P2P Lending in Singapore Comparison (Investors): BRDGE vs Capital Match vs Funding Societies vs Minterest vs MoolahSense

1 February 2021 Update: CAD and MAS Launch Joint Investigation Into CoAssets Group & CA Funding

Do read all about it here! We have thus updated the article and removed CA Funding from this comparison.

Recently, I have been hooked on South Korean Drama Start-Up due to its combination of good story, convincing acting, humour and compelling themes of youth, aspirations, and entrepreneurship.

Not to mention that drama’s start-up setting which helped me relate to the drama more.

Arguably, the biggest star to have emerged from the show is fan favourite Han Ji-Pyeong (played by Kim Seon-ho).

In the show, Han Ji-Pyeong plays the role of team lead at SH Capital: a fictional venture capital firm based in South Korea.

Although his selection process is brutal, he is in a sense helping people fulfil their dreams of entrepreneurship.

As we can’t all become Venture Capitalist investors, there is something else you can consider.

However, there is a way you still can help people start or maintain their own businesses.

You can actually provide unsecured loans to entrepreneurs in Singapore and the region through Peer-to-Peer (P2P) lending platforms, and receive interest on the funds you put in.

This alternative form of investing is undoubtedly exciting. But, it comes quite a bit of risk as well.

If you are interested and wondering which is the best P2P lending platform in Singapore; we got you!

Here is a detailed comparison of the six main players (correct as of 15 Dec 2020) in the Singapore P2P lending market.

Disclaimer: P2P investing is a high-risk investment. The information provided by Seedly serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any investment product.

TL;DR: Ultimate P2P Lending in Singapore to Businesses Comparison: BRDGE vs Moolahsense vs Funding Societies vs CA Funding vs Capital Match vs Minterest

| Company | Weighted Average Rate of Returns (Per Annum) | Default Rate (As at 31 December 2019)* | Loan Tenure | Fees | Entry | Types of P2P Investment Products | Safety Net (Fund Handling Custodian) |

|---|---|---|---|---|---|---|---|

| BRDGE (Formerly SeedIn) | 2017: 7.89% 2018: 8.33% 2019: 9.86% | 2017: 0% 2018: 0.47% 2019: 0% | 1 - 12 months | 15% (on interest earned) | $1,000 per campaign | Business Term | OCBC Bank |

| Capital Match | 2020: 11.14% | 2020: 0.05% | 3 - 12 months | 20% (on interest earned) | $1,000 per campaign (initial deposit $1,000) | Business Term Loans & Invoice Financing | Watiga Trust (Escrow agency) |

| CA Funding (Formerly CoAssets) | 2017: 8.04% 2018: 9.91% 2019: 14.01% | 2017: 2.2% 2018: 0% 2019: 0% | 3 - 36 months | 0% (on investors) | $1,000 per campaign | Business Term Loans & Invoice Financing | Vistra Trust (Escrow agency) |

| Funding Societies | 2017: 16.21% 2018: 11.73% 2019: 9.82% | 2017: 0.08% 2018: 0% 2019: 1.89% | 1 - 12 months | Service Fee: 18% on interest earned (Inclusive of GST) | $20 per campaign (initial deposit $100) | Business Term Loans & Invoice Financing | Vistra Trust (Escrow agency) |

| Minterest | 2017: 14.44% 2018: 7.53% 2019: 6.26% | 2017: 0% 2018: 0.68% 2019: 1.73% | Up to 12 months | 15% (on interest earned) | $50 per campaign (initial deposit $1,000) | Business Term Loans & Invoice Financing | Vistra Trust (Escrow agency) |

| MoolahSense | 2017: 9.73% 2018: 9.9% 2019: 8.78% | 2017: 4.46% 2018: 13.64% 2019: 20.33% | 15 days - 24 months | 1% (on all repayments) | $100 per campaign (initial deposit $1,000) | Business Term Loans & Invoice Financing | Funds held separately with OCBC Bank |

What is P2P Lending?

Well, I’m glad you asked!

P2P lending/peer-to-peer lending to businesses/lending-based crowdfunding by businesses refers broadly to a fundraising model where many persons lend sums of money to a company.

In return, the company enters into a legally binding commitment with the lenders to repay the loan at pre-determined time intervals and interest rates.

The lending is typically conducted through the online platforms discussed in the comparison.

Peer-to-peer (P2P) Crowdfunding Platforms: Solving Issues with SME Loans

At its core, P2P lending platforms were set up to solve one main problem faced by small businesses that are just starting up – funding.

