Have you purchased insurance before?

I made my first insurance purchase when I was 19 years old – a Personal Accident plan.

Why did I do it?

Honestly, my memory’s quite fuzzy, but I think I did it because a “friend” wanted to have coffee with me.

But I never would’ve thought that the purchase was a good decision until I fell into the drain on a rainy day soon after, and I made successful claims for the accident.

Just recently, the topic of insurance came up during one of my gatherings and I realised, most people don’t know what they don’t know about insurance, and hence did not purchase any!

Yes, it’s as simple as that.

So, to help you break down some concepts, I’ll be doing some age profiling to help you understand exactly what you might need in your current life stage.

TL;DR: Insurance Policies You Need At Every Life Stage

Click here to jump:

- Reasons For Buying Insurance

- How much insurance coverage do you need in Singapore?

- What are the most important insurances to have in Singapore?

Disclaimer: Do note that the information provided by Seedly serves as an educational piece and does not constitute an offer or solicitation to buy or sell any investment product(s). It does not consider the specific investment objectives, financial situation, or particular needs of any person. Readers should always do their own due diligence and consider their financial goals before investing in any investment product(s). For definitions of various insurance terms, please refer to lia.org.sg.

Why Do People Buy Insurance?

You see, insurance is a touchy topic.

Stories of agents who ignored your texts after closing your deals are not unheard of.

I like to think that insurance policies should complement each other, but there is no one-size-fits-all matrix, and for some, ‘the more the better’.

For the insurance newbies, these are insurance policies you can find in Singapore:

| Insurance Policies | |

|---|---|

| Careshield | Launched in 2020, it provides financial support to those with severe disabilities. This is a national long-term care insurance scheme that automatically covers everyone between 30 and 40 years of age. Thereafter, future cohorts will join at the age of 30. For these, CareShield Life replaces “ElderShield”. Pays at least $600 a month for as long as care is needed. People above 40 in 2020 can choose to stay with ElderShield or switch to CareShield Life. |

| CPF Dependants Protection Scheme | The Dependants Protection Scheme covers eligible CPF members up to 60 years old for up to a maximum of $70,000. For members above age 60 and up to age 65, DPS covers them up to a maximum sum assured of $55,000. DPS is currently solely administered by Great EastePays insured CPF members or their families should the insured suffer from Terminal Illness or Total Permanent Disability, or pass away. |

| CPF Life | The CPF Lifelong Income For The Elderly (CPF LIFE) Scheme is a life annuity scheme that provides Singapore Citizens and Permanent Residents with lifelong monthly payouts. There are three CPF LIFE plans for you to choose from – the LIFE Standard Plan, the LIFE Basic Plan, and the LIFE Escalating Plan. |

| Critical Illness Insurance | Major illnesses and types of surgery usually covered include major cancers, heart attack of specified severity, coronary artery bypass surgery, stroke and kidney failure. Each critical illness or surgery is precisely defined in the policy. Pays you only if your condition or surgery meets the stated definition. The amount paid may be different, depending on the various stages of a critical illness. A waiting period, typically 90 days from start date of coverage, usually applies to certain illnesses or types of surgery, for example, major cancers, heart attack of specified severity and coronary artery bypass surgery. If any such illness is diagnosed or surgery is carried out during the waiting period, nothing is payable from the policy. |

| Direct Purchase Insurance | Direct Purchase Insurance (DPI) is a class of broadly standardised products offering term insurance or whole life insurance, and which include Total and Permanent Disability (TPD) coverage. Also provides Critical Illness (CI) coverage if you opt for it. DPI is identified by the prefix “DIRECT” in the product name. Buy from the customer service centre, or website if available, of life insurance companies. Sold without financial advice. |

| Disability Income Insurance | To ease your financial burden, it pays a fixed amount each month to replace part of the income you would lose if you are not able to work as a result of an accident or illness. Some policies define disability as not being able to perform your usual work, while others define it as not being able to do any work at all. There may be a deferment period of time during which nothing is payable from the policy. Payment usually starts after you have been continuously disabled for longer than the deferment period. Payment stops once you are able to work again or it may be reduced in proportion to the recovery you are making. |

| Eldershield | Long-term care insurance scheme that provides financial support to those with severe disability. Depending on the plan, ElderShield pays $300 a month for up to 60 months or $400 a month for up to 72 months to help cover caregiving expenses. ElderShield Supplements - ElderShield insurers also offer optional additional coverage with extra premiums. People above 40 in 2020 can choose to stay with ElderShield or switch to CareShield Life. |

