There was once where I almost fainted on the train.

I was out with my friend, and being adventurous, we decided to take on a 1-for-1 beer cocktail drink at Holland V.

It was just one drink, and while my tolerance isn’t the best, I was pretty sure that one drink wouldn’t kill me.

Maybe it was the mix of cheap hard liquor and beer, coupled with the incessant jerking of the MRT train, or the fact that I was sick.

Whatever it was, I felt my vision blurring and my surroundings caving in.

Thank god for my friend, who dragged me out of the train and to a nearby bench.

The point of the story is, we won’t know what will happen to us.

Be it now, or a few decades down the road.

That’s why some of us decide to get insurance, because when life throws shit at you, at least you’d get some sort of protection.

Life insurance basically helps you with that.

For the initiated, life insurance protects you in the unfortunate event where something bad happens to you.

In the case of death, your family or loved ones will get a sum assured.

Why Should I Get Life Insurance?

“Do I need life insurance?”

If you satisfy most of these categories, getting life insurance may be something worth considering:

1. If You Are The Sole Breadwinner Of Your Family

This will help your spouse to sustain the current family’s lifestyle while giving him/her time to find a job.

2. If You Have Dependants

Meaning children who are not financially self-reliant yet, and/or parents you provide for their retirement.

3. If You Have Outstanding Liabilities

Whether it is an education loan or mortgage loan, you should get yourself insured so as to not pass your burden on to your family. Life insurance provides:

- A payout to your family in an unfortunate event of your passing

- A form of income replacement for your family members to tide them over the first few years

It’s arguably the best way to provide some form of income for your family when you are no longer around.

What Are Term Life Policies?

A term life policy is life insurance that provides coverage at a fixed rate of payments for a defined period of time.

As long as you pay your premiums, you’ll be covered.

They’re also used as a short-term solution when you feel that your existing coverage is insufficient.

Term Life Or Whole Life Insurance?

| Whole Life | Term Life |

|---|---|

| Participating (Par) | As long as you pay premiums, you're covered. |

| Non-participating (Non-par | 15/25/30 years or even up to age 65/100 |

| Investment-linked policies (ILP) |

Before choosing Term Life or Whole Life Insurance:

- Never lose focus on your objective – why are you buying insurance?

- Life Insurance Association Singapore suggests that coverage of 11 times your annual earnings is the most optimal, but it really is relative to your lifestyle.

Advantages & Disadvantages Of Term Life and Whole Life

| Whole Life | Term Life |

|---|---|

| Advantages | |

| Limited Pay: Pay premium for a predetermined fixed period (E.g. 20 years) | Premiums are cheaper per month |

| Covers for life (Up to age 99) | Straight Forward |

| Has CASH VALUE | You lose coverage the moment you stop paying your premiums |

| Disadvantages | |

| Complicated | NO CASH VALUE |

If you would like to know more in-depth about Term Life or Whole Life insurances, you can refer to this Seedly Article for a more in-depth explanation of the differences between Term Life and Whole Life.

Here’s a comparison of the different Term Life Insurance you can get for those looking to buy term life insurance policies.

Do note, however, that I write this with a pinch of salt. Everyone has different needs and getting a life or term insurance is very much tailored to a person’s needs. The lowest premiums or the ones offering the highest payouts do not necessarily mean it’s the best plan for you, so make sure you research beyond this article before buying your life insurance.

Term Life Insurance That You May Currently Have:

Here are some term life insurance that’s been set-up for us by the government.

1. Dependants’ Protection Scheme (DPS) – By CPF

![]()

- Sum assured of S$46,000 (maximum)

- Optional

- Automatically opted-in by the Government when you turn 21 years old

- Premiums are deducted from your CPF

2. SAF Group Term Life Insurance Scheme

- Cheap and affordable

- Offered to all SAF NSmen age 55 and below and Dependants of the SAF NSmen

(i.e. $41/month for S$1 million coverage)

A Cross-Comparison Of Term Life Insurance

Direct Purchase Term Life Insurance

Term Life Direct Purchase Insurance (DPI) is a life insurance scheme that lets consumers purchase a term life insurance plan directly through the insurer without going through an intermediary such as a financial advisor. Like the usual term life insurance, it offers protection for a fixed amount of time and will only pay out the sum assured if death, terminal illness or total and permanent disability occurs within the period insured.

