Moving Out From Your Parents’ Home in Your 20s - What You Need to Consider

Seedly

Seedly●

For many Singaporeans, moving out at 18 is not the norm. After all, rent is expensive, space is limited, and staying with your family can help you save significantly more money.

Still, moving out of your parents’ home may be necessary for various reasons. Perhaps you need your own space, want greater independence or need to leave a difficult home environment.

Whatever your reason, learning how to move out of your parents’ house involves more than finding a room and packing your belongings. More importantly, you need to understand the upfront costs, monthly expenses and lifestyle changes that come with living independently.

Although living alone can be rewarding, it can also place considerable pressure on your finances. Therefore, before you sign a tenancy agreement, here is what you should consider.

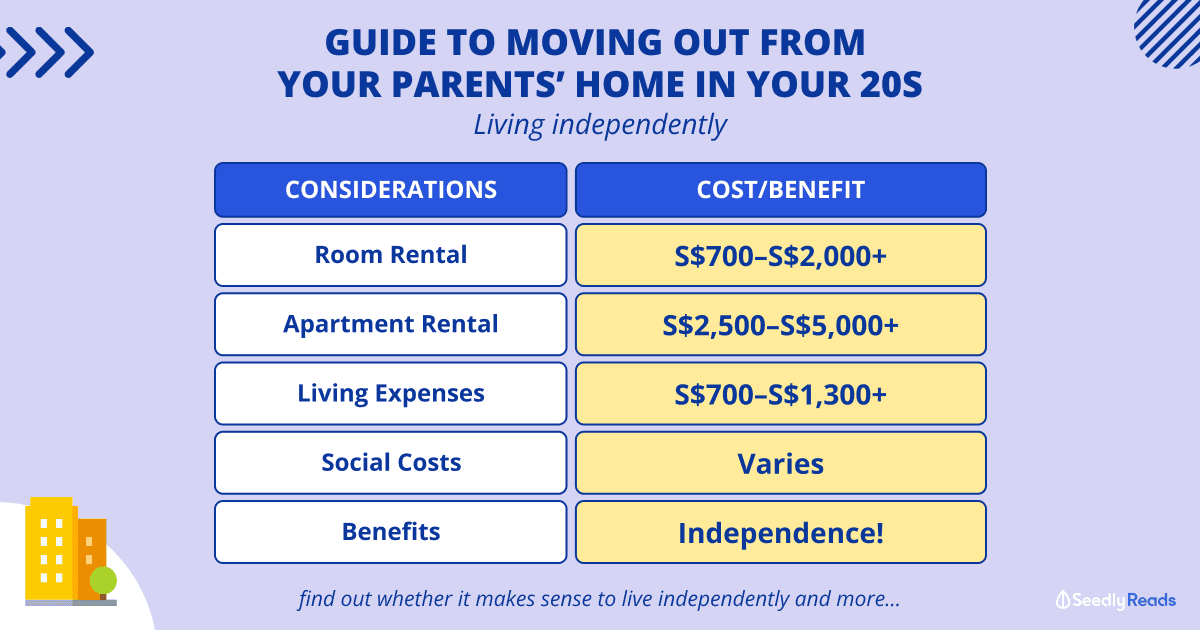

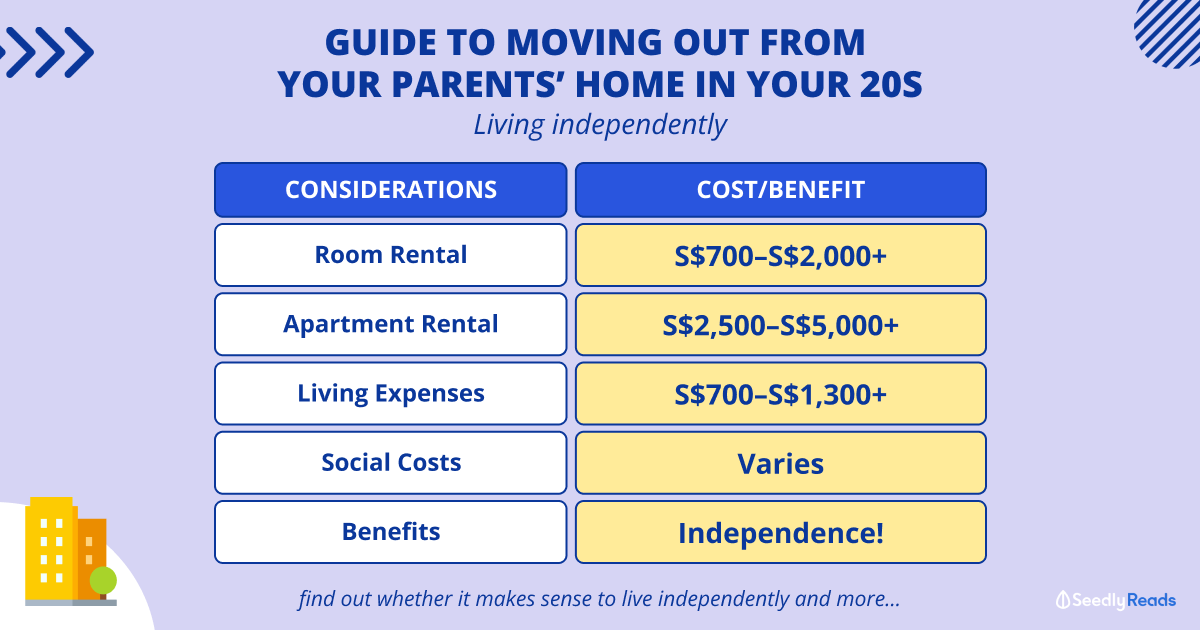

TL;DR: Guide to Moving Out of Your Parents’ Home in Your 20s

Financial Costs of Living Independently

For most people, cost is the biggest obstacle to moving out of their parents’ home.

If you are below 35 and buying a home is not currently an option, you will usually have to consider renting a room, renting an apartment with housemates or staying in a co-living development.

On the other hand, singles aged 35 and above may have additional housing options. For example, eligible singles can apply for a new 2-room Flexi flat or purchase an HDB resale flat. However, buying comes with a very different set of financial commitments, so you should obtain an HDB Flat Eligibility letter and calculate what you can comfortably afford first.

If renting is your preferred option, start by building a realistic budget for moving out of your parents’ house. Besides monthly rent, remember to include deposits, stamp duty, utilities, food, transport and household supplies.

Renting a Room

Renting a room is usually one of the more affordable ways to move out of your parents’ house in Singapore.

However, there is no single reliable rental range that applies across the country. A common room in an HDB flat outside the central area, for instance, may cost substantially less than a master bedroom near an MRT interchange or within the city.

