Worried About Your Parents' Retirement? You Might Want To Take A Look At HDB's Silver Housing Bonus Scheme!

Maybe this isn’t something that you are likely to discuss with your circle of friends, but worrying about our parents’ retirement is a common issue…

Or worse, you’ve just started planning for your retirement and you’re worried that you might not have enough to sustain your daily needs in the future?

Erm, have you even started planning?

Apart from the HDB Lease Buyback Scheme, the Housing & Development Board (HDB) has another trick up its sleeve to help supplement the retirement income for yourself or your parents.

TL;DR – The Ultimate Guide To Silver Housing Bonus (SHB) Scheme

Hang on, don’t get too excited!

There are some conditions you need to meet before you are eligible for SHB.

| Criteria | Eligibility |

|---|---|

| Age & Citizenship | At least one owner is a Singapore Citizen aged 55 or above |

| Income | Gross monthly household income is within $14,000 |

| Existing Property | HDB flat (met Minimum Occupation Period for resale), or |

| Private property of Annual Value of $13,000 or less; and | |

| No concurrent ownership of second property | |

| Property You Are Buying | 3-room (excluding 3-room terrace) or smaller; and |

| of a smaller room type than the last sold property; and | |

| Purchase price does not exceed selling price of the current/last sold property | |

| Housing Transactions | Booking of new HDB flat, or application to buy resale flat must be: |

| before sale of existing property; or | |

| within 6 months of completing sale of existing property |

Since there are so many possible scenarios, we decided to make an assumption that you’ve sold a 4-room flat to right-size to a 2-room Flexi flat.

Bear in mind though, that you should always do your homework and assess if this is the best option for your situation!

Who Qualifies For The Silver Housing Bonus?

Before we dive into how the Silver Housing Bonus (SHB) works, let’s take a look at the conditions that your household needs to meet before you can qualify for the SHB.

Citizenship & Age

Similar to the Lease Buyback Scheme, at least one of the flat owners have to be a Singapore Citizen.

The SHB is less strict as it requires the Singapore Citizen flat owner to be age 55 and above.

Household Income

Likewise, the scheme aims to provide help for the lower-income group.

Your household will meet the income eligibility if the gross monthly income for the entire household does not exceed $14,000.

Current Property

Of course, the current property that you are residing in and planning to sell needs to be an HDB flat.

If your household is residing in a resale flat, you are also required to have met the Minimum Occupation Period before you are eligible.

Yea, we know… The ability to purchase private property in the past is not a good indicator of your current financial situation.

Good news! Owners of private property with an Annual Value of $13,000 or less can also apply for the Silver Housing Bonus if they meet the remaining criteria.

The next one is kinda duh, but you must not be owners of a second property.

Property You Are Purchasing

Needless to say, the property that you are buying needs to be of a smaller room type than the last sold property since the scheme is about right-sizing. I feel like I’m being Captain Obvious here…

More specifically, the property should be 3-room (excluding 3-room terrace) or smaller. It’s just a nicer way of saying that you can only choose between a 3-room flat or a 2-room Flexi flat.

Lastly, the flat that you are buying should not be more expensive than the amount at which you sold your current property.

Housing Transactions

Unlike investing, timing matters for the SHB, guys!

I guess HDB knows that while having a roof over our heads is important, some processes take longer and you can get very busy dealing with them.

So, whether you’re booking a new HDB flat or applying for a resale flat, just make sure that you do so before you sell your current property, or within 6 months of completing the sale of your said property.

Don’t dilly-dally lah, guys…

How Much Can I Get From Right-Sizing?

Step 1 – Right-Size To Smaller Flat

Okay, I’m being Captain Obvious again, but yes, you first need to decide if you want to buy a 2-room Flexi or 3-room flat and whether you’ll be buying from the resale market or from HDB.

So let’s say you are one of the flat owners of a rather old 4-room HDB flat and will be booking a new 2-room flat with HDB…

Psst… You’ll probably have a rather high chance of getting a 2-room Flexi flat if it’s within 4km of your current flat or your children’s flat.