Here are the premiums and coverages for the different plans:

5 Year Plan Tenure

| Name Of Policy | Plan Tenure | Premium (From Age 25-45) | Death and TPD Coverage |

|---|---|---|---|

| FWD Direct Purchase Term Life Insurance | 5-Years | S$4.61-S$7.18 | S$50,000 |

| 5-Years | S$9.40-S$25.40 | S$200,000 | |

| 5-Years | S$16.70- S$36.19 | S$400,000 | |

| Etiqa Direct Purchase Term Life Insurance | 5-Years | S$2.19-S$5.97 | S$50,000 |

| 5-Years | S$6.80- S$18.56 | S$200,000 | |

| 5-Years | S$18.14-S$44.53 | S$400,000 | |

| Great Eastern Direct Purchase Term Life Insurance Apply Now | 5-Years | S$3.96-S$7.67 | S$50,000 |

| 5-Years | S$9.17-S$24.00 | S$200,000 | |

| 5-Years | S$18.33- S$48.00 | S$400,000 | |

| SingLife Direct Purchase Term Life Insurance | 5-Years | S$2.78-S$5.58 | S$50,000 |

| 5-Years | S$9.51-S$20.71 | S$200,000 | |

| 5-Years | S$17.39-S$39.82 | S$400,000 | |

| Etiqa eProtect Term Life Insurance | 5-Years | S$16.19-S$44.19 | S$500,000 |

| 5-Years | S$29.14-S$79.54 | S$1,000,000 | |

| 5-Years | S$51.80-S$141.40 | S$2,000,000 | |

| FWD Term Life Insurance | 5-Years | S$20.45-S$45.24 | S$500,000 |

| 5-Years | S$29.58-S$87.87 | S$1,000,000 | |

| 5-Years | S$52.20-S$161.82 | S$2,000,000 | |

| SingLife Term Life Insurance | 5-Years | S$24.12-S$46.95 | S$500,000 |

| 5-Years | S$40.28-S$79.03 | S$1,000,000 | |

| 5-Years | S$80.58-S$158.05 | S$2,000,000 |

20 Year Plan Tenure

| Name Of Policy | Plan Tenure | Premium (From Age 25-45) | Death and TPD Coverage |

|---|---|---|---|

| FWD Direct Purchase Term Life Insurance | 20-Years | S$4.61-S$12.14 | S$50,000 |

| 20-Years | S$11.14-S$42.28 | S$200,000 | |

| 20-Years | S$18.44-S$67.16 | S$400,000 | |

| Etiqa Direct Purchase Term Life Insurance | 20-Years | S$2.54-S$8.09 | S$50,000 |

| 20-Years | S$7.90-S$36.93 | S$200,000 | |

| 20-Years | S$15.05-S$70.35 | S$400,000 | |

| Great Eastern Direct Purchase Term Life Insurance Apply Now | 20-Years | S$4.38-S$12.08 | S$50,000 |

| 20-Years | S$10.83-S$41.67 | S$200,000 | |

| 20-Years | S$21.68-S$83.33 | S$400,000 | |

| SingLife Direct Purchase Term Life Insurance | 20-Years | S$2.65-S$9.62 | S$50,000 |

| 20-Years | S$8.98-S$36.88 | S$200,000 | |

| 20-Years | S$16.36-S$72.15 | S$400,000 | |

| Etiqa eProtect Term Life Insurance | 20-Years | S$18.81-S$93.19 | S$500,000 |

| 20-Years | S$33.86-S$167.74 | S$1,000,000 | |

| 20-Years | S$60.20-S$298.20 | S$2,000,000 | |

| SingLife Term Life Insurance | 20-Years | S$28.74-S$105.27 | S$500,000 |

| 20-Years | S$47.95-S$175.82 | S$1,000,000 | |

| 20-Years | S$95.90-S$351.64 | S$2,000,000 | |

| FWD Term Life Insurance | 20-Years | S$23.93-S$93.09 | S$500,000 |

| 20-Years | S$34.80-S$174.87 | S$1,000,000 | |

| 20-Years | S$59.16-S$349.74 | S$2,000,000 |

Term Life Insurance Till Age 65

| Name Of Policy | Plan Tenure | Premium (From Age 25-45) | Death and TPD Coverage |

|---|---|---|---|

| FWD Direct Purchase Term Life Insurance | Age 65 | S$6.36-S$11.44 | S$50,000 |

| Age 65 | S$18.62-S$40.72 | S$200,000 | |

| Age 65 | S$29.93-S$66.82 | S$400,000 | |

| Etiqa Direct Purchase Term Life Insurance | Age 65 | S$5.14-S$11.40 | S$50,000 |

