Silicon Valley Bank Collapse Explained: Will Silicon Valley Bank Affect Singapore?

Joel Koh

Joel Koh●

If you have been reading the news lately, you might have seen headlines about Silicon Valley Bank (SVB) and YouTube videos with dramatic clickbaity thumbnails:

You might think that the end is nigh, and we might see another collapse like the 2008 Global Financial Crisis again.

But if you want the truth about what’s really going on.

Read on to find out.

TL;DR: How Did Silicon Valley Bank (SVB) Collapse?

Click to Teleport

- What Caused the Silicon Valley Bank to Collapse?

- What Happened at the Silicon Valley Bank? Timeline of Events

- Will Silicon Valley Bank Affect Singapore?

- What Should You Do With Your Bank Deposits?

What Caused the Silicon Valley Bank to Collapse?

For context, a bank run happens when a large number of depositors withdraw their money simultaneously from a bank due to concerns that the bank might become insolvent. As more and more people withdraw their funds, the bank’s cash reserves diminish, and it may ultimately become unable to repay its depositors. Bank runs have occurred in the past, including during the Great Depression and the 2008-09 financial crisis.

The Federal Deposit Insurance Corporation (FDIC) was created in 1933 as a response to the thousands of bank failures that occurred in the 1920s and early 1930s.

As renowned author Mark Twain once said:

History never repeats itself, but it does often rhyme.

What Happened at the Silicon Valley Bank? A Timeline of Events

This time around, the rhyme is about Silicon Valley Bank (SVB), which collapsed last Friday:

That is the timeline of events, but let me provide some context on what went down.

Is Silicon Valley a Global Bank?

According to Visual Capitalist, ‘Silicon Valley Bank is a 40-year-old commercial bank that was an important lender for the tech and venture capital centre. It is estimated that half of U.S. venture-backed startups were customers of the bank.’

Back in 2020, the U.S. Federal Reserve (Fed) cut interest rates to near zero to stimulate the economy and protect and safeguard the economy from the impact of the COVID-19 outbreak.

At the risk of oversimplifying things, the low cost of borrowing resulted in an uptick in financial activity that saw money pouring into the economy and the stock market go on a bull run.

Startups in America were big beneficiaries as they received funding freely from investors. Flush with cash, these startups deposited their cash in SVB. As a result, SVB’s holdings more than tripled from US$61.76B (S$83.25B) at the end of 2019 to US$189.20B (S$254.77B) at the end of 2021.

Typically most banks earn money on deposits by providing loans. But, the problem that SVB had was that it could not lend out its money fast enough.

To solve this issue, SVB took a risk and invested about US$120B (S$161.62B) into a portfolio of long-term U.S. government-backed securities with a solid credit rating.

Out of the money invested, about US$91B (S$122.56B) was put into fixed-rate mortgage bonds maturing in ten-plus years’ time with an average interest rate of just 1.65 per cent.

This risky move unravelled when the Fed started pivoting and raising interest rates in March last year:

| Target Federal Funds Rates for 2022 | ||

|---|---|---|

| Date | Fed Funds Rate | Event |

| 26 Jan 22 | 0.25% | Effectively Zero |

| 16 March 22 | 0.5% | Inflation |

| 4 May 22 | 1% | The Russian invasion of Ukraine; China brings back COVID-19 lockdowns |

| 15 June 22 | 1.75% | Inflation reached a 40-year high |

| 27 July 22 | 2.5% | Inflation continued to grow |

| 21 Sept. 22 | 3.25% | Inflation is still impacting Americans |

| 2 Nov 22 | 4% | Inflation is still impacting Americans |

| 14 Dec 22 | 4.5% | Fed slows its fight against inflation |

Source: The Balance

As a result of rising interest rates, SVB’s portfolio of bonds fell in value by US$15B (S$20.21B) in 2022. This was almost equivalent to the entirety of SVB’s capital.

If SVB were forced to sell these bonds, it would have to actualise its losses and risk technical insolvency.

At the same time, tech startups were starting to suffer as well due to hikes, as evidenced by the widespread layoffs in the tech sector.

According to Fortune, SVB’s bank run was “sparked by a letter that SVB Chief Executive Officer (CEO) Greg Becker sent to shareholders Wednesday (8 March 2023). The bank had suffered a US$1.8B (S$2.42B) loss on the sale of US treasuries and mortgage-backed securities and outlined a plan to raise US$2.25B (S$3.03) billion of capital to shore up its finances. Customers immediately tried to pull their money, including many of the venture-capital firms the bank had cultivated over decades. Peter Thiel’s Founders Fund, Coatue Management, Union Square Ventures and Founder Collective all advised their startups to pull their cash from the bank, people familiar with the matter said. The withdrawals initiated by depositors and investors amounted to US$42B (S$56.6B) on Thursday alone, according to the regulator. Despite being in sound financial condition before Thursday, the California watchdog said the run ’caused the bank to be incapable of paying its obligations as they come due,’ and it was now insolvent.”

Who Owns the Silicon Valley Bank?

This withdrawal caused the bank to collapse as last Friday (10 March 2023), the California Department of Financial Protection and Innovation (DFPI) took possession of the bank and appointed the FDIC as receivers.