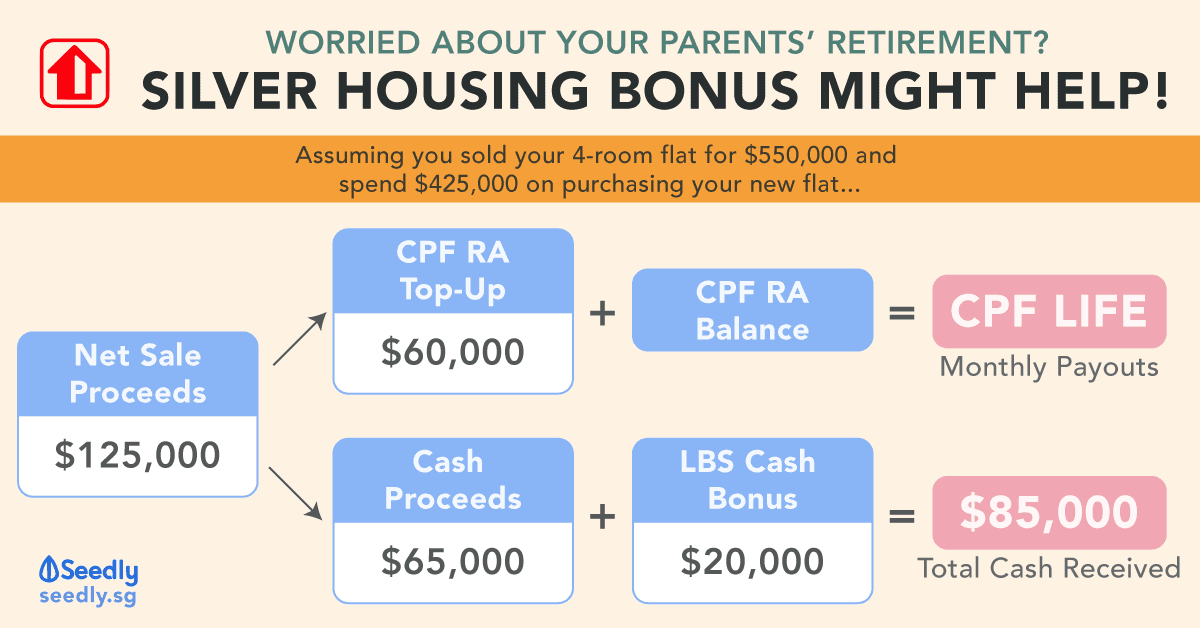

Step 2 – Calculate Net Sale Proceeds

Given the eligibility conditions, you will definitely have sale proceeds from right-sizing your flat.

Unfortunately, calculating your HDB sales proceeds is not as easy as taking the difference between the amount you sold your house and the amount you bought your new flat.

If only selling houses were as easy as selling clothes for cash…

With our example of right-sizing from a 4-room flat to a 2-room Flexi flat, here’s how your sale proceeds will be calculated.

| Selling price of existing property | $550,000 |

|---|---|

| Outstanding loan on existing property | less $80,000 |

| Refund to CPF Ordinary Account | less $150,000 |

| Resale levy | less $40,000 |

| Ancillary Costs | less $15,000 |

| Cash used to purchase next property | less $140,000 |

| Net Sale Proceeds | $125,000 |

As you can see, there are several factors that can affect how much you’ll receive in the end.

You’ll definitely be receiving more if you took a smaller loan many years ago, or have been making voluntary housing refunds back to your CPF along the way.

The amount you need to pay for your resale levy also depends on the flat type of your current property, the larger your property, the more you’ll need to pay. If you were intending to purchase a resale flat instead, then you don’t need to pay a resale levy.

You may potentially be paying lesser for your ancillary costs, but we’ve used HDB’s limit of $15,000 in this scenario.

Of course, depending on the type of flat chosen, the amount of cash you’ll use to purchase your next flat differs accordingly.

Step 3 – Top-Up CPF Retirement Account

Before you take everything and plonk it all into your high-interest savings account, it’s the same thing, guys, some of it has got to go back to CPF too, yea?

You should be glad it’s not everything!

| Net Sale Proceeds | CPF Top-Up Requirement | Net Sale Proceeds (kept in Cash) |

|---|---|---|

| Less than $60,000 | All net sale proceeds | $0 |

| $60,000 - $160,000 | $60,000 | $0 - $100,000 |

| More than $160,000 | $60,000 plus | $100,000 plus |

| Further top-up to prevailing Full Retirement Sum (FRS) | Remaining after further CPF top-up |

You can choose to top-up the CPF Retirement Account for any flat owner for net sale proceeds of $160,000 and below.

