Is it an outright scam?

The answer is no (at least not outright) – but there are serious financial risks to consider.

Also, it’s something of a legal grey area. Here’s how it works:

Note: Special thanks To Douglas Chow for his help; you can call him the Chief Enlightenment Officer (CEO) of Empower Advisory.

What do the ads mean by “owning 20 properties”?

When the ads say “own”, what they really mean is co-ownership of several managed properties.

These schemes rely on getting a group of investors to pool their money together, and buy up a range of properties (mainly commercial, for reasons we’ll explain below).

The money from investors is then handled by a manager (or group of managers), who choose which properties to buy with the money. Rental income from the properties is then shared out among the different investors. The managers are typically paid with a cut of the total revenue generated by the properties (but the method and amount of payment can vary between the different groups).

This is what the ads really mean when they claim you “own” the group of properties. It doesn’t mean that you can take reverse mortgages on those properties, or will the actual buildings to your children. The only real benefit you’re receiving is the rental income.

As for the “no cash down” part, this is true in the sense that you don’t make down payment on any of the properties. But of course, you need to commit your cash to the scheme. This is usually on a monthly basis, but can sometimes include upfront payments or other “administrative fees”.

Now if you’re savvy about the property market and various investment schemes, you’ll be saying…

Hang on, this sounds like a REIT

Spot on! In principle, these schemes operate similarly to a Real Estate Investment Trust (REIT).

However, they differ in many substantial ways. Chief among them is the fact that REITs are listed and hence regulated, but these schemes could be…let’s just say “more loosely run”. We’re not saying they’re all scams. But there are fewer watchdogs to keep them in line.

It’s also a legal grey area, whether these schemes should be allowed to operate as a REIT without the pertinent licenses.

We do expect that the government will come around to clarify things. At the time of writing, however, these schemes are not illegal.

Why do these schemes mainly involve commercial properties?

The two main reasons are:

- There is no Additional Buyers Stamp Duty (ABSD) for commercial properties.

There is still a Goods and Services Tax (GST), but this is much lower than the ABSD. - Commercial properties provide higher yields than residential counterparts.

In the current market, residential units are hovering at rental yields of around two to three per cent. Commercial properties reach between three to five per cent.

In particular, old commercial properties have very high rental yields – sometimes exceeding seven per cent. This is due to their low overall cost (from an expiring lease), coupled with rental income that is unaffected by the lease (tenants don’t care about the remaining lease).

Also note that, if borrowing is involved, the LTV for commercial properties is much higher. For example, you may have seen bank ads offering up to 120 per cent LTV (although that is actually a combination of a Working Capital Loan plus the property loan). Financing is thus easier for commercial properties.

Finally, just as we like to do with residential properties, commercial property investors like to bank on the chances of en-bloc sales.

Overall, it does make good sense for these schemes to go for commercial rather than residential properties. But this can also be a drawback to regular investors, who don’t understand such properties (see below).

