It wasn’t too long ago that the Standard Chartered BonusSaver savings account’s revised (lowered) interest rates took effect.

But guess what?

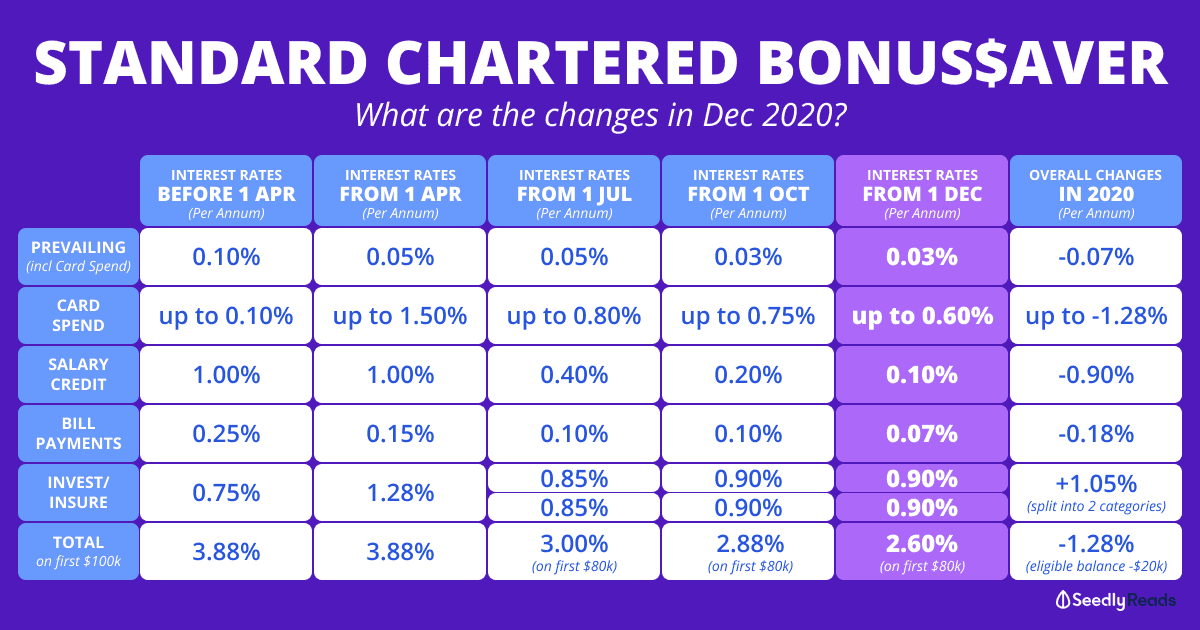

With effect from 1 December 2020, there will be yet another reduction of interest rates.

This doesn’t bode well…

TL;DR: Changes to Standard Chartered BonusSaver Interest Rates

The highest bonus interest rate will drop from up to 2.88% p.a. to… up to 2.60% p.a. on the first $80,000 of your eligible deposit balance.

It goes without saying that the bonus interest which you can earn under categories like Salary Credit, Bill Payment, and Card Spend will be hit too.

The only silver lining?

If you’re currently fulfilling and benefitting from the Invest and Insure categories, the interest rates for those remain unchanged.

Revision of Interest Rates for Standard Chartered BonusSaver From 1 December 2020

| Bonus Interest Categories For First $100,000 | Interest Rate |

|---|---|

| Monthly Salary Credit (≥$3,000) | 2.00% |

| Monthly Card Spend | 0.65% ($500 - $1,999 a month) |

| 1.45% (>$2,000 a month) | |

| Bill Payments (Make Min. 3 Eligible Bill Payments of $50 Each) | 0.23% |

| Invest (Invest in Eligible Products with a minimum subscription of S$30,000) | 2.00% for 12 months |

| Insure (Buy Eligible Insurance Products with a minimum annual premium of S$12,000) | 2.00% for 12 months |

All the Changes to Standard Chartered BonusSaver in 2020

This is the fourth time this year that Standard Chartered is making changes to the interest rates of their Standard Chartered BonusSaver savings account.

Here are the changes at a glance.

Prevailing Interest: A decrease of 0.07% p.a.

Card Spend: A decrease of 0.63% p.a. if you spend between $500 and $2,000, and a decrease of 1.28% p.a. if you spend more than $2,000 a month

Salary Credit: A decrease of 0.90% p.a.

Bill Payments: A decrease of 0.18% p.a.

Invest: Separated from the Insure category, with an overall increase of 1.05% p.a. when both are combined

Total Bonus: A decrease of 1.28% p.a. with the total eligible balance lowered by $20,000 to $80,000

Is it Still Worth Opening a Standard Chartered BonusSaver Account After 1 December 2020?

TBH, I used to like that you could get up to 3.88% p.a. interest on a high balance cap of $100,000.

Note: for most savings accounts, the amount of bonus interest you can earn drops drastically once your balance goes past $75,000 (the sum insured by Singapore Deposit Insurance Corporation).

Even though you have to jump through a couple of (pretty standard) hoops to qualify for the various bonus interest categories.

However, the 1 December 2020 revision is just one of the (too) many revisions this year which will nerf the Standard Chartered BonusSaver Account even further.

So much so that you will only get up to 2.60% p.a.on the first $80,000 in your bank account.

.

.

.

“Is it worth opening a Standard Chartered BonusSaver account after 1 December 2020,” you ask?

If you are already holding onto this account, you probably already have your salary credited, bills set up, and are constantly using Standard Chartered cards for your expenditure.

Assuming you earn at least $3,000 and spend at least $2,000 a month (aside: this is NOT an ideal salary allocation).

Oh, and you also make 3 bill payments of $50 each while somehow managing to maintain a daily average balance of $80,000.

You’re looking at an interest rate of 0.77% p.a. (or $640 interest earned) assuming you don’t invest or insure with Standard Chartered.

I mean… it’s much better than the paltry 0.05% p.a. you get by leaving your money in a regular bank savings account.

But since you’ve already got everything set up.

I would weigh my options carefully if I want to switch to another high-interest savings account.

Because looking at the current low-interest-rate environment we’re in, I wouldn’t be surprised if the other banks will revise their rates further too.

Investing and Insuring with Standard Chartered

However, if you plan to invest and insure with Standard Chartered.

Meaning you want to buy at least $30,000 worth of unit trusts every year.

And need coverage to the amount of $12,000 annually in insurance premiums.

Then, the Standard Chartered BonusSaver is definitely a worthy contender.

Perhaps if they opened their Invest category to also include transactions clocked under their Standard Chartered Trading Account…

Then this might make more sense for investors who are already actively using their online brokerage since it has one of the lowest fees in the market.

Should I Park My Money in the Standard Chartered BonusSaver?

If you’ve got spare cash lying around and don’t want to jump through so many hoops just to get the bonus interest.

You might want to look at other fuss-free options such as Singapore Savings Bonds (but the interest rates aren’t great either).

Or even an insurance savings plan.

Alternatively, you could look for other fuss-free high-interest savings accounts which can do the same (or better) for you.

Just use our FREE Savings Account Calculator and see for yourself.

It’ll only take you less than a minute.

Advertisement