If the net sale proceeds you receive at the end is more than $160,000, the further top-up will be into the flat owner with the lowest balance in their CPF Retirement Account, with the prevailing Full Retirement Sum (FRS) as the top-up limit.

As you can see, with our scenario above, you’ll be able to keep $70,000 in cash from your sale proceeds after topping up $60,000 to your CPF Retirement Account.

Step 4 – Receive Cash Bonus

Here comes the free lunch part!

Your household’s SHB cash bonus depends on your net sale proceeds and the amount you’ve topped up to your CPF Retirement Account.

| Net Sale Proceeds | Cash Bonus |

|---|---|

| Less than $60,000 | $1 for every $3 top-up |

| $60,000 - $160,000 | $20,000 |

| More than $160,000 | $20,000 |

The example that we gave definitely doesn’t cover all the possible scenarios available, so there’s a chance that you may be getting more out of your SHB.

Some things may be out of your control, but if your net sale proceeds are going to be lesser than $60,000, then SHB might not be that beneficial for you. You won’t be able to receive any of your proceeds in cash and you’ll also be receiving a prorated SHB Cash Bonus.

Step 5 – Purchase CPF LIFE Payouts

Even though it currently isn’t explicitly stated on HDB’s SHB website that you are required to purchase a CPF LIFE plan after SHB, it is addressed in their FAQ that all monies in your Retirement Account will be used to buy a CPF LIFE plan.

Especially since the idea of SHB is to enhance your retirement income, make sense, right?

Depending on your age and balance in your Retirement Account after everything is settled, the scenario will be slightly different.

| Age | Current Scheme you are Eligible for When Applying for SHB | What Happens? |

|---|---|---|

| Below age of 80 | CPF Life | Top-up to Retirement Account under SHB will be used to buy an additional CPF Life policy |

| CPF Retirement Sum Scheme | Less than $60,000 in Retirement Account nearer your payout eligibility age: Remain on CPF Retirement Sum Scheme with higher payouts |

|

| Remaining Balance & Top-up to Retirement Account under SHB more than $60,000: Join CPF Life |

||

| Age 80 & above | CPF Life or CPF Retirement Sum Scheme | Top-up to Retirement Account will be streamed out as an additional monthly payout |

So yay, if your parents are the ones applying for SHB, they’ll have a smaller house to take care of, which is a good thing.

Plus, they are more likely to unlock a CPF LIFE plan to help take care of their retirement expenses!

What Do I Need To Take Note Of?

Besides looking at the eligibility conditions and estimating the total cash you might receive, you might also want to take into consideration the following.

Lease Buyback Scheme

If your household previously applied for Lease Buyback Scheme (LBS), since you won’t be able to sell your flat, you will not be eligible for SHB.

However, if you decide to apply for LBS years after, just note that you won’t be eligible for the LBS Cash Bonus, so plan well!

What If I Want To Move In With My Children Instead?

Mmhmm, we get it, some of us might want to live with our children instead of buying another flat.

But if you’re doing so, or have other living arrangements, you won’t be eligible for SHB as they want to ensure that your basic need, housing, is taken care of.

Furthermore, if you’re not buying another flat, well, you’ll probably have quite a substantial sum from the sale of your property!

Can I Use My Savings To Top Up My Net Sale Proceeds?

Whether you have zero net sale proceeds or it’s lower than $60,000, you won’t be able to use your personal savings to top up the difference.

With zero net sale proceeds, you won’t be able to make any eligible top-ups and hence, you won’t be able to receive the SHB.

Even though I don’t have my own flat yet, I’m dreading the idea of cleaning a 4-room or 5-room flat after a long week of work…

Yea, that’s nothing compared to not having enough for our retirement, but hey, it’s still a valid concern!

The Silver Housing Bonus Scheme may be useful for the retirement portfolio for yourself or your loved ones, but at the end of the day, it really depends on the current situation.

Not sure whether the Silver Housing Bonus Scheme or the Lease Buyback Scheme works better for you? Don’t be shy, you can ask our friendly community! !

Advertisement