| Endowment Policy | Covers you for a set period of time. Provides a combination of protection and savings. Pays the sum insured and any bonuses built up at the end of the set period of time (the maturity date), or when you die or become “Totally and Permanently Disabled” if TPD benefit is provided during this period. |

| Integrated Shield Plans | Integrated Shield Plans (IPs) provide higher coverage than MediShield Life. IPs comprise two parts - the basic MediShield Life, and an additional private insurance portion run by private insurers, typically to cover Class A/ B1 wards in public hospitals or wards in private hospitals. No duplication of coverage or premiums between IP and MediShield Life. |

| Investment-Linked Insurance | Provides a flexible combination of death coverage (protection) and investment. You decide on the level of death benefit you want. Premiums are used to buy insurance protection and investment units in a managed fund. Depending on your risk appetite, you invest your premiums in the funds of your choice. The price of your investment units depends on how the funds perform. What the policy pays depends on the price of the units at the time of death or when you cash it in. |

| Long-term Care Insurance | Pays a fixed amount each month when you are unable to perform “activities of daily living” (ADLs) such as bathing, dressing, feeding, going to the toilet and moving around. Definitions of ADLs and the minimum number of activities you must not be able to perform to qualify for payment vary from one policy to another. Payment stops if the number of activities you cannot perform falls below the minimum stated in the policy. Some policies pay for up to a set number of years. Other policies pay for life as long as you meet the qualifying conditions. There may be a waiting period of time during which nothing is payable from the policy. Payment usually starts after you have not been able to perform the minimum number of ADLs for at least a set period of time. |

| Medical Expense Insurance | Reimburses medical costs incurred as a result of an accident or illness. Medical expense insurance will not pay you more than the actual medical expenses incurred, regardless of the number of such policies you have. Pays for inpatient medical treatment or surgery, some outpatient charges for day surgery, consultation with specialists before and after your hospital stay, and X-rays and laboratory tests. May have limits on the amount you can claim. Major medical expense insurance pays for longer hospital stays due to a major illness or major surgery such as heart bypass surgery or organ transplant. |

| Medisave | National savings scheme to help CPF members save for medical expenses, especially for retirement years. You contribute a part of your monthly salary to your MediSave Account. If you earn yearly Net Trade Income (NTI) of more than $6,000 as a Self-Employed Person, you will also need to contribute to MediSave. |

| Medishield Life | National basic healthcare insurance scheme run by the Central Provident Fund Board. MediShield Life replaced MediShield from 1 November 2015, and covers all Singapore Citizens and Permanent Residents for life. Pays for bills of Class B2/ C wards and certain outpatient treatments such as kidney dialysis and chemotherapy for cancer in public hospitals. Pays for bills of Class A/ B1/ B2+ wards in public hospitals or wards in private hospitals, as sized to the equivalent Class B2/C bills and then subject to MediShield Life claim limits. |

| Term insurance | Covers you for a set period of time. Typically, no “cash value” is payable if you decide to terminate the policy. Pays the sum insured when you die or become “Totally and Permanently Disabled” if TPD benefit is provided. |

| Universal Life Insurance | Universal life is a form of 'interest sensitive' life insurance that offers a death benefit and provides the opportunity to build cash values which you can withdraw or, in some instances, borrow from. The cash value earns interest at a declared rate, which may change over time. Notwithstanding that, most universal life plans guarantee a minimum interest crediting rate. Two distinct types of universal life plans: • Protection-oriented universal life plans that provide high insurance coverage, these are typically whole of life plans; or • Savings-oriented universal life plans that provide low insurance cover, and focus on wealth accumulation. These could be for whole of life or for a limited term. Renewability, if applicable, may not be guaranteed Gives you flexibility to support your financial goals over time by varying the amount, method and timing of premium payments. |

| Unit Trust | A financial product where money from investors is pooled together and invested collectively in investments such as shares and bonds. Also called Collective Investment Scheme (CIS). |

| Whole Life Insurance | Covers you for your lifetime. Also provides long-term savings, as the insurance company invests on your behalf. Pays a “cash value” if you decide to terminate the policy. Pays the sum insured and any bonuses built up when you die or become “Totally and Permanently Disabled” if TPD benefit is provided. You pay premiums throughout your life, but this can be changed to a limited payment period. |

Overinsured Vs Underinsured

Suffice it to say, most people don’t really know what being “over-insured” and “under-insured” means.