Therefore, rather than relying on an advertised nationwide average, check recent market transactions for the particular town or development you are considering. HDB provides a market-rent enquiry service for approved whole-flat rentals, while URA publishes information on private residential rental contracts.

Additionally, check exactly what the rent includes. Some landlords include Wi-Fi, utilities and weekly cleaning. Others may charge you separately or impose a monthly utility cap.

Price is not the only consideration either. Since you will be sharing common spaces, your housemates and landlord can have a major impact on your quality of life.

Before committing, meet them where possible and ask practical questions such as:

- How are household chores divided?

- Are visitors allowed?

- Can you cook regularly?

- Is air-conditioning usage restricted?

- Are there quiet hours?

- How are utility bills divided?

- Will the landlord be staying in the unit?

- What happens if an appliance breaks down?

Furthermore, make sure the landlord has obtained the necessary approval to rent out the HDB flat or bedroom. HDB tenancies must generally last at least six months.

Renting an Apartment

If your budget is higher, renting an entire apartment gives you greater privacy and control over your space.

However, apartment rentals can vary considerably according to location, floor area, property age, furnishing and proximity to public transport. As a result, an old studio outside the city and a newly completed one-bedroom condominium near the CBD should not be treated as comparable options.

For a more accurate estimate, search URA’s database of actual private residential rental contracts. You can review transactions by project, postal district and property type instead of relying only on asking prices shown in property listings.

Alternatively, you could rent a larger unit with trusted friends and divide the cost. This may lower each person’s share of the rent. Nevertheless, you should agree on responsibilities before moving in together.

For example, discuss how you will split utilities, groceries, cleaning products and repair costs. You should also decide what happens if one housemate wants to move out before the lease ends.

Do note that private residential properties cannot legally be rented for stays of fewer than three consecutive months. Therefore, avoid informal short-term arrangements that do not comply with Singapore’s residential rental rules.

