Singapore Airlines' $15 Billion Rescue Package Approved by Shareholders - Here is What Investors Need to Know

Joel Koh

Joel Koh●

On 30 April 2020, Singapore Airlines (SIA) shareholders gathered at the SIA virtual Extraordinary General Meeting (EGM) to vote in favour of the $15 billion fundraising package proposed by the airline.

This momentous event was called as the COVID-19 pandemic has brought the global airline industry to its knees.

To get a good grasp on what is happening, you might want to look at why my colleague Sudhan will not be buying SIA shares despite the Singapore Airlines share price being cheap.

But first, here is what you need to know about this package and the EGM.

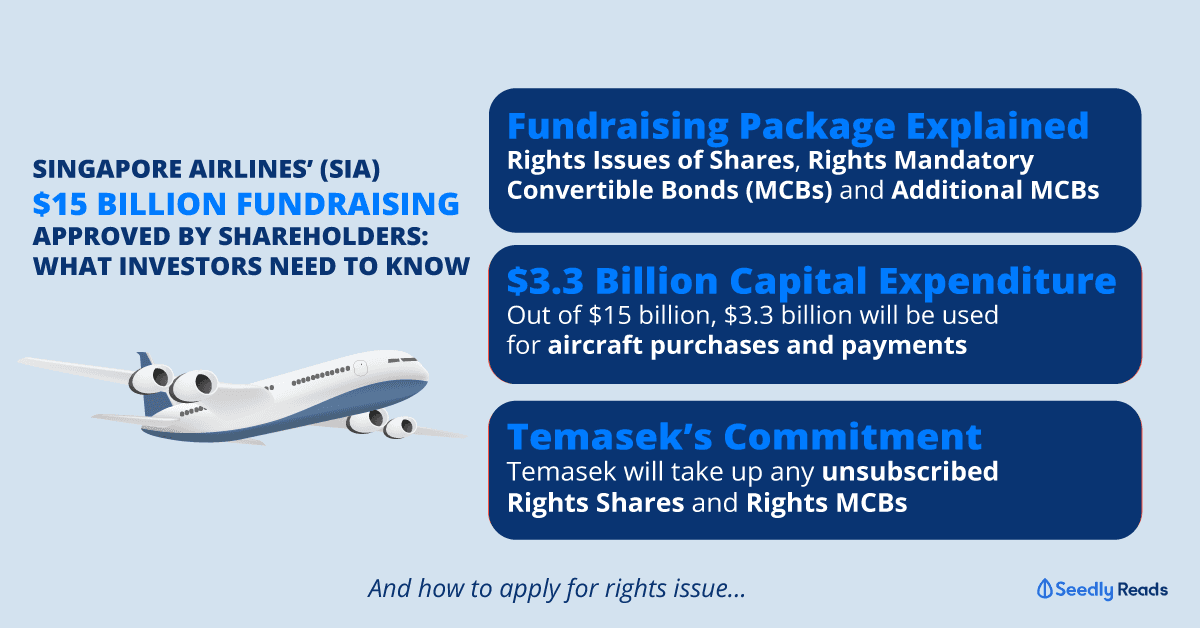

TL;DR: Singapore Airlines’ $15 Billion Rescue Package Approved by Shareholders – Here is What Investors Need to Know

Don’t have time to comb through all the information from the SIA EGM? We got you!

Here are the key takeaways from the April 2020 Singapore Airlines (SGX: C6L) EGM.

![]()

I will be covering:

- The outcome of the EGM

- The Rights Issue and the Mandatory Convertible Bond (MCB) issue

- Why SIA is raising money instead of taking up debt

- How they are managing their expenses

- Temasek’s commitment and;

- What you as an investor should know.

1) Singapore Airline April 2020 EGM Outcome

At the virtual EGM, shareholders voted on two resolutions.

Resolution One: The Proposed Renounceable Rights Issue

99.79% of voters voted in favour of this first resolution.

This will see SIA raising $8.8 billion initially through a 3-for-2 Rights Issue of shares and a Rights MCB issue.

FYI: A mandatory convertible is a bond issued by a company which must be converted into shares or common stock on or before a specific date.

3-for-2 Rights Issue of Shares

SIA will proceed with a renounceable Rights Issue of up to 1.77 billion new shares at $3 per share to raise $5.3 billion

This issue price is about 53.8% of the last traded price of $6.50 per share on 25 March, while the Theoretical Ex-rights Price (TERP) will be about $4.40.

This rights issuance will mean that existing shareholders will be entitled to three rights shares for every two existing shares.

Rights Mandatory Convertible Bond (MCB) Issue

Additionally, the company will raise another $3.5 billion by issuing 10-year Rights MCBs which are of the zero-coupon bond variety.

FYI: A zero-coupon bond is a debt security that does not pay interest but instead trades at a deep discount. Profit is earned when the bond is redeemed.