Banks are reluctant to give loans to these small business due to concerns like:

- The lack of collateral (necessary for bank loans)

- Short credit history (which makes banks reluctant to loan)

- Imperfect financial record

- Long processing time

With peer-to-peer lending platforms, small businesses now have another option to turn to when they are looking for funding.

How Do Peer-to-Peer Crowdfunding Platforms Work?

But you might be wondering…

How do P2P lending platforms work?

Here’s an infographic explaining the whole process:

- P2P lending platforms are the bridge that connects the public to businesses in need of funding.

- Public investors can lend money to these businesses and get returns based on interest rates when borrowers repay the loans.

Pros and Cons of investing in P2P Lending in Singapore

Now that you know a bit more about how P2P lending works, the next thing you would want to consider are the Pros and Cons of this alternative investment.

Pros

- Low Barrier of Entry: Low investment commitment (minimum investment of S$100, or less for some platforms)

- Diversification: Alternative investment products to diversify your portfolio

- Returns: Attractive returns of more than 10% usually (higher than inflation)

- Monthly Returns: Investment principal with interest earned returned to investors on a monthly basis.

Cons

- High Risks:

Default Risk: You will have to run the risk of losing your invested funds should the businesses fail and default on payment.

Platform risk: If the platform (the middleman) you invest in closes down, your investments will not be managed effectively.

Thankfully there is quite a bit of regulation.

P2P Lending Regulation Singapore

The Monetary Authority of Singapore (MAS) has taken steps to regulate the P2P lending industry.

Licensed P2P lending operators must have a Capital Markets Services License and will have to comply with the controls and disclosures required of it under the MAS Circular No. CMI 27/2018 (Securities-Based Crowdfunding Circular)(issued 23 August 2018).

According to the MAS circular, operators must disclose to these things to investors:

-

Interest rate per annum to be paid by the borrower, and the interest rate per annum net of all fees and charges that investors will receive. Such information should be displayed on a restricted section of the website, accessible only to investors who are assessed to be qualified to invest in SCF offers;

-

Information about loans disbursed in each of the past three calendar years:

- (a) the lowest and highest rates of returns (excluding defaulted loans4 ), net of fees and charges to investors; and

- (b) the weighted average rate of returns (excluding defaulted loans), net of fees and charges to investors.

-

Where rates of returns are shown in advertising or marketing materials, these should be reflected as either a range between the lowest and highest rates of return

-

Disclosure of the rates of returns should be accompanied by an explanation of what the rates mean and how they are computed, and a warning that historical rates of returns may not reflect future returns

-

Non-performing loan rates, computed as the ratios of the total amount of loansthat are 30 days past due and 90 days past due over the total amount of outstanding loans for each of the past three calendar years

-

The level of due dilligence it has perfrormed on issuers.

You can find these statistics on the respective P2P lending platforms website.

P2P Lending Platforms in Singapore Comparison: BRDGE vs Moolahsense vs Funding Societies vs CA Funding vs Capital Match vs Minterest

Here’s a detailed overview and comparison of the six main P2P Platforms in Singapore:

| Company | Weighted Average Rate of Returns (Per Annum) | Default Rate (As at 31 December 2019)* | Loan Tenure | Fees | Entry | Types of P2P Investment Products | Safety Net (Fund Handling Custodian) |

|---|---|---|---|---|---|---|---|

| BRDGE (Formerly SeedIn) | 2017: 7.89% 2018: 8.33% 2019: 9.86% | 2017: 0% 2018: 0.47% 2019: 0% | 1 - 12 months | 15% (on interest earned) | $1,000 per campaign | Business Term | OCBC Bank |

| Capital Match | 2020: 11.14% | 2020: 0.05% | 3 - 12 months | 20% (on interest earned) | $1,000 per campaign (initial deposit $1,000) | Business Term Loans & Invoice Financing | Watiga Trust (Escrow agency) |

| CA Funding (Formerly CoAssets) | 2017: 8.04% 2018: 9.91% 2019: 14.01% | 2017: 2.2% 2018: 0% 2019: 0% | 3 - 36 months | 0% (on investors) | $1,000 per campaign | Business Term Loans & Invoice Financing | Vistra Trust (Escrow agency) |

| Funding Societies | 2017: 16.21% 2018: 11.73% 2019: 9.82% | 2017: 0.08% 2018: 0% 2019: 1.89% | 1 - 12 months | Service Fee: 18% on interest earned (Inclusive of GST) | $20 per campaign (initial deposit $100) | Business Term Loans & Invoice Financing | Vistra Trust (Escrow agency) |

| Minterest | 2017: 14.44% 2018: 7.53% 2019: 6.26% | 2017: 0% 2018: 0.68% 2019: 1.73% | Up to 12 months | 15% (on interest earned) | $50 per campaign (initial deposit $1,000) | Business Term Loans & Invoice Financing | Vistra Trust (Escrow agency) |

| MoolahSense | 2017: 9.73% 2018: 9.9% 2019: 8.78% | 2017: 4.46% 2018: 13.64% 2019: 20.33% | 15 days - 24 months | 1% (on all repayments) | $100 per campaign (initial deposit $1,000) | Business Term Loans & Invoice Financing | Funds held separately with OCBC Bank |

*The default rate for P2P lending mentioned above refers to the percentage of Non-Performing Loan Rates as per MAS’ guidelines

Loans are considered as defaults when the company that borrowed the loan has not made payment for more than 90 days from the contractual repayment date.

