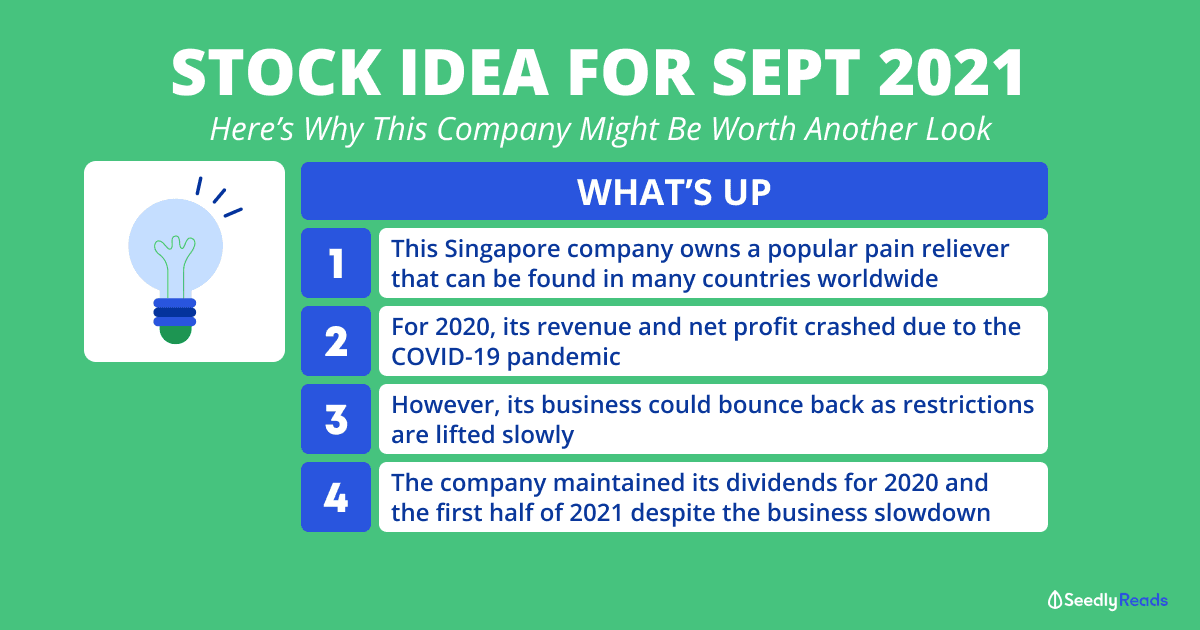

This company owns a popular pain reliever that can be found in over 100 countries.

It claims that the pain reliever is “arguably the world’s leading and most versatile topical analgesic brand”.

However, despite being a well-known healthcare brand the world over, the COVID-19 pandemic affected the company, with its overall revenue falling considerably.

Having said that, I believe the company can bounce back strongly in time to come.

The company is also one of the stocks that didn’t cut its dividend despite the headwinds from COVID-19.

This speaks well of management’s confidence in its business for the long run.

For the month of September, we are introducing Haw Par Corporation Ltd (SGX: H02) as a Singapore stock you can consider buying for the long term.

Haw Par owns the well-known Tiger Balm brand and it also has strategic stakes in two other Singapore-listed companies – United Overseas Bank Ltd (SGX: U11) and UOL Group Limited (SGX: U14).

With that, let’s find out more about Haw Par and its investment merits.

TL;DR: Haw Par — A Stock To Consider for September 2021

Here’s why Haw Par is worth another look:

- Haw Par owns the popular Tiger Balm healthcare product that’s widely used the world over.

- Its strategic stakes in UOB and UOL provide the company with a stable source of recurring dividend income.

- Haw Par maintained its 2020 total dividend and 2021 interim dividend despite the coronavirus-driven business headwinds.

- Its dividends are also well-covered, which should attract income investors who are in it for the long haul.

- Haw Par’s future looks bright, especially with a strong balance sheet that allows it to ride through the tough economic conditions and provides a dry powder for acquisitions.

Understanding Haw Par’s Business

First, let’s dive deeper into how Haw Par makes money.

The company has three main business segments, and they are “Healthcare Products”, “Investments”, and “Others”.

Here’s a breakdown of the company’s business segments and the profits that those divisions contributed in 2019 (before COVID-19):

| Business Segment | Segment Profits |

|---|---|

| Healthcare Products | S$74.8 million |

| Investments | S$114.1 million |

| Others | S$10.8 million |

| Total | S$119.7 million |

The Healthcare Products division mostly manufactures and distributes topical analgesic products under the Tiger Balm and Kwan Loong brands.

The largest contributor to the healthcare business is Tiger Balm.

The Investments division engages in investing activities, mainly in stocks listed in Asia.

Haw Par’s investment portfolio, which consists largely of strategic stakes in UOB and UOL, provides Haw Par with a stable source of recurring dividend income.

As of 30 June 2021, the strategic investments were worth around S$2.5 billion.

The Others division consists of Haw Par’s property and leisure divisions.

The property arm owns and leases out several investment properties in Asia.

The total lettable area of the property portfolio is around 45,000 square metres consisting of commercial and industrial spaces in Singapore and Malaysia.

In Singapore, Haw Par owns three leasehold properties, namely, Haw Par Centre, Haw Par Glass Tower, and Haw Par Technocentre.

In Malaysia, it has Menara Haw Par, a freehold commercial building located in Kuala Lumpur.