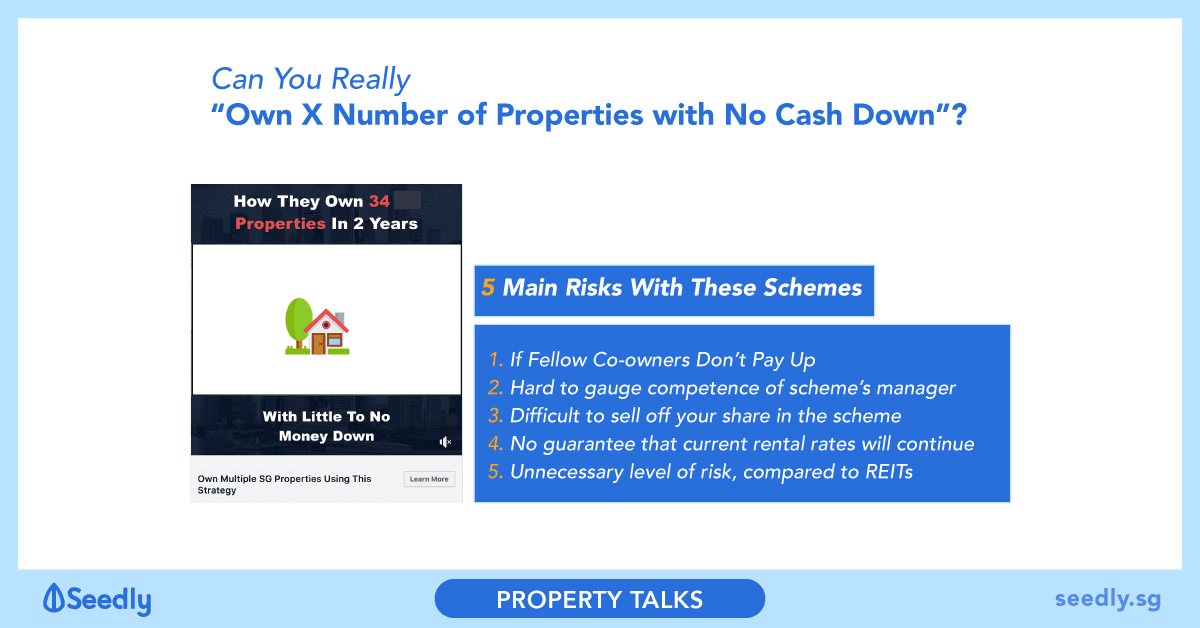

What are the main issues with these schemes?

As we’re not Financial Advisors, we’re in no position to advise you for or against these schemes. But we can point out some key concerns, from a property perspective:

- You have to consider the consequences if fellow co-owners don’t pay up (if loans are involved)

- Regular investors find it hard to gauge the competence of the scheme’s manager(s)

- It’s difficult to sell off your share of the scheme

- There’s no guarantee that current rental rates will continue

- The schemes may add an unnecessary level of risk, compared to just buying regular REITs

1. You have to consider the consequences if fellow co-owners don’t pay up (if loans are involved)

Not all the schemes use the financing to buy properties. Some of them just buy the properties in cash, in which case there’s little risk of rising interest rates, defaults, etc.

But if there are loans involved, you need to ask what happens if some of your co-owners decide to stop paying. Will you be left to pick up the slack? Or will the entire scheme just wash out like a sandcastle at high tide?

The legal consequences can be complex where loans are involved, and you should check the terms and conditions with a legal professional.

Even if there are no loans involved, you need to know what will happen to your money if the scheme is dissolved for some reason (e.g. the manager messes up and the properties start generating high losses).

These issues pose a serious financial risk, and you should consult a financial planner/wealth manager before you even consider them.

2. Regular investors find it hard to gauge the competence of the scheme’s manager(s)

This is often marketed as a plus point: the scheme will tell you it’s better to let an expert manage the property, as you know nothing about it yourself.

But how do you gauge an expert if you’re not an expert yourself? For all you know, the “expert” could be someone who failed their way out of a proper REIT. Even if you can look up, say, the managers’ 15-year track record (usually you can’t), would you really understand how to gauge their performance?

And remember that, if the managers mess up and the scheme implodes, they don’t have to pay you back one cent of their fees. It’s your money they’re playing with.

3. It’s difficult to sell off your share in the scheme

These are not stocks, which you can quickly sell off by tapping parts of your phone screen. If you want to pull out of the scheme, you need to find someone to buy over your share.

You’ll really need a property agent then. To sell your house, that is, because there’s probably no way to get out of this if the scheme starts falling apart (who is going to buy over a share of a collapsing property scheme?)

4. There’s no guarantee that current rental rates will continue

Be aware that the attractive rental yields right now may not continue.

In retail, stores are increasingly moving to e-commerce. In business, a growing number of companies are opting for co-working spaces, rather than three-year leases in conventional offices. Meanwhile, slowdowns in the global economy will take their toll on logistics and manufacturing – this will impact rental yields for warehouses and factories.

In short, rents can go down, and vacancies can increase. Take a long term view of the market, and don’t be dazzled by rental yields at the present.

5. The schemes add an unnecessary level of risk, compared to just buying regular REITs

This is the biggest and most important question:

Short of less protection, what do you get from buying into these schemes, rather than, say, a better regulated REIT? The two operate the same way, but a commercial REIT is more highly capitalised, has a more transparent track record, and is easier to buy or sell.

Again, talk it over with a financial advisor before buying.

This article first appeared on 99.co and is part of a content syndication agreement between 99.co and Seedly.

For our Property Talks, the Seedly team worked closely with 99.co, who is an expert in the field, to curate unbiased, non-sponsored content to add value back to our readers.

99.co is a Singapore-based property portal that aims to take away the tedious bits of property hunting.

If you have any questions regarding property, feel free to discuss them with the friendly Seedly Community!