Banking on Diversification: Why You Should Have Multiple Bank Accounts

Seedly

Seedly●

Bank accounts are the bedrock of our financial lives.

It is where we keep most of our life savings, make transactions and track our money. Most of us assume that just having one bank account would suffice.

But if you have ever wondered, “is it better to have multiple bank accounts?” or “should I open multiple bank accounts?”, the answer is: it depends on how you use your money.

As someone who prefers simplicity, I understand the appeal of keeping everything in one place. However, as your savings grow and your financial life gets more complex, having multiple bank accounts can give you better protection, more flexibility and a cleaner way to manage your money.

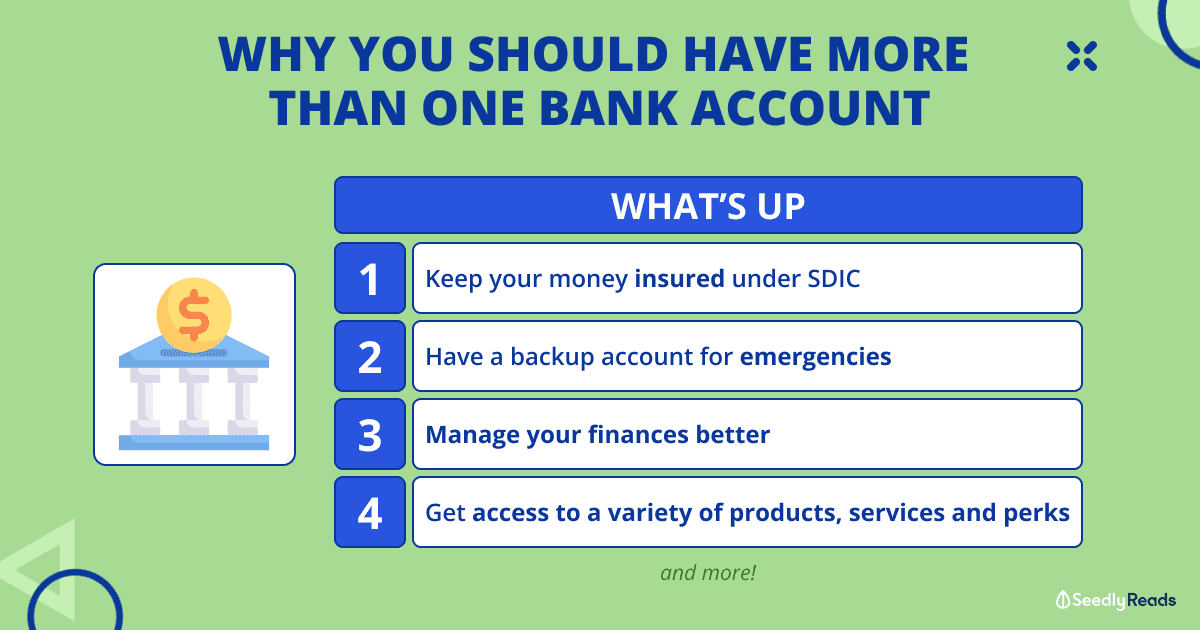

So, here’s why you should have more than one bank account!

TL;DR: Why You Should Have More Than One Bank Account

Jump to:

- Keep Your Money Insured Under SDIC

- Ensure Seamless Transactions and Payments

- Manage Your Finances Better

- Get Access to a Variety of Financial Products, Services, and Perks

- Things to Look Out For When Choosing Bank Accounts

- How Many Bank Accounts Should I Have?

1. Keep Your Money Insured Under SDIC

One key reason to have more than one bank account is deposit insurance.

In Singapore, eligible Singapore-dollar deposits with a full bank or finance company that is a member of the Deposit Insurance Scheme are insured by the Singapore Deposit Insurance Corporation, or SDIC.

The current SDIC coverage limit is up to S$100,000 per depositor per Scheme member. This means that if you have multiple accounts with the same bank, your eligible insured deposits with that bank are aggregated and covered up to S$100,000. However, eligible deposits held with different Scheme-member banks are covered separately, up to S$100,000 per bank.

This is where multiple accounts can be useful.

For example, if you keep more than S$100,000 of eligible Singapore-dollar deposits in one bank, the amount above the insured limit may not be covered by SDIC. In that case, you may want to place the excess cash with another SDIC Scheme-member bank so that more of your money sits within the insured limits.

Of course, Singapore’s banking system is generally regarded as sound and resilient. MAS has also stated that Singapore banks remain well-capitalised and liquid. Still, the point of insurance is not to predict disasters. It is to manage risk before you need it.

The collapse of Silicon Valley Bank and the takeover of Credit Suisse in 2023 were reminders that even established names can face stress. For SVB specifically, US authorities made all depositors whole, but the standard FDIC deposit insurance limit remains at least US$250,000 per depositor, per FDIC-insured bank.

So yes, having more than one bank account can be a practical way to diversify where your cash is held.

2. Ensure Seamless Transactions and Payments

Another reason to keep more than one account is simple: outages can happen.

Back in 2023, DBS experienced major disruptions to its digital banking services, including a disruption on 29 March 2023 and another disruption involving digital banking and ATM services on 5 May 2023.

DBS remains Singapore’s largest bank, and it also provides one of the widest self-service banking networks here. But even large banks are not immune to service disruptions.

That is why it helps to have a backup bank account.

