claim Limits | Current | Recommended |

|---|---|---|

| Inpatient Treatments | ||

| Daily Ward & Treatment Charges | ||

| Normal Ward | $700 per day | $800 per day (add claim limit of $200 per day for first 2 days) |

| ICU Ward | $1,200 per day | $2,200 per day (add claim limit of $200 per day for first 2 days) |

| Psychiatric | $100 per day (up to 35 days per policy year) | $160 per day (up to 60 days per policy year) |

| Stereotactic Radiosurgery | $4,800 per treatment course | $10,000 per treatment course |

| Community Hospital | ||

| Rehabilitative Care | $350 per day | $350 per day |

| Sub-acute Care | $430 per day | |

| Outpatient Treatments | ||

| Kidney Dialysis | $1,000 per month | $1,100 per month |

| Immunosuppressants for Organ Transplant | $200 per month | $550 per month |

| Radiotherapy for Cancer | ||

| External Radiotherapy (except Hemi-body) | $140 per treatment | $300 per treatment |

| Hemi-Body Radiotherapy | $900 per treatment | |

| Maximum Claim Limits | ||

| Claim Limit per Policy Year | $100,000 | $150,000 |

Higher Claim Limits for Daily Ward and Treatment Charges for First 2 Days of Acute Hospital Stay

The current claim limit for daily ward and treatment charges are $700 per day.

And $1,200 for an Intensive Care Unit (ICU) ward.

The Council would like for both limits to be increased.

At the same time, the Council also recognises that higher charges tend to be incurred during the first 2 days of hospital stay — due to medical tests and diagnostics.

The introduction of higher claim limits for the first 2 days will help better cover short stays.

Introduce Treatment-Specific Claim Limits for Community Hospital Care & Outpatient Radiotherapy

The current claim limit is $350 per day for both rehabilitative and sub-acute care in community hospitals.

However, sub-acute care is costlier as it involves the treatment of complicated medical conditions.

Therefore, the proposed increment to $430 per day for sub-acute care would improve this area of coverage.

And also improve coverage of the costlier types of outpatient radiotherapy treatments.

Increase in Annual Claim Limit from $100,000 to $150,000

This would better protect Singaporeans from exceptionally large bills.

Due to long or multiple hospitalisations throughout the year.

This claim limit would be sufficient for a lot more patients, and this amount is considered alongside the increase in premiums.

Changes to Deductibles

Lower Deductible for Day Surgeries for Older Patients

The deductible for day surgery patients above 80 years old can be lowered from $3,000 to $2,000.

This is in line with the deductible for inpatient stays in C-class wards.

Doing so gives patients the choice to choose either a day surgery or an inpatient stay — since both are subjected to the same deductible.

Lower Pro-Ration Factor for Private Hospitals

Even if you seek treatment at a private hospital, you can still make claims through MediShield Life.

As MediShield Life payouts are usually pegged to subsidised public hospitals bills.

Private hospital stays are pro-rated by 35% to make them more comparable to a subsidised public hospital bill, before the MediShield Life payout is calculated.

For example, if you currently have a $10,000 private hospital bill.

Your MediShield payout will be computed as if the bill is $3,500.

The Council recognises that the pro-ration is insufficient to bring private hospital bills down to subsidised public hospital bill levels.

To allow greater fairness between subsidised and private patients, it recommends the pro-ration factor to be reduced to 25% instead.

This ensures similar level of payouts between subsidised and private patients receiving the same treatments.

So that same $10,000 private hospital bill, will now be pro-rated to $2,500 instead.

Removal of Standard Exclusions

Treatments Arising from Attempted Suicide, Intentional Self-Injury, Drug Addiction, and Alcoholism

Currently, there are standard exclusions for treatments due to:

- attempted suicide

- intentional self-injury

- drug and alcohol abuse

The Council recognises that these types of treatments can help support individuals to recover or overcome their addictions.

And it proposes the removal such standard exclusions.

Changes to Premiums

With all of these proposed benefit enhancements.