Living Expenses

Rent will probably be your largest expense. Even so, it is far from the only cost of moving out of your parents’ home.

Before signing anything, calculate both your upfront moving costs and your recurring monthly expenses.

Upfront Deposit

A landlord may ask for a security deposit to cover unpaid rent, damage or other breaches of the tenancy agreement.

Although people commonly refer to one or two months of rent, the amount is not fixed by a universal statutory formula. Instead, it depends on what you and the landlord agree to include in the tenancy agreement.

Therefore, check:

- The exact deposit amount

- When the deposit must be paid

- The circumstances under which deductions may be made

- Who is responsible for minor repairs

- When the remaining deposit must be returned

- Whether photographs and an inventory list will be recorded during handover

In addition, avoid transferring money before verifying the property, landlord and agent.

If an estate agent is involved, check that the person is registered through the Council for Estate Agencies’ Public Register. You can also use CEA’s tenancy agreement templates as a reference when reviewing the lease.

Stamp Duty and Other Upfront Costs

Besides the deposit, you may have to pay stamp duty on the tenancy agreement.

Stamp duty is calculated using the contractual rent or market rent, whichever is higher. The tenancy agreement should state who is responsible for paying it. If it does not, the tenant is generally the party liable.

Additionally, your upfront moving budget may need to cover:

- Advance rent

- Moving or delivery services

- Agent commission, where applicable

- Utility account charges

- Broadband installation

- Furniture and appliances

- Curtains, bedding and kitchenware

- Cleaning supplies

- Minor repairs or replacement items

Consequently, your upfront cash requirement can be much higher than one month’s rent.

Cost of Appliances, Furniture and Repairs

The amount you need for furniture and appliances depends heavily on whether the property is fully furnished, partially furnished or unfurnished.

For example, a fully furnished room may already include a bed, wardrobe, desk and air-conditioning. In contrast, an unfurnished apartment may require you to purchase major items such as a refrigerator, washing machine, bed and dining table.

Before moving in, request an inventory list and test the appliances. Moreover, take photographs or videos of the property’s condition during the handover. This gives both you and the landlord a clearer record if a dispute arises later.

Rather than immediately buying everything new, you could consider second-hand furniture, refurbished appliances or items from family members. However, check measurements first because delivery, disposal and assembly fees can add up.

Most importantly, maintain an emergency fund. As a general guide, aim to keep at least three to six months of essential expenses available. If your income is irregular, you may need a larger buffer.

Bills

Free Wi-Fi and utilities are no longer guaranteed once you move out.

Depending on your tenancy, you may need to pay for:

- Electricity

- Water

- Gas

- Refuse collection

- Broadband

- Mobile service

- Air-conditioning servicing

- Streaming subscriptions

Electricity costs can also change every quarter. For July to September 2026, the regulated household electricity tariff is 31.91 cents per kWh before GST, or 34.78 cents per kWh after GST.

However, your total bill will depend more on your usage than the flat type alone. Air-conditioning, water heaters, clothes dryers and frequent cooking can significantly increase consumption.

Meanwhile, advertised fibre broadband plans currently start from around S$30 per month, although the final amount depends on the contract, router, installation fees and post-promotional price.

As a starting point, set aside approximately S$120 to S$220 per month for utilities, broadband and household subscriptions if you are paying them yourself. Nevertheless, treat this only as a planning range. Someone renting a room with utilities included could spend much less, while a person living alone and using air-conditioning daily could spend more.

To lower your bills, compare electricity purchase options through EMA’s official comparison service and choose energy-efficient appliances where practical.

You may also consider a cashback card for recurring household expenses. For instance, the UOB One Credit Card offers additional cashback on eligible Singapore Power utility transactions when you meet its quarterly cashback requirements.

As of July 2026, eligible new-to-UOB applicants applying through SingSaver can receive S$60 Cash via PayNow after spending at least S$500 within 30 days of card approval. The offer is subject to SingSaver’s promotion terms and ends on 31 July 2026.

However, do not apply for a card solely for the sign-up reward. First, make sure you can consistently meet its spending requirements without buying things you do not need. Otherwise, a simpler no-minimum-spend cashback card or GIRO arrangement may suit you better.

Food

Once you move out, food can become one of your largest variable expenses.

