Due to the COVID-19 outbreak, the economy has weakened significantly.

This has affected individuals and businesses, where there might be challenges in meeting financial obligations and managing cash flows.

In view of this, the Monetary Authority of Singapore (MAS) has collaborated with financial institutions to roll out a package of measures to assist individuals and Small and Medium Enterprises (SMEs) which are facing temporary cash flow difficulties, to help them weather the storm.

The Special Finance Relief Programme (SFRP) is established to provide relief measures to bank customers, helping to ease any financial burden and still be able to access basic banking services during this difficult period.

This would be helpful for you if you are someone with loans, be it from housing, renovation, credit cards or education.

In this article, we explore the features of the programme, and what assistance it could provide you.

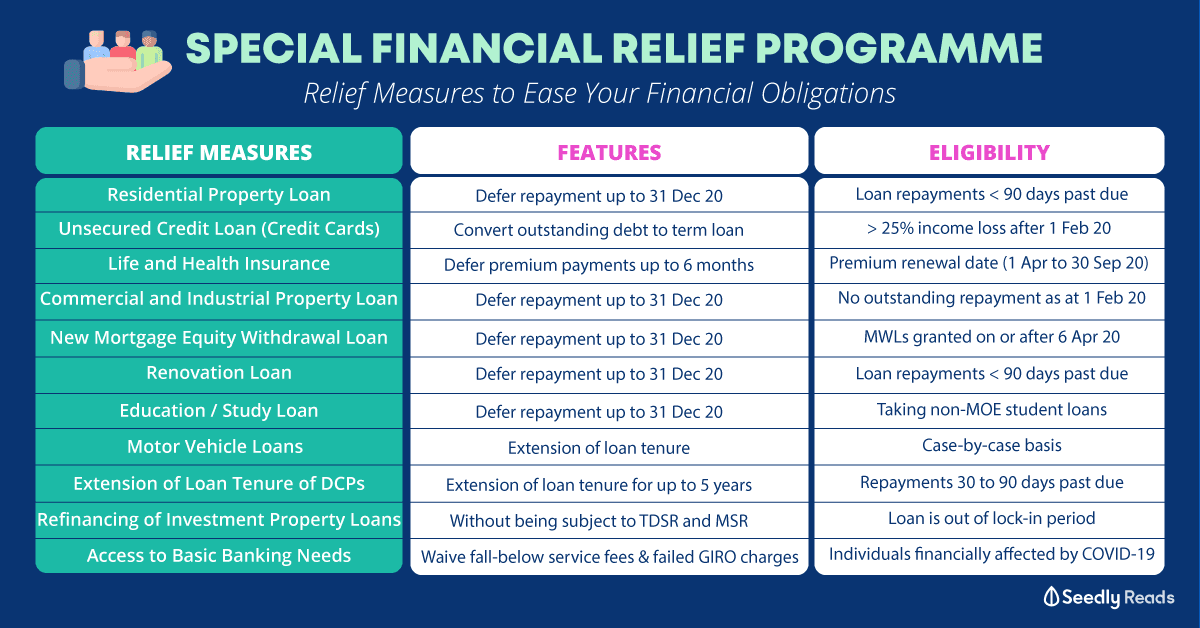

TL;DR: Special Finance Relief Programme (SFRP) – COVID-19 Loans Support in Singapore

| Objective | Relief Measures | Features | Eligibility |

|---|---|---|---|

| Ease Cashflow Through Deferment of Repayment | Housing Loans | - Defer repayment of principal or both principal and interest up to 31 Dec 2020 - Interest-on-interest is waived | Borrowers with mortgage repayments no more than 90 days past due (as at 6 Apr 2020) |

| Personal Unsecured Credit (e.g. Credit Cards) | - Convert outstanding unsecured debt to a term loan (from 6 Apr to 31 Dec 2020) - Effective interest rate capped at 8% - Tenure up to 5 years | Borrowers with at least 25% income loss after 1 Feb 2020 | |

| Life and Health Insurance | - Defer premium payments up to six months while maintaining insurance coverage | Policyholders with premium due date or policy renewal date between 1 Apr to 30 Sep 2020 | |

| Commercial and Industrial Property Loans | - Defer repayment of principal up to 31 Dec 2020 - Ability to extend the loan tenure by up to corresponding deferment period | For borrowers with no outstanding repayment as at 1 Feb 2020 | |

