We are living in extraordinary times.

As the world reels from the impact of COVID-19, central banks around the world have been cutting their benchmark rates after the U.S. Federal Reserve cut interest rates to near-zero.

The Fed also recently announced that they will keep interest rates near zero until 2023.

As such, local banks like UOB have had to make changes to the interest rates for their savings accounts.

The new round of changes will take effect from 1 November 2020.

This will be the third time UOB is cutting interest rates on its UOB One Account in Singapore this year.

In addition, UOB will also be cutting the interest rates for another one of its savings account, the UOB Stash Account.

For existing UOB account holders and those looking to open up a UOB One account; should you still be using this account after the changes or look elsewhere?

Here’s what you need to know

TL;DR: UOB One Account + UOB Stash Account Updated Interest Rates

We’ll break it down by the Ugly, the Bad and the Good.

- The Ugly: UOB Cutting Interest Rates for its UOB One Account

- The Bad: UOB Cutting Interest Rates for its UOB Stash Account

- The Good: Qualifying Criteria for the UOB Account and UOB Stash Account Remains Unchanged and Simple

Earning Interest Rates with the UOB One Account

| Account Balance in your UOB One Account (SGD) | Category A: Credit Card Spend | Category B: Credit Card Spend + Credit Salary OR 3 GIRO debit transactions |

|---|---|---|

| First $15,000 | 0.25% | 0.50% |

| $15,001 - $30,000 | 0.25% | 0.55% |

| $30,001 - $45,000 | 0.25% | 0.65% |

| $45,001 - $60,000 | 0.25% | 0.80% |

| $60,001 - $75,000 | 0.25% | 2.50% |

| $75,001 and Above | 0.05% | 0.05% |

In case you’re new to the UOB One Account, there are 2 categories you can fulfil to earn the bonus interest rates for your UOB One savings account.

- Category A: Minimum $500 spending requirement on a UOB card each calendar month.

- Category B: Meet the minimum $500 card spend per calendar month + Salary Crediting OR 3 Bill Payments via GIRO

- Note: the Base Interest for UOB One is 0.05% p.a if you do not fulfil any of the categories.

How do you qualify for Category A?

Action 1: Spend a minimum of $500 on a UOB card each calendar month.

By simply hitting the monthly card spend requirement will get you to Category A’s extra 0.25% p.a.

This spend consists of all Visa and/or Mastercard® transactions successfully posted in the calendar month which includes:

- All Visa and/or Mastercard retail spend on your card.

- Recurring payments which cover your insurance premiums charged to your card.

Selected Debit and Credit Cards include:

- UOB One Card

- UOB Lady’s Card

- UOB YOLO

- UOB One Debit Mastercard

- UOB One Debit Visa Card

- Mighty FX Debit Card

And one of the best credit cards to complement this savings account would be its namesake – the UOB One Card.

This is a crowd favourite cashback card due to its exclusive cash rebates for merchants like Cold Storage, Giant, Grab, and Singapore Power.

How to Qualify for Category B?

To qualify for category B, you will need to fulfil Action 1, AND either Action 2 or Action 3.

Action 2: Make a Minimum $2,000 Salary Credit via GIRO to Your UOB One Account

What constitutes as Salary Crediting?

- Only valid for salary credited through GIRO with the transaction reference “SALA”

- Bonus interest is paid on the Monthly Average Balance at month-end

Action 3: Make 3 GIRO Debit Transactions Monthly From Your UOB One Account

What constitutes as GIRO debit transactions?

- Bill payments via GIRO – You need to make 3 GIRO debit transactions payable to any billing organisation with the bank, within the calendar month