As well as the need to keep up with evolving medical practices and healthcare cost inflation.

It’s a given that premiums will increase in order to keep MediShield Life sustainable.

| Age at Next Birthday | Current Premiums (before subsidies) | Proposed Premiums (before subsidies) | Increase |

|---|---|---|---|

| 1 - 20 | $130 | $145 | 11.5% |

| 21 - 30 | $195 | $250 | 28.2% |

| 31 - 40 | $310 | $390 | 25.8% |

| 41 - 50 | $435 | $525 | 20.7% |

| 51 - 60 | $630 | $800 | 27.0% |

| 61 - 65 | $755 | $1,020 | 35.1% |

| 66 - 70 | $815 | $1,100 | 35.0% |

| 71 - 73 | $885 | $1,195 | 35.0% |

| 74 - 75 | $975 | $1,320 | 35.4% |

| 76 - 78 | $1,130 | $1,530 | 35.4% |

| 79 - 80 | $1,175 | $1,590 | 35.3% |

| 81 - 83 | $1,250 | $1,675 | 34.0% |

| 84 - 85 | $1,430 | $1,935 | 35.3% |

| 86 - 90 | $1,500 | $2,025 | 35.0% |

| More than 90 | $1,530 | $2,055 | 34.3% |

Why the Increase in Premiums?

There are mainly three key drivers of the premium increases.

One of them is due to increase in claim limits as mentioned above, to allow Singaporeans to continue to be adequately covered for the bulk of subsidised medical bills.

This accounts for one-quarter of the premium increase.

Another would be due to benefit enhancements, including those that were implemented since 2018.

This includes the extension of coverage to inpatient hospices and serious pregnancy complications.

Last but not least, the support in the increase in ultilisation and payout of Medishield Life accounts for two-third of the premium increase.

Since the launch of Medishield Life, the number of claimants have increase by about 30%, and the annual payouts have increased by about 40% over the last four years.

The average hospitalisation bill size in public healthcare institutions has increased by an average of 6% a year between 2001 and 2019.

This increase can be attributed to medical cost inflation, medical advancements as well as our demographics over the years.

Why Still Increase Premiums When Medishield Life Has So Much Reserves?

A total of S$7.5 billion in premiums were collected from 2016 to 2019.

This includes S$3.1 billion (40%) collected from the Government in terms of premium subsidies and other forms of premium support provided to keep premiums affordable.

There were also a total of S$3.5 billion in claims that were paid out, and S$3 billion was set aside for future premium rebates.

Reserves are also meant for rainy days and for Singaporeans’ future benefits.

They also help to ensure that MediShield Life is self-sustaining and can continue to pay out claims during unforeseen events, providing a buffer against unforeseen circumstances such as a sudden surge in claims during disease outbreaks.

In addition, reserves are computed by external professional actuaries in accordance with the Monetary Authority of Singapore (MAS)’s requirements and is in line with industry standards.

MediShield Life is a not-for-profit Scheme.

How Will the Government Help With the Premium Increases?

The Government has committed about $2.2 billion for premium subsidies and support over the next 3 years to help Singapore Residents cope with the increase in premiums.

There are premium subsidies of up to 50% for lower and middle-income households.

All Merdeka Generation seniors receive additional subsidies of up to 10%.

All Pioneer Generation seniors receive special subsidies of up to 60%.

The Council has also taken into account that the total household premiums (because some are using their own MediSave to pay for their dependants) after subsidies are within MediSave contributions and inflows for most households.

There is also Additional Premium Support for the needy who are unable to afford their premiums even after Government subsidies and limited family support.

So overall, no one will lose their MediShield Life coverage after this review.

Further Support Due To COVID-19 Impact

To further help Singaporeans during this exceptional period, the Government has provided additional a COVID-19 subsidy for all Singaporeans during the next two years.

This subsidy will cover 70% of the net premium increase in the first year, and 30% of the net premium increase the second year.

As such, the net increase for all Singaporeans will be no more than about 10% in the first year after this review is implemented.