Important Disclaimer: P2P investing is a high-risk investment. We cannot stress this enough! Also, past performance is not indicative of future returns.

As such, here is more in-depth information about the companies as well as real user reviews from members of our Seedly community who will give whole lot more insight on each product to help you make a decision on the platform of your choice.

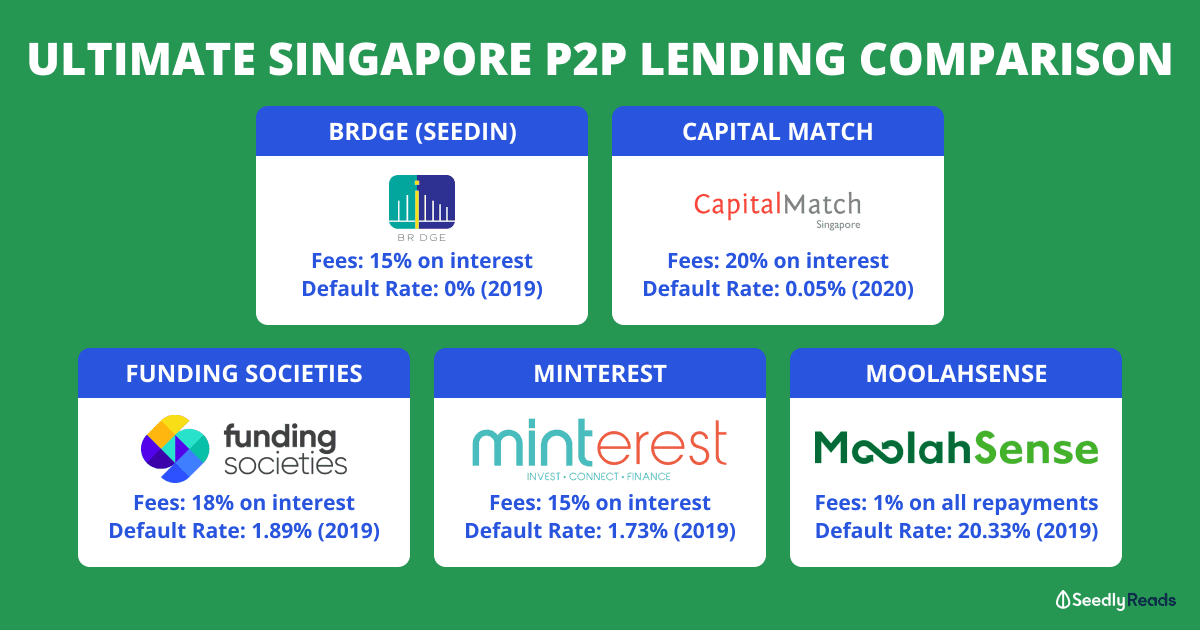

1. BRDGE (Formerly SeedIn)

- History: Established in 2013 with the vision to connect local businesses, BRDGE has facilitated about S$72 million in loans to SMEs.

- Funding: –

- Interface: Modern, clear and rather easy to use.

- Fees: 15% on repaid interest.

- Loans funded: ~S$72 million.

- Rate of default: 0% in 2019 as of 31 December 2019

- Risk Management:

Borrowers: There are many factors that go into BRDGE’s credit decision-making process. There is a minimum requirement in that the businesses to be either registered as a Singapore Private Limited or Limited Liability Partnership Entity(s).

Platform: As part of the regulatory requirements of holding the Capital Markets Services License, all the monies belonging to the investors and businesses are held in an escrow account that set up with OCBC Bank to independently manage the funds.

2. Capital Match

- History: Capital Match was established in 2014 to create a more inclusive channel for companies to access debt financing and for investors to generate strong fixed-income returns. The company was founded by Pawel Kuznicki, a tech entrepreneur with venture development before founding Capital Match.

- Funding (Crunchbase): Raised US$710K from Series A in August 2015. Total funding amount: SGD1M Investors include Innosight Ventures, Crystal Horse Investments, CE-Tech Invest.

