How Poor Are Singaporeans? Monthly Household Income vs Household Expenditure

Do you know where you stand among fellow Singaporeans in terms of household income?

Now, go on and sum up the income of all the income earners in your household, does it give you more than $7,744 per month?

If it does, congratulations, you are better off than 50% of Singaporean households!

But, have you ever compared your income to Singapore’s cost of living?

TL;DR: Monthly Household Income vs Household Expenditure in Singapore: Where Do You Stand?

- At least 20% of Singaporeans are earning less than their monthly expenditure

- Singaporean’s households spend an average of $4,910 per month

- Two ways to do better for household finances: Pegging your expenses in the various categories to the Singaporean’s household average, and finding the right investment to stretch your savings

Further Reading: Singaporean Household Spending

- Household expenditure of Singaporeans differs with age, with the age range of 30-39 years old spending the most.

- Based on the Household Expenditure Survey done in the year 2017/18, Singaporeans spend an average of $4,906 per month. Back in the year 2012/13, the household expenditure per household is at $4,724.

- The average expenditure per household member is $1,628 per month.

- That includes day-to-day expenses on items such as food, bus/MRT fares and clothing. Regular expenditure such as utilities, phone bills and school fees, as well as items such as holidays and hospitalisation bills are included too.

What Are Singaporeans Spending On Every Month?

Here’s a breakdown of what Singaporean households are spending on every month:

| Types Of Expenses | Amount Spent | Examples Of Expenses | Amount On Each Type Of Goods And Services |

|---|---|---|---|

| Food | $1,199 | Hawker Centres, Food Courts, Coffee Shops | $437 |

| Food, Non-alcoholic Beverages | $389 | ||

| Restaurants, Cafes and Pubs | $296 | ||

| Transport | $781 | Private Road Transport | $507 |

| Public Road Transport | $175 | ||

| Passenger Transport By Air | $96 | ||

| Housing Related | $708 | Housing And Utilities | $426 |

| Furnishing And Household Maintanence | $282 | ||

| Recreation And Culture | $379 | Holiday Package | $176 |

| Information Processing Equipment | $31 | ||

| Newspaper, Books And Stationary | $18 | ||

| Educational Services | $339 | University Education | $120 |

| Private Tuition And Other Educational Courses | $112 | ||

| Health | $323 | Outpatient Services | $172 |

| Communication | $240 | Telecommunication Services | $222 |

| Telecommunication Equipment | $18 | ||

| Clothing And Footwear | $123 | Clothing | $87 |

| Footwear | $26 | ||

| Accommodation Services | $70 | Overseas Hotel | $65 |

| Others | $744 | Insurance | $371 |

| Personal Care | $130 |

Source: Singstat.gov.sg

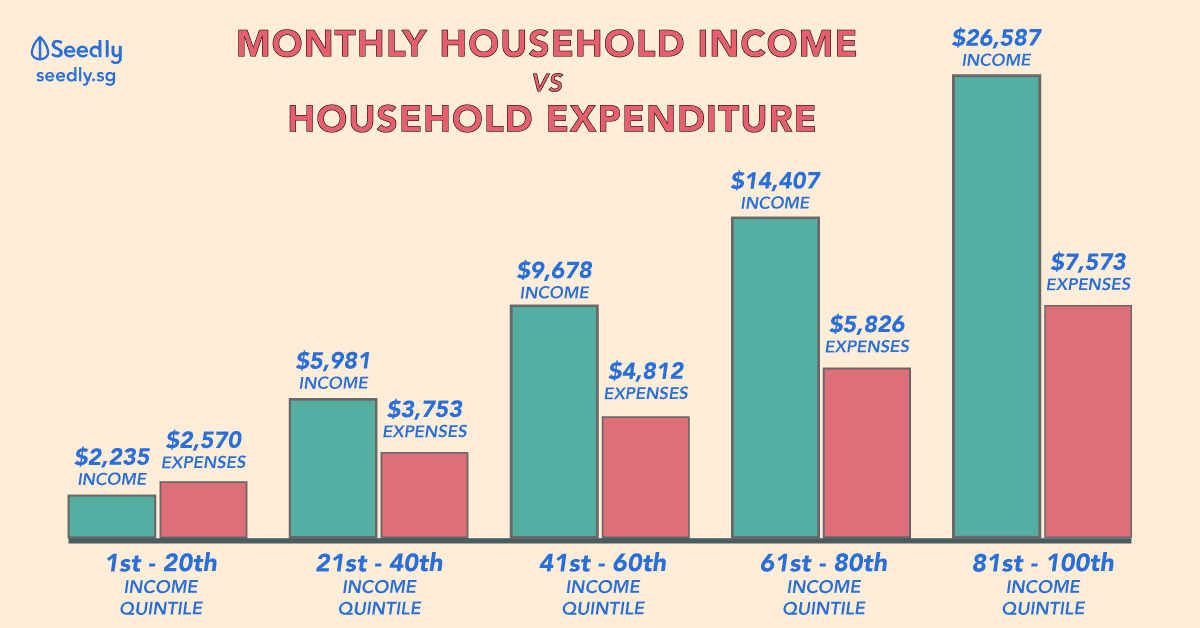

Average Monthly Household Expenditure By Income Quintile

If you are wondering how much are each income quintile of Singaporeans:

| Income Quintile | Average Monthly Household Expenditure |

|---|---|

| 1st - 20th | $2,570 |

| 21st - 40th | $3,753 |

| 41st - 60th | $4,812 |

| 61st - 80th | $5,826 |

| 81st - 100th | $7,573 |

Source: Singstat.gov.sg

Average Monthly Household Income By Income Quintile

Now that we know the monthly household expenditure, we look at the average monthly household income by income quintile.