- Bonus interest is paid on the Monthly Average Balance at month-end

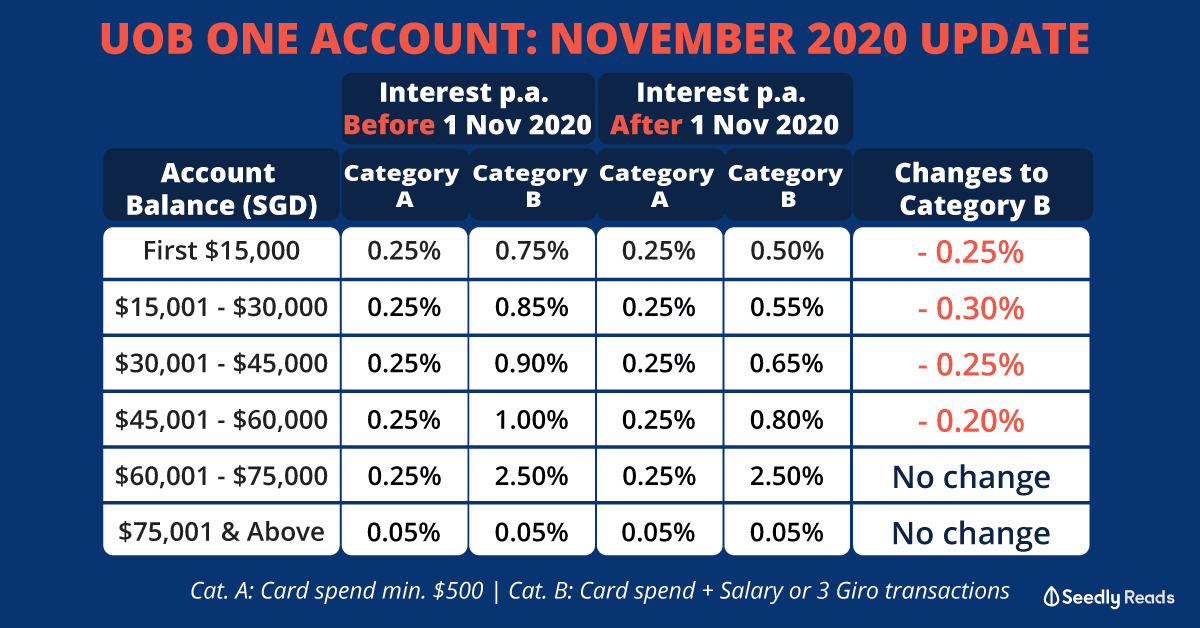

The Ugly: UOB One Account Reduction of Interest Rates From 1 November 2020

UOB has announced that they will revise the interest rates on the UOB One Account.

These changes will take place from 1 November 2020 onwards.

This revision will be applicable to all new and existing UOB One accounts.

UOB One Account Revised Interest Rates from 1 November 2020

| Account Balance in your UOB One Account (SGD) | Spend Min. S$500 (Calendar Month) on Eligible UOB Card Total interest | Spend Min. S$500 (Calendar Month) on Eligible UOB Card AND Credit Your Salary OR Make 3 Giro Debit Transactions Total Interest |

|---|---|---|

| First $15,000 | 0.25% p.a. | 0.50% p.a. |

| $15,001 - $30,000 | 0.25% p.a. | 0.55% p.a. |

| $30,001 - $45,000 | 0.25% p.a. | 0.65% p.a. |

| $45,001 - $60,000 | 0.25% p.a. | 0.80% p.a. |

| $60,001 - $75,000 | 0.25% p.a. | 2.50% p.a. |

| $75,001 - $100,000 | 0.05% p.a. | 0.05% p.a. |

The reduction in interest rates for the UOB One Account is pretty thorough.

The category A interest rates remain unchanged.

Almost all the category B interest rates have fallen with a range of –0.30% to –0.25%.

The biggest drop is for those who have between $15,001 – $30,000 in their account balance; with interest rates being cut -0.30%.

However, for those who have anything above $60,001 and above in your UOB One account, take heart. The interest rates remain unchanged.

The drop is not as drastic as the August changes, but the final interest rates are quite low.

The Bad: UOB One Stash Account Reduction of Interest Rates From 1 November 2020

| Account Monthly Average Balance | Interest Rate (p.a.) Before 1 November 2020 | Account Monthly Average Balance | Interest Rate (p.a.) After 1 November 2020 |

||||

|---|---|---|---|---|---|---|---|

| Base Interest Rate | Bonus Interest Rate | Total Interest | Base Interest Rate | Bonus Interest Rate | Total Interest | ||

| First $10,000 | 0.05% | 0.00% | 0.05% | First $10,000 | 0.05% | 0.00% | 0.05% |

| Next $40,000 | 0.05% | 0.75% | 0.80% | Next $30,000 | 0.05% | 0.25% | 0.30% |

| Next $50,000 | 0.05% | 0.95% | 1.00% | Next $30,000 | 0.05% | 0.55% | 0.60% |

| Above $100,000 | 0.05% | 0.00% | 0.05% | Next $30,000 | 0.05% | 0.95% | 1.00% |

| - | Above $100,000 | 0.05% | 0.00% | 0.05% | |||

For the UOB Stash Account, there will be a reduction in interest rates across the board.

The biggest change is the addition of another tier for the account monthly average balance across the board.

This will make it harder for you to earn more interest as previously, you only needed $10,001 to earn 0.80% interest. Now with the same amount, you are only getting 0.30%.

The Good: Qualifying Criteria for the UOB Account and UOB Stash Account Remains Unchanged and Simple

Good news.

All existing qualifying criteria for the UOB One savings account remains unchanged.

You can continue to meet the monthly eligible card spend with your UOB One card or a wide range of cards every month.

Although salary crediting remains an efficient way to raise the interest rates for your UOB One Account, it might work for people like freelancers and self-employed individuals.

Thankfully, UOB allows you the flexibility to fulfil Action 3 and qualify for category B by making 3 GIRO debit transactions each month.

This makes it still a great option for self-employed persons who do not have a regular salary.

As for the UOB Stash Account, the qualifying criteria remains the same. You simply have to maintain or increase your Monthly Average Balance to qualify for interest.

Is it Still Worth Opening a UOB One Account After 1 November 2020?

With UOB taking the lead to reduce interest rates across the board yet again, we expect the other banks to follow suit. It’s best to adopt a wait and see approach.

This does not detract from the value of this account as it is still relatively simple to perform the two UOB One Account actions to qualify for category B.

Spending $500 a month on UOB cards is not unachievable, but you should also look at our credit card reviews to see if you can get a better rate.

UOB also offers flexibility for those who cannot perform the salary crediting action with their 3 GIRO transactions action.

Alternatively, you can check out our comparison of cash management accounts in Singapore — a reasonable option with good interest rates and high liquidity.

Do note that for these accounts, there is no capital guarantee as they are investments.

Stay safe everyone!

Advertisement