There will be 295 Rights MCBs for every 100 existing shares owned priced at $1 each

If you do not redeem the MCB before the maturity date, the MCB will be converted to new shares priced at $4.84, which is 10% higher than the TERP.

| Key Terms of Rights MCBs | |

|---|---|

| Issue Size | Up to approximately $3.5 billion |

| Issue Price | $1.00 for each $1.00 in principal amount of the Rights MCBs |

| Maturity Date | 10th anniversary of the issue date of the Rights MCBs |

| Coupon | Zero coupon |

| Rights Ratio | 295 Rights MCBs for every 100 existing Shares |

| Mandatory Conversion | Mandatory conversion at maturity at Final Accreted Principal Amount. No further cash outlay is needed from the Rights MCB holders for the conversion of their Rights MCBs into Shares. |

| Final Accreted Principal Amount | $1.80611 in respect of each S$1.00 in principal amount of Rights MCBs on the Maturity Date (1) |

| Conversion Price | Initially S$4.84 (2) |

| Redemption Option | At the option of the Company, in whole or in part, on every 6th month anniversary of the issue date. Any redemption prior to maturity will be in the form of cash payment. |

| Redemption Price | Within first four years of issue date. 4% yield to call (p.a.) |

| Within fifth to seventh year of issue date. 5% yield to call (p.a.) |

|

| From eighth year of issue date onwards. 6% yield to call (p.a.) |

|

(1) Calculated based on a 6% annual yield to conversion, compounded on a semi-annual basis

(2) Subject to adjustments, representing a 10% premium to TERP. Includes consolidation or subdivision of Shares, capitalisation of profits or reserves, capital distributions, dividends, share repurchases and others.

Resolution Two: The Proposed Issuance of Additional Mandatory Convertible Bonds and Additional Conversion Shares.

99.66% of shareholders voted in favour of this resolution

This will allow SIA to issue up to $6.2 billion of Additional MCBs with nearly identical terms to shareholders within 15 months after the 30 Apr 2020 EGM.

2) What Is The Difference Between Rights MCBs and Additional MCBs?

SIA states that the terms of the Additional MCBs will be almost identical to the terms of the Rights MCBs.

Additional MCBs will be offered to Shareholders on a pro-rata basis if the airline chooses to carry out more rights issues.

3) Why is Singapore Airlines Raising Such a Large Amount?

A shareholder asked why there was a need to raise such a large amount so quickly and what the funds will be used for.

Singapore Airlines responded by saying that the initial amount of $8.8 billion that is to be raised in the Rights Issue will provide their business with liquidity.

The funds will be used to meet pressing operating cash flow needs, capital expenditure and fixed obligations for most of Fiscal Year (FY) 2020/2021.

They intend to utilise the net proceeds from the S$8.8 billion Rights Issue for the following:

- $3.7 billion to fund fixed costs and other operating expenses incurred during this period of reduced operations and the subsequent recovery period Capital expenditure

- $3.3 billion to be used for aircraft purchases and aircraft-related payments

- $1.8 billion to be used for debt service and other contractual payments

If the COVID-19 pandemic does not clear up by the end of 2020, the airline will possibly issue the Additional MCBs.

4) Why Will a Significant Portion of the Funds (38% or $3.3 Billion) Be Used for Capital Expenditure?

Speaking of expenditures, a shareholder questioned why so much was being used for capital expenditure.

SIA explained that this money will be used mainly for aircraft purchases and other aircraft related payments.

The company clarified that these aircraft purchases were made in the past as part of their fleet renewal strategy.

The aim was to upgrade their fleet with new-generation aircraft to replace their existing fleet as these planes are operationally more efficient and produce fewer emissions.

They are also negotiating with the aircraft manufacturers to adjust their delivery stream in light of current market conditions.

5) Why is SIA Carrying Out Fundraising Instead of Issuing Debt?

Another shareholder asked why SIA chose to undertake the fundraising instead of taking on more loans or issuing debt.

The airline responded by saying that choosing to raise money through debt financing entirely will significantly increase the company’s leverage.

This will increase the company’s risk of default and limit them from raising any money through debt funding in the future.

Additionally. this will further strain their weak liquidity as there will be the added cash outflow obligations from taking up more debt.

Instead, they have chosen to carry out the issuance of Rights Shares, Rights MCBs and Additional MCBs (if applicable).

This means that the funds raised will be considered equity and protect their balance sheet for the future.

Plus, the Rights MCBs and Additional MCBs (if issued) are of the zero-coupon variety, which relieves them of immediate cashflow problems as holders of the MCBs are not allowed to redeem them.

It is clear why SIA is taking this route. Hopefully, the airline industry will recover and bounce back for the sake of all the investors involved.

6) How is SIA Managing its Costs During These Uncertain Times?