| New Mortgage Equity Withdrawal Loans Granted | - Defer repayment of principal or both principal and interest up to 31 Dec 2020 - Interest-on-interest is waived | Borrowers with mortgage equity withdrawal loans (MWLs) that are granted on or after 6 Apr 2020 | |

| Renovation Loans | - Defer repayment of both principal and interest up to 31 Dec 2020 - Interest-on-interest is waived | Borrowers whose loan repayments are no more than 90 days past due at the point of application | |

| Education / Study Loans | - Defer repayment of both principal and interest up to 31 Dec 2020 - Interest-on-interest is waived | Borrowers whose loan repayments are no more than 90 days past due at the point of application | |

| Motor Vehicle Loans and Hire-Purchase Agreements | Extension of loan tenure by up to the corresponding deferment period | Case-by-case basis, subjected to assessment | |

| Ease Cashflow Through Extension of Loan Tenure | Extension of Loan Tenure of Debt Consolidation Plans (DCPs) | Extend loan tenure of existing DCP for up to 5 years (18 May to 31 Dec 2020) - Will not cause loan to be reflected as a restructured loan | Borrowers with income impacted by COVID-19, and repayments are between 30 and 90 days past due during application |

| Reduce Debt Obligations | Easier Refinancing of Investment Property Loans | Refinance or Reprice Investment Property Loans without being subject to the total debt servicing ratio (TDSR) and mortgage servicing ratio (MSR) | Loan is out of lock-in period |

| Ensure Access to Basic Banking Needs | - Waive Fall-Below Service Fees Waive Failed Giro Deduction Charges for Retail Bank Accounts | - Fall-below service fees waived up to 31 Dec 2020 - Failed deductions from GIRO arrangements will have bank fees waived up to 31 Dec 2020 | Individuals with income impacted by COVID-19 |

Do note that all of these schemes are on an opt-in basis, and are subject to different eligibilities.

The application can be done online at the respective bank websites:

1. Deferring Repayment of Residential Property Loan (Housing Loans)

For most adults, the biggest loan to have would be housing loans.

Under the SFRP, individuals could opt to defer either the principal payment, or both principal and interest payments up to 31 December 2020.

The interest will only accrue on the deferred principal amount, and no interest would be charged on the deferred interest payments (i.e. no interest-on-interest).

To be eligible, individuals should not be in arrears for more than 90 days as of 6 April 2020.

There is also no need to prove any financial impact that has occurred from COVID-19 in order to obtain this deferment.

However, do note that there will be additional interest that will accrue over the deferment period, in which the loan amount together with this additional interest will be fully amortised over the remaining loan tenure.

2. Lower Interest Rates on Personal Unsecured Credit (Credit Cards and Other Revolving Credit Lines)

For the uninitiated, unsecured loans refer to loans which are not backed by any assets.

This means that the lender does not have any collateral that can be repossessed, in an event the borrower is unable to repay the debt.

One of such loans would be credit cards.

Under this programme, borrows can choose to convert their outstanding unsecured debt from credit cards (or any other revolving credit lines) to a term loan at reduced interest rates, anytime from 6 April to 31 December 2020.

The effective interest rate is capped at 8%, which is much lower than the 26% which is typically charged for credit cards.

Borrowers can choose the term of the loan of up to five years, depending on his/her ability to meet the monthly repayment.

In order to qualify for this, individuals have to provide the loss of 25% (or more) of monthly income after 1 February 2020, and must be between 30 to 90 days past due for existing unsecured debt.

3. Deferring Repayment of Life and Health Insurance

For life and health insurance policyholders, there is an option to defer premium payments for up to six months, while maintaining insurance coverage during the deferment period.

This applies to all individual life and health insurance policies with a renewal or premium due date between 1 April 2020 to 30 September 2020.

This initiative will supplement the existing premium relief options, which includes taking a premium loan against the policy cash value, or converting to a paid-up policy by reduction of the sum assured.

4. Deferring Repayment of Commercial and Industrial Property Loans

For existing loans which have been taken to purchase commercial or industrial properties, borrowers can opt to defer repayment of the principal loan, up to 31 December 2020.

The loan tenure can be extended by up to the corresponding deferment period.

This deferment will not cause the loan to be reflected as a restructured loan in the borrowers’ credit bureau report.

To be eligible, borrowers must not have any outstanding repayment as at 1 February 2020.

Borrowers are also not subject to the total debt serving ratio (TDSR) when applying for deferment.