I’ve recently come across someone who holds five whole-life insurance policies and is spending at least $1,200 per month just on these policies!

For the uninitiated, being overinsured means you’ve overbought insurance plans which might potentially leave you struggling financially or paying more than what you might need and as a result, “overpaying” some premiums.

On the flip side, being underinsured means there are gaps in your insurance coverage which could leave you vulnerable to financial risks and uncertainties.

So, the next question you’ll ask is…

How Much Insurance Coverage Do You Need?

The general rule of thumb is to assess based on your current circumstance.

Are you a student? A first jobber? A mid-career switcher? A new parent?

What’s your occupation and is there a physical risk imposed? Do you have a family history of cancer?

It all boils down to risks and liabilities.

On a relatable note, most buyers are also perturbed by the “Sum Assured” because they aren’t sure how much they really need if something were to happen.

To evaluate your “Sum Assured”, here are some recommended coverage:

If someone tries to upsell you insurance with an expensive premium, especially a life insurance policy when you already have one, consider these:

- Are you sufficiently covered for your current one?

- What is the purpose of having another one?

- Will you be financially strapped?

- Could the money used for this extra policy be better used in other areas e.g. low-risk investments such as Singapore Savings Bonds?

Again, I’m not downplaying what you need, but let’s just say it’s easy to be convinced because of the uncertainties.

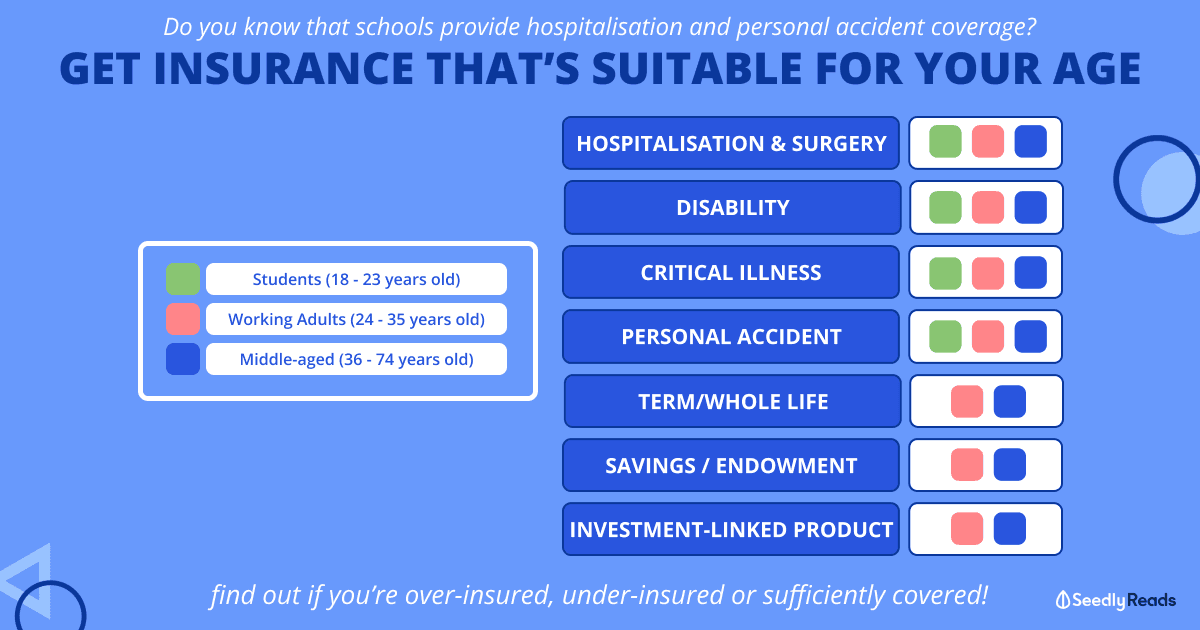

What Insurance Should You Be Getting?

18 – 23 Years Old: What Insurance Should Students Get?

I’m not sure if you’re aware, but most schools in Singapore do offer Group Personal Accident (GPA) and Hospitalisation & Surgical insurance that covers specialist visits.

In fact, since 2018, the Ministry of Education has rolled out the GPA for students in primary school, secondary school, and junior college, led by the Income Insurance Co-operative Limited.