For example, you could keep your main account for salary crediting, bills and daily spending. Then, you could keep a second account with another bank that has enough cash for a few days of essential expenses.

This way, if your main banking app, card or ATM access is temporarily unavailable, you still have another way to pay for meals, transport, groceries or urgent transfers.

It is not about expecting your bank to fail. It is about making sure your day does not grind to a halt when one payment channel goes down.

3. Manage Your Finances Better

Using multiple bank accounts for budgeting can also help you separate your money by purpose.

A common approach is the 50-30-20 rule:

- 50% for needs

- 30% for wants

- 20% for savings, investing or debt repayment

Budgeting is encouraged as a way to track income, spending, savings and debt, and suggests setting aside emergency savings of around three to six months’ worth of monthly expenses.

The problem is that when all your money sits in one account, it can be hard to tell what is truly available to spend.

For example, your account balance might look healthy after payday. But that same balance may need to cover your credit card bill, insurance premium, mortgage, investment transfer and upcoming holiday expenses.

This is where separate accounts can make life easier.

You could use:

- One account for salary and daily transactions

- One account for emergency savings

- One account for short-term goals, such as travel or a home renovation

- One account for investing or wealth-building transfers

By separating your money, you are less likely to accidentally spend cash that was meant for another purpose.

This also makes it easier to track progress. If your emergency fund sits in its own account, you can see at a glance whether it is growing, shrinking or sitting where it should be.

4. Get Access to a Variety of Financial Products, Services, and Perks

Not all bank accounts are built the same.

Some accounts reward salary crediting, card spending, bill payments or investing. Others are simpler savings accounts with fewer hoops, but lower potential interest. Because of this, one account may not give you the best mix of convenience, interest, tools and perks.

For example, the DBS Multiplier Account currently offers bonus interest of up to 4.10% p.a. on the first S$100,000, but the rate depends on monthly eligible transactions such as income crediting and transaction categories. If you do not meet the criteria, base interest applies.

That does not mean the account is useless. You may still value DBS for everyday banking, DBS PayLah!, PayNow transfers, QR payments and ATM access. DBS PayLah! continues to support everyday functions such as payments, transfers and bill payments.

On the other hand, you might use another savings account for cash that you do not need to touch often.

For example, Standard Chartered JumpStart is available for applicants aged 18 to 26 at account opening, and customers may continue maintaining the account after turning 26. Its base interest is currently 0.50% p.a. on the first S$50,000 and 0.10% p.a. on amounts above S$50,000. However, additional Step-Up interest requires meeting investment-related conditions, so you should not treat the highest advertised rate as automatic.

GXS Savings Account is another example. Its Main Account currently earns 0.88% p.a., Saving Pockets earn 1.08% p.a., and Boost Pockets can earn up to 1.60% p.a., depending on the tenure and maturity conditions. GXS also states that there is no minimum balance, no salary crediting and no minimum spend for its core savings account features.

The takeaway is not that you should open every account available.

Instead, think of each account as a tool. One account may be best for daily payments. Another may be better for emergency savings. A third may work better for salary crediting, investments, or credit-card-linked perks.

When used properly, multiple accounts can help you get more out of the banking system without mixing up your money.

Things to Look Out For When Choosing Bank Accounts

Before opening multiple accounts, check the details carefully.

Some accounts come with minimum balances, fall-below fees, account service fees or age requirements. For instance, bank pricing guides may list different minimum-balance and fall-below-fee rules depending on the account type. These charges can eat into your interest if you are not paying attention.

You should also check how bonus interest is earned.

Ask yourself:

- Do you need to credit your salary?

- Do you need to spend on a linked card?

- Do you need to invest or buy insurance?

- Is the advertised rate only for a limited balance?

- Is the rate automatic, or does it depend on specific actions?

Beyond interest rates, look at practical features too.

A good bank account should fit the way you actually live. That includes a reliable mobile banking app, smooth PayNow transfers, easy bill payments, card compatibility, useful ATM access and support for mobile wallets such as Google Wallet / Google Pay where relevant. Google’s support materials now refer users to Google Wallet for setup and contactless payment features, while Google Pay acceptance remains relevant at checkout.

Finally, do not open too many accounts for the sake of it.

Having multiple accounts can help, but having too many can become messy. You may forget minimum-balance requirements, miss fee changes, or lose track of where your money is parked.

A good bank account setup should make your finances clearer, not more confusing.

How Many Bank Accounts Should I Have?

If you ask me, at least three bank accounts can be a practical starting point:

- A transactions account

- A savings account

- A wealth or investing account

Your transactions account is for salary, spending, bills and transfers.

Your savings account is for emergency funds, short-term goals and cash you do not want to spend casually.

Your wealth or investing account is where you route money meant for investments, fixed deposits, robo-advisors, brokerage transfers or other wealth-building tools.

That said, this is not a hard rule.

If you are just starting out, two accounts may already be enough: one for spending and one for saving. As your savings grow, your goals become more specific, or your cash exceeds SDIC’s S$100,000 insured limit with one bank, adding another account may make sense.

So, should you open multiple bank accounts?

If you want better budgeting, more payment backup, broader access to bank features, and a smarter way to stay within deposit insurance limits, then yes, having multiple bank accounts can be worth considering.

The key is to keep it intentional.

Do not open accounts just because a bank is advertising a high rate. Open them because each account has a clear job in your financial life.

Related Articles

Advertisement