| Age 65 | S$15.99-S$35.46 | S$200,000 | |

| Age 65 | S$30.45-S$67.55 | S$400,000 | |

| Great Eastern Direct Purchase Term Life Insurance Apply Now | Age 65 | S$6.33-S$11.71 | S$50,000 |

| Age 65 | S$18.67-S$40.17 | S$200,000 | |

| Age 65 | S$37.33-S$80.33 | S$400,000 | |

| SingLife Direct Purchase Term Life Insurance | Age 65 | S$4.56-S$10.51 | S$50,000 |

| Age 65 | S$16.63-S$40.42 | S$200,000 | |

| Age 65 | S$31.64-S$79.23 | S$400,000 | |

| Etiqa eProtect Term Life Insurance | Age 65 | S$38.06-S$54.69 | S$500,000 |

| Age 65 | S$68.51-S$159.86 | S$1,000,000 | |

| Age 65 | S$121.80-S$284.20 | S$2,000,000 |

Which One Should I Get? 5 Years, 20 Years, or Till Age 65 Plan?

When it comes to determining your policy period, you can determine your policy period based on your age.

If you’re in your 20s, a longer-term (till age 65) policy is advisable.

If you’re in your 50s, you can consider a 20-year term life insurance policy. If you’re looking for a high cover, low-premium term plan, you should buy your term insurance at an earlier stage to enjoy lower premiums. Once fixed, premiums usually remain the same for the entire policy period.

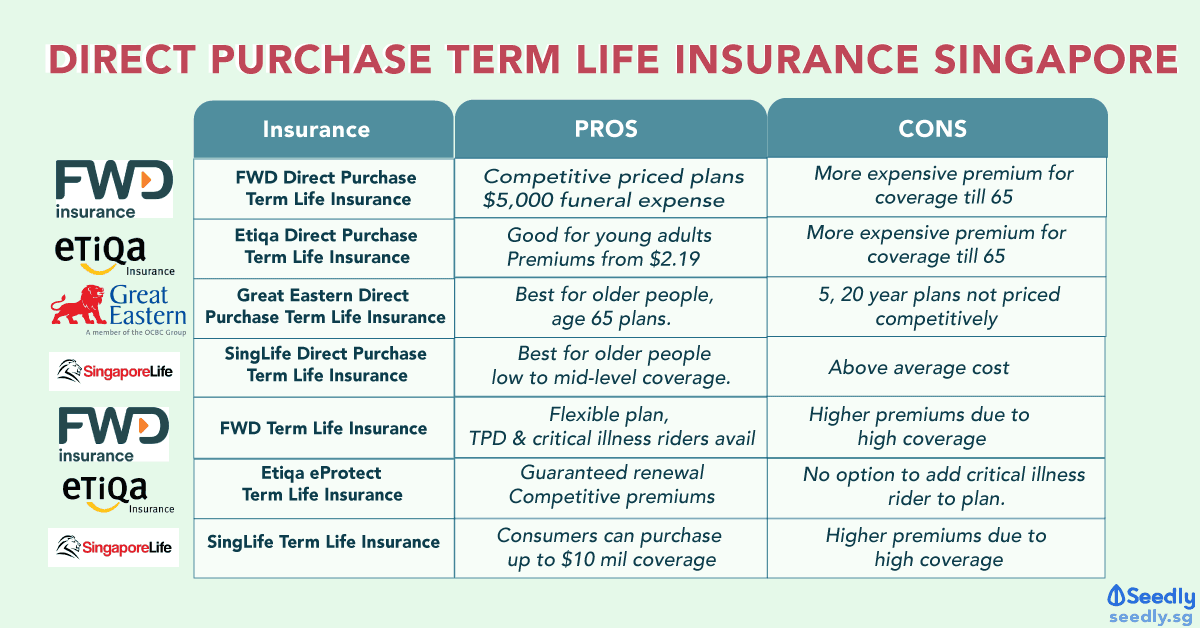

Which One’s Best For Me?