Generally, the insurance covers death, permanent and total/partial disability, and medical due to:

- Accidents happen in school

- Participation in school activities;

- Commuting from (or to) her place of residence, to or from the school’s premises or the place where an activity covered by the GPA Insurance is conducted;

- In the student care center located in her school;

- Participating in any activity conducted by the above-mentioned student care center.

Universities in Singapore also provide such insurance with standard consultations and medications at university health centers charged for free.

Of course, most of the coverage is either directly related to school or on-campus incidents.

If you’re prone to accidents out of school compounds, chances are you should be getting a personal accident plan just like me.

There are tons of affordable plans out there with attractive promotions.

Similarly, if you’re getting a personal accident plan, you can complement it with a Hospitalisation & Surgery plan if it’s deemed necessary.

Again, you need to ask yourself if your risk exposure is low or high.

If you’re already covered in school, do you really need a separate plan?

24 – 35 Years Old: What Insurance Should Young Working Adults Get?

When you fall into this age range, you’re out of school and more or less getting started with better insurance coverage as life’s responsibilities pile up.

For those who’re becoming new parents, you might want to consider getting life insurance if you haven’t.

Everyone has different needs and getting life or term insurance is very much tailored to a person’s needs. The lowest premiums or the ones offering the highest payouts do not necessarily mean it’s the best plan for you, so make sure you research beyond this article before buying your life insurance.

It is also at this age that we experience drastic life transitions and become more conscious about our needs.

We’ve previously covered five key insurance plans working adults should be getting.

If you noticed, hospitalisation & surgical insurance is always prioritised, and this is not without a reason.

We’re in the pink of health and probably the healthiest during this period.

While we have the Central Provident Fund administered national health insurance plan aka MediShield, it’s might be insufficient for some.

After all, healthcare is not cheap, and for illnesses that require more medical attention and expensive treatments, your MediSave account might not be sufficient to cover them.

In fact, this plan saved me quite a sum when I caught dengue and checked in at the hospital last year!

It’s also a common misconception that health insurance premiums are especially expensive with age.

In actual fact, premiums for health insurance or Integrated Shield Plans increase over time as we age, regardless of when we purchase it. The older you are, the more expensive your insurance premium will be, no matter what plans you choose.

When you’re looking at Hospitalisation & Surgery plans, don’t forget that a Critical Illness plan may also complement it.

36 – 74 Years Old: What Insurance Should Middle-Aged to Older Adults Get?

If you noticed, I didn’t split this group because the commitments between both groups often overlapped, especially when the statutory retirement and re-employment age are both increasing.

Those entering their late 30s and late 40s, this is the peak of the rising affluent who have heavier financial commitments, but also the period where you really have more means to work towards achieving financial freedom.

Also, this is the age when most people start picking up caregiving duties.

This means that if you want to purchase a policy for your older parents, you need to do it before they turn 75, as most insurance policies have this maximum entry age that you should pay attention to.

Besides investing, you also have to consider putting aside savings and emergency funds if you have dependents.

To avoid depleting your savings when you meet a mishap that may lead to a potential loss of income, consider insuring yourself early with long-term care insurance plans to get a payout, such as the CareShield Life supplementary plan, which can be paid using MediSave.

Needless to say, when you have kids, getting a savings mix insurance plan such as an Endowment plan is a way to save for your child’s education, your retirement, or some other fixed milestone.

With emerging short-term endowment plans such as the Great SP Series 9 or Tiq 3-Year Endowment Plan, instead of taking a decade or more to reach maturity, these plans mature in just two to six years.

You might’ve also heard of Investment-Linked Insurance which provides a flexible combination of death coverage protection and investment. First things first, for every investment-centric product, there is a level of risk involved.

Before jumping on it, ask around for reviews and read the terms and conditions carefully to ensure that there’s some form of flexibility that you can make use of if you need the money urgently.

When to Review Your Insurance Plans?

Ideally, you should review your insurance once a year.

Take this as a checkpoint to assess your current situation and what may happen over the rest of the year!

Related Articles:

- Best Insurance Savings Plans in Singapore (2022): Dash PET vs Singlife Account vs Dash EasyEarn vs GIGANTIQ

- Freelancer Insurance Guide: So That You Get Paid Even When Sh*t Happens

- Best Home Insurance (2022): Lessons Learnt When My Wife Tried to Set Me On Fire

- Best Credit Cards for Insurance Premiums in Singapore 2022

- The Best Car Insurance Guide in Singapore: Promotions, Comparisons Etc.

Advertisement