Cooking regularly will generally give you more control over your spending. However, cooking for one is not always automatically cheaper, especially if ingredients go unused or you frequently buy specialised items.

Therefore, estimate your food budget based on your actual routine. Consider:

- How many meals you eat at home

- How often you order food delivery

- Whether lunch is subsidised at work

- Your dietary requirements

- Whether groceries are shared with housemates

- How much food you usually waste

For a conservative starting point, you might allocate around S$400 to S$700 per month for groceries, hawker meals, food delivery and occasional dining out. Still, your actual figure may sit outside this range.

One useful approach is to track your food spending for one or two months before moving. Then, add a buffer because you will no longer be able to rely on meals and household groceries purchased by your family.

Entertainment

Living independently does not mean eliminating every enjoyable activity from your budget.

Instead, set a realistic discretionary allowance for concerts, nights out, hobbies, gaming, streaming services and other activities.

Rather than using a fixed S$200 target, decide how much you can spend after covering rent, essentials, insurance, savings and debt repayments.

For example, you could separate your entertainment budget into:

- A monthly social budget

- An annual concert or travel fund

- A subscription budget

- A guilt-free personal spending allowance

This makes it easier to enjoy yourself without accidentally using money intended for rent or emergency savings.

Overall, a single renter could easily spend approximately S$700 to S$1,300 per month on non-rent expenses, depending on food, transport, utilities and lifestyle choices.

However, do not treat this as a universal amount. Build your own budget using your bank and card transactions from the past three months. Then, add the expenses your parents currently absorb, such as utilities, groceries, household supplies and internet service.

Social Costs

Financial costs are only one part of living independently.

Unless you move in with close friends, you may be living alone or with people you do not know well. Consequently, you may need to put more effort into maintaining relationships and building a healthy routine.

At first, having complete privacy may feel liberating. No one will ask where you are going, what time you will be home or why you are still awake at 3 a.m.

However, living alone can also feel isolating. Therefore, make time to meet friends, speak to family members you trust and take part in activities outside your home.

If you live with housemates, compatibility becomes just as important. Different expectations around cleanliness, noise, visitors and shared items can quickly create tension.

For that reason, discuss house rules early rather than waiting for a disagreement. Furthermore, put important arrangements in writing, particularly when money is involved.

Benefits of Living Independently

Once you account for the costs, living independently can still offer meaningful benefits.

First, you gain greater freedom over your routine and environment. You can decide when to sleep, what to eat, how to decorate your space and who may visit.

At the same time, that freedom comes with responsibility. No one else will automatically clean the bathroom, replace household supplies, arrange repairs or make sure the bills are paid.

Second, living independently can give you a stronger sense of confidence. Once you learn to manage a household, solve problems and keep within your budget, you may feel more capable of handling other areas of adulthood.

Finally, moving out forces you to understand your personal finances more clearly. Expenses that were previously invisible—such as electricity, cleaning products and appliance repairs—suddenly become part of your monthly budget.

As a result, you may become more deliberate about saving, spending and planning ahead.

Should You Move Out and Live Independently in Your 20s?

Ultimately, whether you should move out depends on your financial position, family circumstances and personal priorities.

For someone living in an unsafe or highly distressing home environment, the emotional and personal benefits of moving may outweigh the financial cost. In that situation, consider speaking to someone you trust and researching the support or housing options available to you.

Meanwhile, if your main goal is independence, ask yourself whether moving out now is worth delaying other goals such as building an emergency fund, furthering your education or purchasing a home.

Before committing, run through the following checks:

- Can you pay the deposit, stamp duty and moving expenses without borrowing?

- Can you afford the rent while still saving every month?

- Do you have at least three to six months of essential expenses saved?

- Have you accounted for food, transport, insurance and utility bills?

- Have you checked the landlord, agent and rental approval?

- Have you read the tenancy agreement carefully?

- Can you continue paying the rent if your income falls temporarily?

- Are you prepared for the household and social responsibilities?

If the numbers are too tight, you do not have to abandon the idea completely. Instead, you could rent a room rather than an entire unit, share with trusted housemates or delay the move while building a larger cash buffer.

Moving out of your parents’ home can be expensive. Nevertheless, with a proper budget and realistic expectations, it can also be a valuable step towards greater independence.

Advertisement