However, as with the other loan repayment deferments, it is worth noting that there is also interest accrued during the deferment period.

5. Deferring Repayment of New Mortgage Equity Withdrawal Loans

This is for mortgage equity withdrawal loans which are secured on residential, commercial and industrial properties.

This is for borrowers with mortgage equity withdrawal loans that are granted on or after 6 April 2020.

For this, borrowers can choose to defer repayment of principal of both principal and interest, up to 31 December 2020.

The options may vary between different financial institutions.

Interest-on-interest will be waived for any deferred principal amount, and borrowers can choose to extend the mortgage tenure by up to the corresponding deferment period.

Similarly, this deferment will also not be reflected as a restructured loan in the borrowers’ credit bureau.

6. Deferring Repayment of Renovation Loans

For those who have been constructing their dream homes and have taken a renovation loan, there is an option to defer repayment on both the principal and interest amounts, up to 31 December 2020.

Interest-on-interest will also be waived for this deferment.

To be eligible, borrowers should have loan repayments that are no more than 90 days past due at the point of application.

One thing to note would be that interest would be accrued from the deferment period.

Therefore, it is important to weigh these options carefully, as deferring payments might increase future obligations.

7. Deferring Repayment of Education or Study Loans

For students who are currently on education loans, you can also choose to defer repayment too!

Do note that this is only for full-time or part-time programmes at local and foreign private tertiary institutions (i.e taking non-MOE student loans).

Similarly, students can choose to defer repayment on both the principal and interest amounts, up to 31 December 2020.

Interest-on-interest will also be waived for this deferment.

However, interest would still be accrued from the deferment period, which might increase future financial obligations.

8. Deferring Repayment of Motor Vehicle Loans and Hire-Purchase Agreements

Individuals who have car loans and hire-purchase agreements and require payment deferment can approach their respective financial institutions to discuss suitable repayment plans.

The institution will assess this on a case-by-case basis, based on factors such as the borrowers’ financial condition, the need for use of the vehicle, the vehicle’s current market value etc.

If the deferment is granted, borrowers can discuss with the institution on the loan tenure extension by up to the corresponding deferment period.

Similarly, this deferment will not cause the loan to be reflected as a restructured loan.

9. Extending Repayment of Debt Consolidation Plans (DCP)

Debt Consolidation Plans (DCPs) are plans which allow customers to consolidate all his unsecured credit lines (such as credit cards) from different financial institutions, into one financial institution.

There are currently 14 participating financial institutions:

- American Express International, Inc.

- Bank of China Limited Singapore

- CIMB Bank Berhad

- Citibank Singapore Limited

- DBS Bank Ltd

- Diners Club Singapore Pte Ltd

- HL Bank

- HSBC Bank (Singapore) Limited

- Industrial and Commercial Bank of China Limited

- Standard Chartered Bank (Singapore) Limited

- Maybank Singapore Limited

- Oversea-Chinese Banking Corporation Limited

- RHB Bank Berhad

- United Overseas Bank Limited

Under SFRP, borrowers who are on DCP can apply to extend the loan tenure of their existing plans for up to 5 years, anytime from 18 May 2020 to 31 December 2020.

This extension will not cause the loan to be reflected as a restructured loan in the borrowers’ credit bureau report.

To be eligible, borrowers must be financially impacted by COVID-19, with repayments between 30 and 30 days past due at the point of application.

10. Easier Refinancing or Repricing of Investment Property Loans

This is for individuals who have taken loans to purchase residential, commercial and industrial properties.

Individuals with these loans that are out of the lock-in period can apply to refinance or reprice their loans, without being subject to the total debt servicing ratio (TDSR) and mortgage servicing ratio (MSR), up to 31 December 2020.

In addition, borrowers who do not meet TDSR or MSR do not need to commit to a debt repayment plan to repay 3% of their outstanding loan amount over three years.

As such, this exemption would lower monthly repayments.

However, do note that contractual penalties may apply if the loan is still within the lock-in period.

11. Waiver Of Fall-Below Bank Account Service Fees and Failed GIRO Deduction Charges

For individuals who have their incomes affected by COVID-19, there is a waiver of retail bank account service fees.

Fall-below service fees can be waived up to 31 December 2020, when the average monthly bank balance is not met.

Bank fees incurred from any failed GIRO deductions (from GIRO arrangements which have been set up for payments, such as phone bill or electricity bills) will also be waived up to 31 December 2020.

Advertisement