| Pros | Cons | Company Credit Rating | |

|---|---|---|---|

| FWD Direct Purchase Term Life Insurance | Competitive priced plan with lower premiums, regardless of gender. S$5,000 for funeral expenses paid by the next business day after they receive the death certificate | Not the cheapest plan to get for those looking for coverage till age 65. | BBB- |

| Etiqa Direct Purchase Term Life Insurance | One of the most affordable plans for young, non-smoking adults. Premiums start from $2.19. Enjoy 5% savings if you pay annually instead of monthly | Above average premiums for those looking at age 65 plans | A- |

| Great Eastern Direct Purchase Term Life Insurance Apply Now | Best for older Singaporeans looking for up to age 65 plans. Premiums from $6.33 | Less competitively priced for 5 to 20 year tenure plans for younger consumers. Age is defined as age at next birthday, as opposed to other plans that define your age as the age of your previous birthday, decreasing your total coverage by one year | AA- |

| SingLife Direct Purchase Term Life Insurance | Best for older consumers over 50 looking for low to mid-level coverage. Traditional online term life plan offers competitive coverage. Offers coverage up to $400,000 as well as critical illness riders. | Costs above average for most users. | BBB |

| FWD Term Life Insurance | Flexible design: You can renew your policy each year, or a fixed term policy where you pay the same premiums throughout the selected period. TPD benefit and critical illness benefit available as rider. | Higher premiums greater death and TPD coverage | BBB- |

| Etiqa eProtect Term Life Insurance | 5-year policy term has guaranteed renewal. Competitive premiums among $1,000,000 coverage plan for young peopl and $2,000,000 for middle-aged consumer. | No option to add critical illness rider to plan. | A- |

| SingLife Term Life Insurance | Allows consumers to purchase up to S$10,000,000 of death and terminal illness coverage online. | Higher premiums due to high coverage. | BBB |

Traditional Term Life Insurance

What’s the difference?

Traditional Term Life Insurance is usually purchased directly from your insurance agent. Unlike direct-purchase term life insurance, traditional term life insurance also offer benefits such as guaranteed renewal, inflation protection, an option to convert term to life insurance, and increased coverage for certain life milestones. These are on top of the usual death, total permanent disability, and terminal illness coverage.

Here’s a non-exhaustive list of Term Life Insurance:

| Term Life Policy | Max Age for Coverage | Coverage | Additional Benefits |

|---|---|---|---|

| NTUC Income DIRECT - Term (renewable) | 84 | Death, Terminal Illness, Total Permanent Disability (before age 65) $400,000 coverage | Sum Assured |

| NTUC iterm | 84 | Death, Total Permanent Disability, Terminal Illness | Guaranteed renewal |

| NTUC TermLife Solitaire | 100 | Death, terminal illness | Min. S$1 million coverage, 1-time Medical concierge |

| NTUC Lady 360 | 64 | Death | Screening benefit, illness benefit, surgery benefit, support benefit, multiple policy claims, premium waiver |

| Raffles Medical Preferred Life Protector | N/A | Death, total permanent disability | Daily Hospital Income (some plans), Available for kids |

| AXA Term Protector Prime | 99 | Death, terminal illness | Preferred currency, convertibility to whole life, automatic renewability, cash benefit riders for business protection |

| AIA Secure Flexi Term | 101 | Death, terminal illness | Terminal Cancer benefit Renewable term option, choice of coverage up to age 65, 75 or 100. |

Things To Look Out For When Considering Buying A Term Life Insurance

1. The insurance’s company market reputation

Finding out the market reputation is important to get a sense of the insurer’s ability to settle payouts efficiently. One way of measuring this is through looking at the company’s credit rating.

An insurance company credit rating is the opinion of an independent agency regarding the financial strength of an insurance company. An insurance company’s credit rating indicates its ability to pay policyholders’ claims.

Here’s a gauge on how insurance companies and their products are being rated:

| S&P/ Fitch Rating | Rating Description |

|---|---|

| AAA | Prime |

| AA+ | High Grade |

| AA | |

| AA- | |

| A+ | Upper Medium Grade |

| A | |

| A- | |

| BBB+ | Lower Medium Grade |

| BBB | |

| BBB- |

Source: Investment Moats

When buying life insurance, looking at the insurance company’s credit rating is important to ensure that you get a reliable insurer.

2. Conversion feature

If you’re looking into term life insurance, it’s good to choose one that has a conversion policy. The conversion feature would allow you to keep your coverage, in an event where you developed any medical conditions since your initial term purchase. You may not be able to qualify if you were to go back out to the market for a new policy.

3. Affordability

If you buy a policy that’s affordable, you’ll be much more likely to be able to hold onto it if you have to make any serious cuts to your budget. Life insurance is a long term investment, so make sure you choose one with a premium that you can afford in the long run.

Advertisement