To preserve cash, SIA has engaged in these cost-cutting measures:

- Cut 96% of their scheduled capacity up to end June 2020

- Pay cuts for senior management since 1 March 2020. The percentage will be raised 20-30% with effect from 1 April 2020

- Directors will also take a 30% pay cut.

- Pilots, executives and associates have been taking compulsory no pay leave as well as furloughs for those on re-employment contracts.

- Implementation of a hiring freeze and a voluntary no-pay leave scheme for staff.

- Deferment on non-essential expenditure.

They have also taken these steps to improve their liquidity:

- Activated their lines of credit maintained for emergency situations.

- Explored other traditional funding channels such as secured financing and sale-and-leaseback transactions, although opportunities remain limited in current market conditions.

Well, hindsight is 2020, but back in 2015, the company bought back 630,800 of its own shares in the open market at S$9.68 to S$9.92; coughing up a total of $6.18 million.

Perhaps they will learn from this lesson and save up more cash for rainy days.

7) Temasek’s Commitment to SIA

Majority shareholder Temasek who owns a 55.4% stake in SIA voted in favour of the Rights Issue and the MCBs Issue.

![]()

They have also committed to taking up any unsubscribed Rights Shares and Rights MCBs

This gives a degree of certainty of funding to SIA which will allow the company to survive and hopefully position itself to capture medium and long term growth beyond COVID-19.

What Investors Need to Do

Retail investors who own Singapore Airlines shares have only two options.

The first option is to protect your current position and take part in the rights issuance at $3 per share and average down the cost of your holdings.

This increases your potential upside if the company eventually recovers if and when global travel demand picks up.

The implication is that as an investor, you will need to have the capital to subscribe pro-rata to this additional issuance.

For example, if you currently own 1,000 pieces in SIA, you will need S$4,500 ready to take part in this rights issuance.

The second option is to choose not to subscribe to the additional rights issuance. However, this will result in the significant dilution of your stake in SIA.

Assuming you currently own a 1% stake in SIA and do not take part in the rights issuance, your stake will be immediately diluted to 0.4% post-rights issuance.

Indicative Timeline of Key Events For SIA Rights Issue

As such, here are the key dates to take note of if you would like to take part in the rights issue.

| Key Event | Date and Time |

|---|---|

| First date for Shares to trade “ex-rights” to the Rights Issue | Wednesday, 6 May 2020 from 9.00am |

| Lodgment of the Offer Information Statement, the product highlights sheet and accompanying application forms with the MAS | Friday, 8 May 2020 |

| Record Date | Friday, 8 May 2020 at 5.00pm |

| Despatch (where required) of the Offer Information Statement (together with the product highlights sheet, the ARE, the ARS or the PAL, as the case may be) to Entitled Shareholders | Wednesday, 13 May 2020 |

| Commencement of trading of Rights | Wednesday, 13 May 2020 from 9.00am |

| First date and time for acceptance of and payment for the Rights Shares, the Rights MCBs and/or applications for excess Rights Shares and/or excess Rights MCBs | Wednesday, 13 May 2020 from 9am for electronic applications through ATMs of Participating Banks or online |

| Last date and time for splitting and trading of Rights | Thursday, 21 May 2020 at 5.00pm |

| Last date and time for acceptance of and payment for Rights Shares and/or Rights MCBs and/or applications for excess Rights Shares and/or excess Rights MCBs | Thursday, 28 May 2020 at 5.00pm for applications made via CDP or the share registrar or online Thursday, 28 May 2020 at 9.30 pm for electronic applications through ATMs of Participating Banks |

| Last date and time for application and payment for Rights Shares and/or Rights MCBs by renouncees |

|

| Expected date of issuance of Rights Shares and Rights MCBs | Friday, 5 June 2020 |

| Expected date of commencement of trading of Rights Shares(1) | Monday, 8 June 2020 |

| Expected date of commencement of trading of Rights MCBs | Tuesday, 9 June 2020 |

The rights shares can be traded on SGX. This means you can buy and sell them like normal stock

However, you should consider selling off the rights if you do not want to exercise them. You can also buy more rights and exercise them later.

The rights shares are entitled “SIA R” with the symbol “LRDR.”

The MCB rights are entitled “SIA MCB R” and code “GANR.”

(1) This does not apply to CPFIS Members, SRS Investors and investors who hold Shares through a finance company and/or Depository Agent. (E.g. custodian accounts).

CPFIS Members, SRS Investors and investors who hold Shares through a finance company and/or Depository Agent should refer to the Offer Information Statement after the lodgment of the Offer Information Statement with the MAS for details relating to the application procedure for them.

(2) Further details relating to the online application website will be set out in the Offer Information Statement after the lodgment of the Offer Information Statement with the MAS.

What Are Your Thoughts on Singapore Airlines?

In the meantime, why not check out the Seedly Community and participate in the discussion surrounding stocks like Singapore Airlines (SGX: C6L)!

Disclaimer: The information provided by Seedly serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any stock.

Advertisement