Ever since graduation, I’ve felt like I’m finally a full-fledged adult.

While #adulting has mostly been a wildly stressful ride, one great thing that came out of it was being able to gain full control of my finances.

While my health and fitness were indicating a slow demise of my youth, I knew I still had a long way ahead given how I had just entered the workforce, and could still enjoy the eighth wonder of the world – compound interest.

With one of the golden rules of personal finance always being to start as soon as possible, I was eager to start planning for everything, including my retirement.

Being a first jobber, a significant amount of my salary was going to my Central Provident Fund (CPF).

And of course, I had to think about how I could maximise it.

TL;DR: Should You Transfer Your CPF OA To SA as a Working Adult?

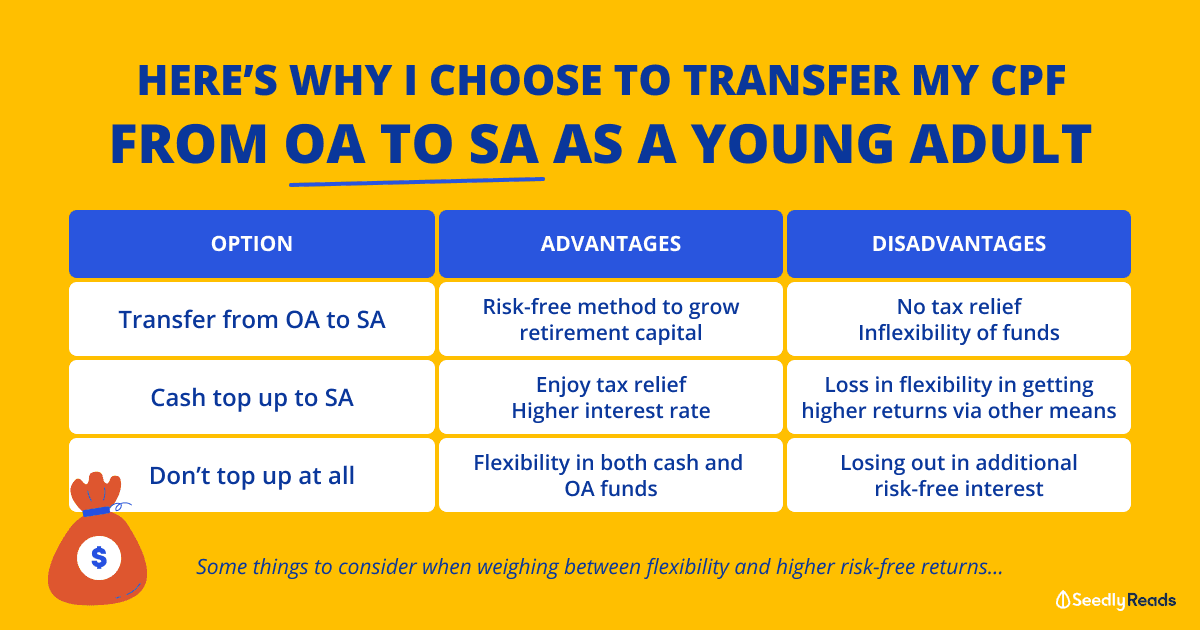

| Options | Pros | Cons |

|---|---|---|

| Transfer OA to SA | Risk-free method to grow your retirement capital | No tax relief OA cannot be used for other purposes such as education, investments Irreversible |

| Top Up SA with cash | Higher risk-free interest rate as compared to money in the bank Enjoy tax relief of up to $7,000 a year | Loss in flexibility of cash Loss in possibility of growing money with higher rate of return |

| Leave it as it is | Enjoy flexibility of both OA and SA Might have potential to jump into the property market in the future | Not earning that extra 1.5% risk-free interest |

What Is the CPF?

In short, the Central Provident Fund (CPF) is implemented to ensure that Singaporeans save up for important things — retirement, housing, and healthcare.

However, there are various purposes which you can use the CPF account for, such as property and education.

For this article, we will be focusing on two of the accounts – the Ordinary Account and Special Account.

| Ordinary Account (OA) | Special Account (SA) | |

|---|---|---|

| Uses | Property, Education, Investments | Retirement, Old Age |

| Risk Free Guaranteed Interest % p.a | 2.5% | 4.0% |

| Extra Interest For the first $60,000 | + 1% (Capped at first $20,000) | + 1% |

| Flexibility | Can use for various defined uses as above | Locked in till age 55 |

| What Happens at Age 55 | OA + SA = RA (Retirement Account) which you can remove total sum minus the Basic Retirement Sum ($93,000 for 2021) | |

The CPF Strategy I’m Adopting

Given how subjective the topic of CPF can be, here’s a quick disclaimer that this is what I feel works best for me.

Such decisions are highly personal and very subjective, so pick the one that suits you the best.

Through this article, you will be able to see the different strategies you are able to adopt.

For me, I personally prefer this method:

- Keep sufficient funds for HDB BTO downpayment (~10% of purchase price)

- Buffer 12 to 18 months for loan repayment

- Transferring the excess OA to SA

Note: You need to have a property in order to only set aside Basic Retirement Sum at 55

Instead of just leaving the minimum $20,000 required in the OA, I chose to set aside more for contingency due to the volatility of the job market.

