For our Morning Stocks Analysis, the Seedly team worked closely with The Motley Fool, who is an expert in the field, to curate unbiased, non-sponsored content to add value back to our readers.

Disclaimer: This is not a sponsored post. Opinions expressed in the article should not be taken as investment advice. Please do your own due diligence.

If you have any questions on the mentioned stocks, you can ask the Seedly Community here.

DBS Group Holdings Ltd (SGX: D05), Oversea-Chinese Banking Corporation Limited (SGX: O39) and United Overseas Bank Ltd (SGX: U11) are three major listed banks in Singapore.

The trio, which makes up around 40% of the Straits Times Index (SGX: ^STI), performed well financially in 2018. For investors who are looking to pick the best of the lot, here’s a comparison of the banks’ 2018 key financial ratios.

Key ratios on profitability

The table below shows a few key ratios that give us a picture of the banks’ profitability:

| Bank | Net Interest Margin | Cost-to-Income Ratio | Return on Assets | Return on Equity |

|---|---|---|---|---|

| DBS | 1.85% | 44.0% | 1.05% | 12.1% |

| OCBC | 1.70% | 43.4% | 1.17% | 11.5% |

| UOB | 1.82% | 43.9% | 1.07% | 11.3% |

Source: Banks’ 2018 financial statements (the “best” metrics are in bold)

Net interest margin (NIM): Similar to the operating margin for an industrial company. The NIM shows the average interest margin that a bank is earning from its borrowing and lending activities. Among the three banks, DBS had the highest NIM for 2018.

Cost-to-income ratio: This ratio measures the non-interest expense of a bank as a percentage of its revenue. It is to gauge the efficiency and productivity of banks. Generally, the lower the ratio is, the more efficient a bank is. Among the three banks, OCBC had the lowest cost-to-income ratio in 2018.

Return on assets and return on equity: These tell us how effective a bank’s management is in maximising the profits earned on shareholders’ capital. Among the three banks, for 2018, OCBC had the highest return on assets and DBS had the highest return on equity.

Key ratios on strength of their balance sheet

Here is a table showing the key ratios that can give us clues on how strong the banks’ balance sheets are:

| Bank | Loan-to-Deposit Ratio | Non-Performing Loans Ratio | Leverage Ratio | Average All-Currency Liquidity Coverage Ratio |

|---|---|---|---|---|

| DBS | 87.6% | 1.5% | 7.1% | 133% |

| OCBC | 86.4% | 1.5% | 7.2% | 143% |

| UOB | 88.2% | 1.5% | 7.6% | 135% |

Source: Banks’ 2018 financial statements (the “best” metrics are in bold)

Loan-to-deposit ratio: This ratio measures a bank’s liquidity. The sweet spot for this ratio is usually between 80% and 90%. Banks that have a loan-to-deposit ratio below that range may not be maximising the capital they have. On the other hand, if a bank’s loan-to-deposit ratio is above the range, it might run into liquidity problems when there is a high withdrawal rate on deposits, especially during an economic crisis. Among the three banks, UOB was the best at maximising the loans and deposits it had in 2018, given that it had the highest loan-to-deposit ratio in that year.

Non-performing loans (NPL) ratio: A non-performing loan is a loan on which the borrower is unable to pay off interest or the principal amount. The lower the ratio, the better it is for a bank. It’s a tie among the three banks in 2018 as all have an NPL ratio of 1.5%.

Leverage ratio and liquidity coverage ratio: These ratios show the ability of a bank to meet its financial obligations. In general, the lower the leverage ratio, the better. Meanwhile, for the liquidity coverage ratio, we’re looking for high numbers. Among the three banks, DBS had the lowest leverage ratio while OCBC had the highest liquidity coverage ratio in 2018.