Do note that household income includes employer CPF contributions per household member.

| Income Quintile | Average Monthly Household Income |

|---|---|

| 1st - 20th | $2,235 |

| 21st - 40th | $5,981 |

| 41st - 60th | $9,678 |

| 61st - 80th | $14,407 |

| 81st - 100th | $26,587 |

Source: Singstat.gov.sg

The Scary Truth: At Least 20% Of Singaporeans Are Earning Less Than Their Monthly Expenditure

Statistically, median household income after CPF contribution exceeds monthly household spending.

It may appear that Singaporeans are doing well until we break down the information even further.

Comparison Between Average Monthly Income To Monthly Household Expenditure

| Income Quintile | Average Monthly Household Income | Average Monthly Household Expenditure | Difference |

|---|---|---|---|

| 1st - 20th | $2,235 | $2,570 | -$335 |

| 21st - 40th | $5,981 | $3,753 | $2,228 |

| 41st - 60th | $9,678 | $4,812 | $4,866 |

| 61st - 80th | $14,407 | $5,826 | $8,581 |

| 81st - 100th | $26,587 | $7,573 | $19,014 |

- The lower 20% earners in Singapore’s income is less than their monthly expenditure. Every month, they are exceeding their monthly income by $335.

- Should they have no way of covering back this additional $335 expenses incurred, they get trapped in a cycle of debt.

- The difference in monthly household expenditure between the top 20% earners and the bottom 20% in Singapore is about $5,003.

- For the higher income, their monthly expenditure is not even one-third of their monthly household income, which means they will only get richer with each passing month.

The lower 20% earning household in Singapore, on the other hand, face a high chance of getting stuck in this cycle with no extra cash to pull themselves out of the poverty cycle. Their never-ending cycle with debt will only add on to their financial burden each money.

This is how real Singapore’s poverty situation can get for the lower income.

As for Singaporeans households that are on the 21st – 40th quintile and above, their income sits on a very comfortable level.

- 21st – 40th quintile: Income exceeds expenditure by $2,228

- 41st – 60th quintile: Income exceeds expenditure by $4,866

- 61st – 80th quintile: Income exceeds expenditure by $8,581

- Above 80th quintile: Income exceeds expenditure by $19,014

This further enhances the point that the rich will only get richer.

How we can do better – breaking that usual cycle?

- If you find your household spending more than the average, maybe it’s time to watch your expenses.

- Two ways Singaporean are stretching their household expenditure: spending on necessary item (expenditure fats) and spending on a wrong investment product

Breaking down our expenses: In search of household expenditure fats

The most immediate way to getting better with our household expenditure is to get rid of our expenditure fats. Below is a quick overview of average monthly household expenditure according to age range.

| <30 years old | 30-39 years old | 40-49 years old | 50-59 years old | >60 years old | |

|---|---|---|---|---|---|

| Housing related expenses | $830 | $888 | $761 | $595 | $552 |

| Food | $997 | $1,235 | $1,245 | $1,280 | $1,019 |

| Transport | $573 | $988 | $990 | $805 | $538 |

| Recreation | $398 | $449 | $443 | $407 | $307 |

| Educational Services | $166 | $279 | $456 | $383 | $117 |

| Health | $212 | $271 | $233 | $268 | $284 |

| Communication | $191 | $232 | $243 | $237 | $159 |

| Clothes & Foorwear | $140 | $194 | $175 | $164 | $103 |

| Others (eg. Cigarettes, beer, manicure) | $513 | $824 | $808 | $698 | $505 |

If we translate the above information into bar charts, we noticed that the 3 main categories Singaporeans of all ages spend on are:

- Housing

- Food

- Transport

Other than health, education and housing which might be subjective, one can take a look at the rest of his expenditure in terms of category every month to find out which area is he spending too much on.

Two ways to track your expenses effectively:

- An expense tracking app like Seedly (it’s free to use!)

![]()

- A detailed excel sheet

“Yea. Seedly is that free expense tracking app you can download.”

Getting The Right Investment Product

Your paycheque and savings account can only get you so far.

Choosing the right investment product should always be at the back of your mind.

It’s not uncommon for people to be sold investment-linked products by their insurance agents even if they don’t fully understand or know that they can keep the protection and investment elements apart.

In fact, some of these people might be better off investing in other financial products like the Singapore Savings Bond (SSB) if they are properly educated!

Advertisement