Assuming that I transfer $30,000 from my OA to SA at age 25, this is the difference in the amount as compared to leaving it in my OA till 55 years old.

| Age | Ordinary Account (2.5%) | Special Account (4.00%) |

|---|---|---|

| 25 | $30,000 | $30,000 |

| 30 | $33,942.25 | $36,499.59 |

| 40 | $43,448.94 | $54,028.31 |

| 50 | $55,618.32 | $79,975.09 |

| 55 | $62,927.03 | $97,301.93 |

We can see the difference in interest using the rule of 72.

The rule of 72 indicates taking the number 72 and dividing it by the interest rate, and we can see how many years it takes for a sum to double.

If the interest rate is 2.5%, the amount of money will double in about 29 years.

If it is 4%, it will double in 18 years instead!

This is not taking into account the transfers I’ll continue to do as I continue working along the years.

I’m choosing to do this as I am not planning to invest my CPF monies, even though it might potentially yield higher returns.

What Are the Strategies That You Can Adopt

There are a few strategies you can look into to utilise your CPF accounts.

All methods come with their own sets of pros and cons.

Strategy 1: Transfer from OA to SA

This is the strategy that I’m adopting, which basically provides guaranteed returns of minimally 4% in the SA and it will compound for many years till age 55.

![]()

Pros:

- You get a risk-free method to grow your retirement capital at a faster pace (4% SA vs 2.5% OA)

- Convenient as you don’t have to choose what to invest in

Cons:

- You will not be able to use your CPF OA to pay for private or HDB property, especially if you choose to upgrade along the way

- You will also not be able to spend the additional funds in investments, education or approved insurance

- There’s no tax relief for transfers from OA to SA, which might be a missed opportunity especially for high-earners

Note: You can use this official calculator by CPF to determine if you should transfer between OA to SA.

Strategy 2: Cash Top up To SA

This is a method that some bloggers would recommend.

Especially if you are someone who has excess cash sitting in the bank but also unwilling to take risks with other investment products out there.

Pros:

- If cash sits in the bank, it gets around 1% interest. On the other hand, the CPF SA gives you a 4% risk-free interest rate every year, compounded over time

- You get to enjoy tax relief of up to $7,000 each calendar year based on the total amount you top up your SA

Cons:

- Losing the flexibility of cash which might be required for other purposes, especially big-ticket items

- Losing the possibility of growing the money via other methods (e.g. investments) which might bring a higher rate of return

Strategy 3: Don’t Top up Your SA at All

This is the default strategy that any working adult would adopt if no changes are made.

The allocation for the SA and OA will change over the years as you reach retirement age.

| Employee’s Age | Contribution Rates from 1 Jan 2016 | ||

| By Employer (% of wage) | By Employee (% of wage) | Total (% of wage) | |

| 55 and below | 17 | 20 | 37 |

| Above 55 to 60 | 13 | 13 | 26 |

| Above 60 to 65 | 9 | 7.5 | 16.5 |

| Above 65 | 7.5 | 5 | 12.5 |

Pros:

- By keeping the OA and SA separate, it gives us the flexibility of having both cash and the OA funds for other opportunities

- As mentioned by a Business Times contributor, he felt that by letting the OA build over time with 2.5% would provide the opportunity to pounce on the property market

Cons:

- Not earning that extra 1.5% which would compound over the years

- This is assuming that the SG government would not change any of the property cooling measures which might make the property market less attractive for rent or appreciation

Conclusion: Higher Flexibility vs Higher Risk-Free Returns

As with any other money decision, this decision has to be considered carefully and it is important to do your own due diligence on the different options available.

As mentioned above, the main concerns for the transfer of CPF from OA to SA are as follows:

- It locks up your funds in the SA account till age 55

- You will not be able to jump on other property opportunities with CPF OA or use it for other purposes

- You cannot reverse this action or choose to withdraw from the SA once you decided to top up your SA with either your OA or cash

At the end of the day, it’s about being more comfortable with whichever choice that you’ve made, and seeing which one aligns with your long-term goals.

How To Top up Your CPF SA

For those who are interested in topping up your CPF account, here are a few methods to do so.

Option 1: My CPF Online

Type: CPF transfers (from OA to SA) or cash top-ups via OCBC’s Internet Banking

- Login with your SingPass.

- Submit an online application via My Requests > Building Up My / My Recipient’s CPF Savings.

- For cash top-up, please make your payment immediately via OCBC’s Internet Banking/Mobile Banking/ATM.

Top-ups will be processed within 5 working days upon receipt of application.

Option 2: e-Cashier

Type: Cash top-ups only

- Go to e-Cashier and select payment for top up my own/recipient’s RA/SA under the Retirement Sum Topping-Up Scheme (RSTU).

- Make your payment immediately via E-cashier’s mode of payment (eNETS Debit only).

Your top-up will be processed according to CPF service standards after the application is received.

Option 3: AXS Machine

Type: Cash top-ups only

- Go to any AXS station and select payment for top up my own/recipient’s RA/SA under the Retirement Sum Topping-Up Scheme (RSTU).

- Make your payment immediately via the AXS machine.

Your top-up will be processed within CPF service standards after the application is received.

Would you transfer your CPF from OA to SA?

Would you transfer your CPF from OA to SA, or what would some of your considerations be?

Let us know at our SeedlyCommunity!

Advertisement