Meanwhile, included in the Others division is Underwater World Pattaya in Thailand, Haw Par’s leisure business.

Haw Par used to own Underwater World Singapore, but that business has ceased operations since June 2016.

Haw Par’s Five-Year Financial Highlights

Now that we have an overview of Haw Par’s business, let’s find out how the company has performed in the past couple of years.

| 2020 | 2019 | 2018 | 2017 | 2016 | |

|---|---|---|---|---|---|

| Revenue (S$’000) | 111,032 | 243,987 | 237,814 | 222,763 | 201,644 |

| Profit from Healthcare Products Division (S$’000) | 16,200 | 74,777 | 77,252 | 68,579 | 66,051 |

| Profit from Investments Division (S$’000) | 101,027 | 114,102 | 105,508 | 60,217 | 61,366 |

| Net Profit (S$’000) | 119,773 | 182,207 | 179,068 | 122,460 | 120,109 |

| Net Asset Value Per Share (S$) | 13.04 | 14.28 | 13.26 | 13.98 | 10.60 |

| Debt-to-Equity (%) | 0 | 0.2 | 0.8 | 1.5 | 2.0 |

| Total Dividend Per Share (cents) | 30 | 30 | 115 (includes 85 cents special dividend) | 20 | 20 |

We can see that from 2016 to 2019, Haw Par’s revenue, profit from both its healthcare and investments divisions and net profit have grown consistently.

However, in 2020, Haw Par’s revenue plunged 54.5% year-on-year to S$111.0 million while net profit tumbled 34.3% to S$119.8 million.

The poor performance was due to lower consumer demand for its healthcare products as movement restrictions and border closures were imposed to curb the spread of the virus.

However, there were some bright spots for the year.

Haw Par said that most of its core markets in Europe grew or maintained sales with pharmacies and para-pharmacies remaining open.

In Singapore, amid a record high number of cases of dengue infection, the Tiger Balm Mosquito Repellent range enjoyed strong sales.

For the first half of 2021, Haw Par’s revenue continued its fall, tumbling 18.6% year-on-year to S$65.8 million.

However, the decline in percentage terms was much lesser than that seen in the 2020 first-half, where the top-line crashed 43.6%.

This could mean that the worst is over for the company.

Haw Par continues to maintain a strong balance sheet with a cash hoard of S$574.5 million and no bank borrowings.

The company also held its interim dividend of 15 Singapore cents per share steady, demonstrating its ability to constantly pay well-covered dividends and management’s confidence about Haw Par’s future prospects.

Despite the lower profit for the latest period, Haw Par’s dividend payout ratio stood at a conservative 63%, given its 2021 first-half earnings per share of 23.9 cents.

With a healthy balance sheet and the ability to pay sustainable dividends, Haw Par should be able to ride through any tough economic conditions.

How Does Haw Par’s Future Like?

In Haw Par’s outlook statement for the 2021 first-half earnings, it said:

“The outbreak of the more infectious COVID-19 Delta variant around the world is likely to dampen the economic recovery in certain countries and will continue to have a negative impact on the Group’s operating businesses.”

While this may be true, I’ve noticed that Haw Par has taken a rather conservative stance in its outlook statements over the years.

For instance, for its 2019 third-quarter where the company went on to produce record revenue for the year, it mentioned:

“The Group’s businesses may face stronger headwinds if the US-China trade conflict and a slowing global economy persist. In particular, the healthcare segment may also be affected if trade sentiments and domestic issues in certain regional markets worsen.”

Despite the pandemic wreaking havoc in Haw Par’s business, the future looks bright.

With e-commerce booming as people sought shelter indoors, Haw Par picked up on the trend and has been investing more time and resources in the online space.

E-commerce revenue is still an insignificant part of its business, but it has accelerated its brand’s presence and the availability of products online by setting up Tiger Balm shopfronts on major e-commerce platforms.

Over the longer term, the ageing population and the emergence of the middle class that cares about health, fitness and well-being could provide tailwinds for Haw Par.

Also, with the Monetary Authority of Singapore (MAS) lifting the dividend cap for Singapore banks, more dividends from UOB would be flowing into Haw Par’s coffers.

With a strong balance sheet that contains lots of cash with zero borrowings, Haw Par could acquire other companies to grow its business further.

In fact, during an interview with the Singapore Exchange (SGX), the chief executive of Haw Par Wee Ee Lim mentioned:

“We’re keeping our powder dry so that we can strike when we need to – I have some years to go, and I want to build at least another leg for Haw Par for the next generation.”

Is Haw Par Cheap or Expensive?

At a share price of S$12.94, Haw Par has a trailing price-to-earnings (P/E) ratio of 35x, a price-to-book (P/B) ratio of 0.9x, and a trailing dividend yield of 2.3%.

The trailing P/E ratio is elevated due to the depressed earnings lately.

Using 2019’s earnings per share of 82.4 Singapore cents and assuming profit can bounce back, Haw Par’s P/E ratio would be around 16x, which is more palatable.

Income investors might also want to look at Haw Par since it pays sustainable dividends that are well-covered.

There’s potential for the dividend payout to increase as Haw Par’s business grows further.

Do You Want Free Seedly Exclusive Stock Deep Dive Reports?

We’ve released stock deep dive reports on a couple of companies. Grab hold of them at Seedly Rewards right now!

Disclaimer: The information provided by Seedly serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any stock. The writer doesn’t own shares in any companies mentioned.

Advertisement