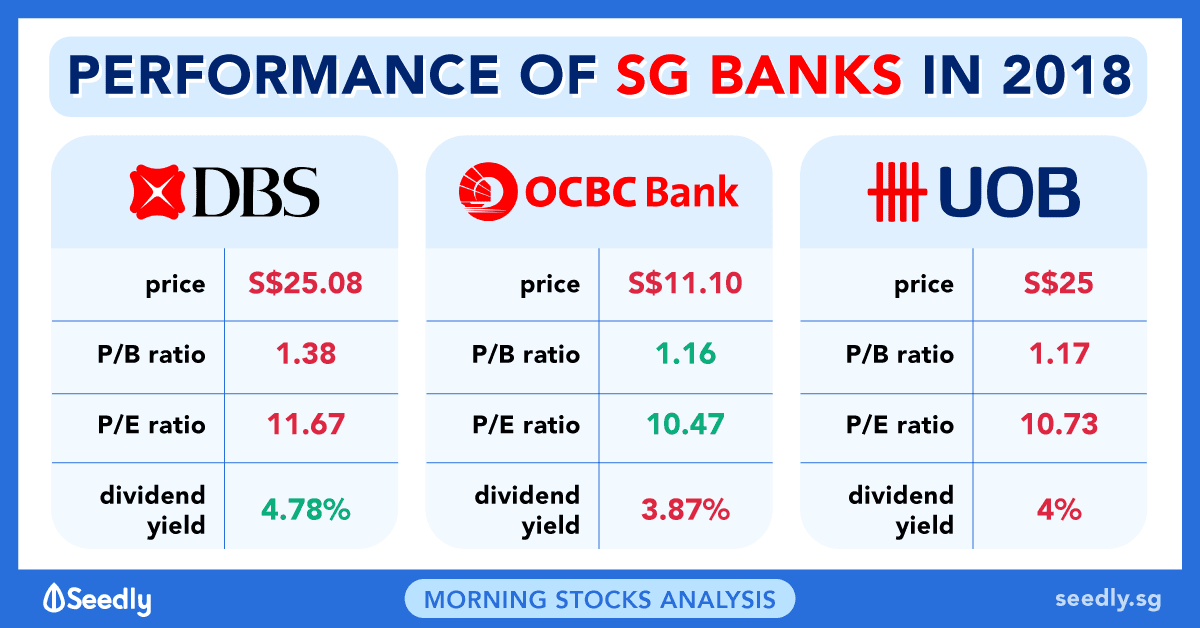

Key ratios on valuation

The following table spells out the banking trio’s important valuation numbers:

| Bank | Price | Price-to-Book (PB) Ratio | Price-to-Earnings (PE) Ratio | Dividend Yield |

|---|---|---|---|---|

| DBS | S$25.08 | 1.38 | 11.67 | 4.78% |

| OCBC | S$11.10 | 1.16 | 10.47 | 3.87% |

| UOB | S$25.00 | 1.17 | 10.73 | 4.00% |

Source: Banks’ 2018 financial statements; closing price as at 1 March 2019

OCBC seems to offer the best value among the three banks with its lowest PB and PE ratio. However, it loses out to the other banks in terms of dividend yield. UOB’s board has declared a special dividend of 20 cents per share in 2018. Including that dividend, the bank’s adjusted dividend yield would be 4.80%.

Seedly Guest Contributor: The Motley Fool

The Motley Fool (fool.sg) offers stock market and investing information, offering people suggestions on how to take control of their money and make better financial decisions.

The Motley Fool Singapore primarily covers the Singapore market, though we also bring investing news from around the world. We also host a range of educational content, written for everyday people. We feel that the best person to make your financial decisions is you, and we want to help you take control of your own money. The Motley Fool also champions shareholder values and advocates tirelessly for the individual investor.

Read other articles by The Motley Fool:

- 3 Singapore Blue-Chip Stocks That Have More Than Doubled Their Profits In The Last Decade

- Singapore’s Top 10 Dividend Shares Among the World’s Best

- The Better Dividend Share: SIA Engineering Company Ltd or Singapore Technologies Engineering Ltd?

- Big Week For Earnings With DBS, OCBC, UOB And Two Property Giants

- 2 Singapore Blue-Chip Companies That Announced Weaker Results Recently

Advertisement