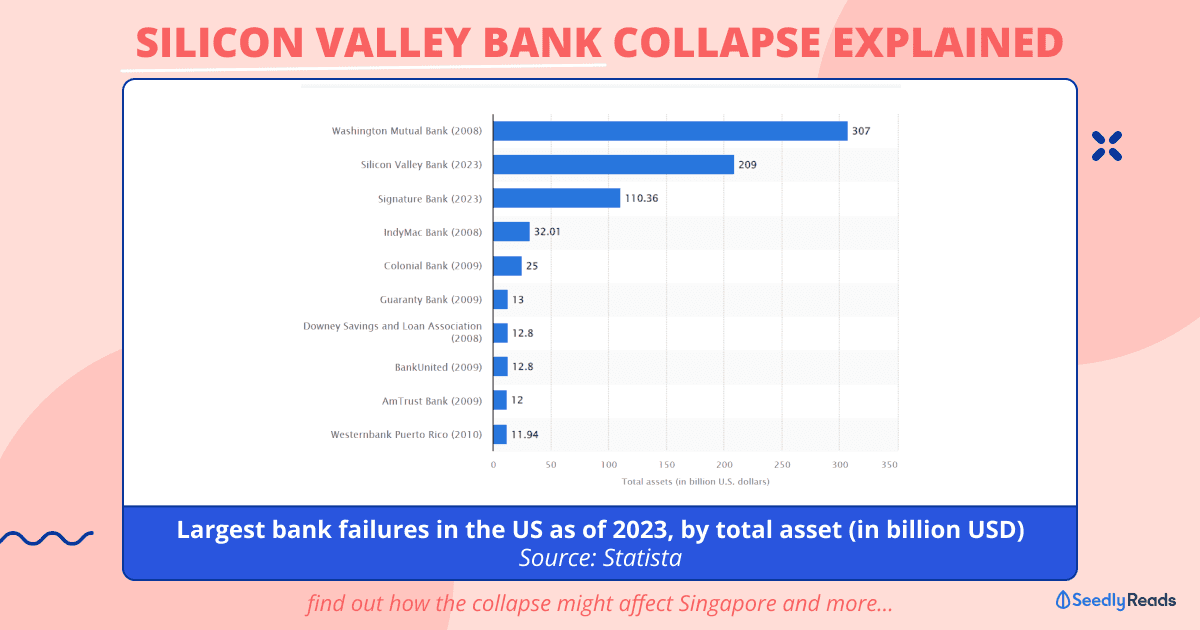

SVB’s collapse went down as the second-biggest bank run in U.S. history, with the biggest being the fall of Washington Mutual back in 2008.

That’s not all.

On Sunday (12 March 2023) Signature Bank, a financial institution based in New York with a huge real estate lending business and made a recent big bet on Cryptocurrency deposits, closed its doors.

The Financial Times reported that the ‘FDIC took control of Signature, which had US$110.36B (S$148.76B) in assets and US$88.59B (S$119.41B) in deposits at the end of last year.’

Arguably, Signature Bank could have been a victim of the SVB panic.

Silicon Valley Bank Bailout?

To prevent this contagion from spreading, the Department of the Treasury, Federal Reserve, and FDIC issued a joint statement:

After receiving a recommendation from the boards of the FDIC and the Federal Reserve, and consulting with the President, Secretary Yellen approved actions enabling the FDIC to complete its resolution of Silicon Valley Bank, Santa Clara, California, in a manner that fully protects all depositors. Depositors will have access to all of their money starting Monday, March 13. No losses associated with the resolution of Silicon Valley Bank will be borne by the taxpayer.

We are also announcing a similar systemic risk exception for Signature Bank, New York, New York, which was closed today by its state chartering authority. All depositors of this institution will be made whole. As with the resolution of Silicon Valley Bank, no losses will be borne by the taxpayer.

Shareholders and certain unsecured debtholders will not be protected. Senior management has also been removed. Any losses to the Deposit Insurance Fund to support uninsured depositors will be recovered by a special assessment on banks, as required by law.

So it appears that the banks are safe, and the contagion has been contained for now.

Will Silicon Valley Bank Affect Singapore?

In response to these events, the Monetary Authority of Singapore said in a statement yesterday (13 March 2023) that:

The Singapore banking system has insignificant exposures to these failed banks in the US. Banks in Singapore are well-capitalised and conduct regular stress tests against interest rate and other risks. Their liquidity positions are healthy, underpinned by a stable and diversified funding base. These factors will allow them to weather potential stresses from global financial developments.

MAS is closely monitoring the domestic financial system and international developments. MAS stands ready to provide liquidity through its suite of facilities to ensure that Singapore’s financial system remains stable and financial markets continue to function in an orderly manner.

What Should You Do With Your Bank Deposits?

The bank run in the U.S. might have you feeling a bit anxious about your bank’s deposits.

But, Singapore consumers enjoy the benefits of a sound banking system. Banks and finance companies licensed in Singapore are supervised by the Monetary Authority of Singapore (MAS). It is MAS’ aim to ensure the stability of the banking system in Singapore and to require financial institutions to have sound risk management systems and adequate internal controls.

However, MAS does not guarantee the soundness of individual financial institutions. Therefore, a Deposit Insurance Scheme has been set up to protect the core savings of small depositors in Singapore in the event a full bank or finance company fails.

The SDIC was set up to protect the core savings of small depositors in Singapore if a full bank or finance company fails.

Your deposits in your bank account are insured for up to S$75,000 per bank. So if the bank goes bankrupt, this is the amount which you can get back from this organisation.

An important thing to note is that according to the SDIC, the deposit insurance ‘limit of S$75,000 is applied on a per depositor per Scheme member basis. The deposits in your savings account and fixed deposit account with Bank A will be aggregated and covered up to S$75,000. Only trust and client accounts are separately insured on a per account basis.’

So if you are really kiasu (scared to die in Hokkien), you should not put more than S$75,000 in one bank as even if you have multiple bank accounts with one bank, your deposits are only insured by up to S$75,000.

Read More

Advertisement