What Is MediShield Life?

MediShield Life is a basic health insurance plan, which all Singaporeans and Singaporean PRs are automatically enrolled in.

It was an initiative launched in November 2015 to replace MediShield.

Which helps you to pay for large medical bills and even certain types of outpatient treatment like dialysis or chemotherapy.

At a glance, MediShield Life offers:

- Better protection and higher payouts, so you pass less MediSave or cash

- Lifetime protection including pre-existing conditions

What Are the Benefits of MediShield Life?

While coverage is not as extensive as other health insurance schemes, here is what is covered under MediShield Life:

| Claim Limits | |

|---|---|

| Inpatient / Day Surgery | |

| Daily Ward and Treatment Charges: Normal Ward | $800/day |

| Intensive Care Unit Ward | $2,200/day |

| Community Hospital | $350/day |

| Psychiatric | $160/day |

| Surgical Procedures: Less Complex to More Complex Procedures | $240- $2,600 |

| Implants | $7,000 per treatment |

| Radiosurgery | $10,000 per procedure |

| Continuation of Bone Marrow Transplant Treatment For Multiple Myeloma | $6,000 per treatment |

| Outpatient Treatments | |

| Chemotherapy For Cancer | $3,000 per month |

| Radiotherapy For Cancer | $300-$1,800 per treatment |

| Kidney Dialysis | $1,100 per month |

| Immunosuppressants for Organ Transplant | $550 per month |

| Erythropoietin for Chronic Kidney Failure | $200 per month |

| Long Term Parenteral Nutrition | $200/month |

| Maximum Claim Limits | |

| Per Policy Year | $150,000 |

| Lifetime | No Limit |

Source: Ministry Of Health Singapore

How Much Can I Claim Under MediShield Life?

There are 3 ways you can claim your hospital bill under MediShield Life:

| MediShield Life Claim Limit | Deductibles | Insurance Co-payment |

|---|---|---|

| There is an annual claim limit of $100,000 per year. | Depending on your age, there is a deductible amount you have to pay each year before you can activate MediShield Life. For those below the age of 80, you have to pay ~ $1,500 - $2,000. Those age 81 and above will have to pay $2,000 - $3,000. If you were hospitalised once and paid the full deductible, you don't have to pay it again if you are hospitalised again in the same year. | This is the percentage of the claimable amount that you have to pay. After paying your deductible, you will have to pay your co-payment as well! |

Co-Insurance Claims and Payments

| Claimable Amount For Inpatient And Day Surgery | Co-Insurance (% if Claimable Amount) |

|---|---|

| $0-$5,000 | 10% |

| $5,001-$10,000 | 5% |

| >$10,000 | 3% |

| Co-Insurance For All Outpatient Treatments | 10% |

How Much Do I Have To Pay For MediShield Life?

To minimise cash payment, you may use your MediSave to pay for your MediShield Life premiums in full.

If you’d like to, you can also use your MediSave to help pay the MediShield Life premiums of your immediate family members.

For lower- to middle- income families who have difficulties paying the premiums, there are many government subsidies and MediSave top-ups to help ensure that you are adequately covered.

For those who are needy and are unable to pay their share of premiums even after subsidies.

The Government offers Additional Premium Support to help you with the premium payments.

if you’d like to find out more about your premiums payable as well as the types of subsidies which you might be eligible for.

You can use the MediShield Life premium calculator to find out.

Is Having MediShield Life Enough?

MediShield Life is a really basic health insurance that is meant to help most Singapore Residents to defray their medical costs.

Whether the coverage is sufficient…

That’s highly dependent on your needs.

For example, if you were hospitalised, MediShield Life will give you enough payouts to cover the cost of Class C or B2 wards at public hospitals.

But if you’d like to enjoy greater flexibility with regard to:

- the types of wards you can stay in

- the types of treatments you want

then you might want to opt for an Integrated Shield Plan (IP) to enhance your MediShield Life coverage so you can have more options!

Advertisement