- Interface: More heavy on numbers, fewer graphics.

- Fees: 20% on repaid interest

- Loans funded: ~S$200.5 million as of 2020.

- Rate of default: 0.05% in 2020 as of 15 December 2020.

- Risk Management:

Borrowers: Invoice financing offers more secured arrangement over unsecured loans. Only invoices issued to large debtors (corporates, government entities etc.) are accepted, and Capital Match always verifies invoices and in most cases redirect the payment from a large debtor to our bank account. This allows Capital Match a high level of control of the repayments.

Platform: As part of the regulatory requirements of holding the Capital Markets Services License, all the monies belonging to the investors and businesses are held in an escrow account set up with Watiga Trust to independently manage the funds.

3. Funding Societies

- History: Kelvin Teo and Reynold Wijaya founded Funding Societies in 2015 while studying for their MBA at Harvard. Prior to Funding Societies, Kelvin was a management consultant at Accenture and McKinsey & Co., while Reynold was a leading executive in a family business conglomerate in Indonesia.

- Funding (Crunchbase): Total funding amount: $112.5M | Backers include SoftBank Ventures Asia, Sequoia Capital, Alpha JWC Ventures, LINE Ventures, and others.

- Interface: Modern, clear and rather easy to use. Has a statistics page to allow you to see a quick overview of some of their numbers.

- Fees: 18% on interest earned (Inclusive of GST).

- Total Loans Funded Amount: ~S$1.91 billion in Singapore, Malaysia and Indonesia.

- Rate of default: 1.89% in 2019 as of 31 December 2019 (Singapore).

- Risk Management:

Borrowers: Credit assessment is based on the company’s cash flow (based on past financial data and upcoming projects), and the company/owner’s capacity & willingness to repay the loan. Personal (usually company directors) or corporate guarantor is required. These details are summarised in the form of the factsheet for every loan, and accessible by investors before and during crowdfunding.

Platform: Funding Societies holds the investors’ funds in a trust account. Should they become insolvent one day, the funds will continue to be handled escrow agency Vistra Trust. Loan agreements in place will not be dissolved and a reputable agency will be assigned to fulfil the service duties. - Skin in the game: Funding Societies’ founders invest a bit of their money in every loan they dispatch.

4. Minterest

- History: Minterest is founded by a team of former bankers Charis Liau and Ronnie Chia who both worked together in the same bank for more than 10 years.

- Funding (Crunchbase): Undisclosed.

- Interface: Modern, clear and rather easy to use.

- Best Pricing: 15% on interest repaid.

- Loans funded: Over S$152 million raised.

- Rate of default: 1.73% in 2019 as of 31 December 2019 (Singapore).

- Risk Management:

Borrowers: Minterest has its proprietary credit assessment model that reflects both quantitative and qualitative factors taking into account business and financial risks of each borrower and their respective financing requirements. Data is also sourced from third party independent information providers (eg. Dun & Bradstreet, Credit Bureau Singapore) etc. More than 200 data points are processed through their proprietary model to generate a MintGrade rating.

Platform: Minterest holds the investors’ funds in a trust account. Should they become insolvent one day, the funds will continue to be handled by an escrow agency, Vistra. Loan agreements in place will continue to be valid and a reputable agency will be assigned to fulfil the service duties.

5. MoolahSense

- History: MoolahSense was founded by Lawrence Yong, the former Vice President at Macquarie Capital. The company’s first financing campapaign was started in 2014.

- Funding (Crunchbase): Undisclosed. Seed round led by East Ventures and Pix Vine Capital. MoolahSense has raised 2 rounds. Their latest funding was raised on Sep 20, 2019 from a Corporate Round.

- Interface: Modern, clear and easy to use with a statistics page that allows a quick overview on some of their numbers.

- Fees: 1% on all repayments received on the platform

- Total Loans Funded Amount: S$74.38M

- Rate of default: 3.48%

- Risk Management:

Borrowers: Credit assessment model that assesses potential Issuers according to the nature and outlook of the industry they operate in, the strength of their financials and overall business model as well as the background and character of its Directors.

Platform: Should Moolah Sense become insolvent one day, DP Information Group to transfer servicing function to ensure that investors continue to receive monthly repayments on the loans that have been dispatched.

Conclusion: Seek to mitigate your risks with P2P investing

Should you decide to invest in any of the P2P platforms, do take note:

- P2P investing is a high-risk investment. Only invest in the portion of your money set aside for risky investments.

- Always diversify when investing in P2P. Eg. Instead of throwing all of your S$1,000 into one company on the platform, split them up into 10 companies of S$100 each.

- Diversify your investment into companies across different industries.

Advertisement