Insurance is your life’s GOALKEEPER, i.e. your last line of defence. If all else fails, you will need to count on your insurance to be there, especially for financial woes.

In fact, we frequently get this question asked and answered by our friendly Seedly community on our platform:

“What are the key insurance policies that I really need?”

Let’s dive into what insurance policies we really need.

TL;DR: Insurance Policies in Singapore You Should Get

In this article:

- Why Insurance is Important

- What Insurance Do I Need?

- Insurance Coverage Guide: Which Are The Most Important Types Of Insurance To Get?

- Frequently Asked Questions About Insurance

- Concluding Thoughts

Disclaimer: The Information provided by Seedly does not constitute an offer or solicitation to buy or sell any insurance product(s). It does not take into account the specific objectives or particular needs of any person. We strongly advise you to seek advice from a licensed insurance professional before purchasing any insurance products and/or services.

Why Insurance is Important

Basically, it protects you from three Worst Case Scenarios:

- You pass away prematurely, and your dependents (e.g. family, kids) inherit your debts and loans while losing a source of income

- You come down with a terminal illness, e.g. cancer (most common) and get hospitalised often while having to foot the bill for expensive treatment sessions

- You get into an accident and survive but face expensive hospital bills and follow-up treatment.

No Longer “Ownself Check Ownself”

When you enter the working world, your friends in financial planning or advisory sectors will likely approach you for coffee.

I urge you to take this opportunity to learn from them. However, do not buy immediately, especially if you need more time to understand the product.

Read up beforehand or after and have your doubts clarified despite their recommendations.

So how can you do this?

Simple.

Use this guide, and feel free to show it to your insurance agent as a checklist to ensure that your interests are taken care of.

Note: We do not receive commissions from any of these recommendations, so this would probably be one of the most unbiased guides in Singapore.

How Much Insurance Coverage Do You Need?

A lot of people believe that insurance is a pain in the ass.

I believe that insurance agents mis- and oversell because, more often than not, they’re just motivated to close the sale.

Of course, there are some agents and advisors who genuinely do a good job and care about your interests.

In any case, getting insurance should be as simple as getting sufficient coverage for the right reasons at the lowest cost.

Insurance Coverage Guide: Which Are The Most Important Types Of Insurance To Get?

We conducted a poll with the Seedly Community some time back to find out which are the most important types of insurance to get:

![]()

From the 200+ votes that the poll gathered, more than 185 voted for health (hospitalisation and surgery), followed by more than 80 for term life, followed by other options like critical illness, personal accident and disability.

Side note: I highly recommend checking out the Seedly community’s comments, as they provide pretty interesting insights into why these are the top options.

Frequently Asked Questions About Insurance

Here are some of the more commonly asked questions about insurance that we will answer.

Should You Get A Financial Consultant Or Do-It-Yourself (DIY)?

This is entirely up to you and which you are more comfortable with.

The same analogy follows:

- Pharmacy: If you already know what you want (e.g. buying Panadol or flu medicine), you don’t pay consultation fees

- Doctor Clinic: If you have some complicated existing plans or complications, go to the doctor and pay consultation fees on top of the medicine cost

If you are ‘sick’, you would go to a doctor you know or recommended by someone close.

But before you do anything, you should always seek the services of a professional. This means finding a financial consultant or advisor who is an expert in this area.

Talk to a few of them, find out your needs, balance the recommendations across different consultants, and decide if you want to do it yourself.

To be honest, I have tried doing it myself, but it was tedious as I wasn’t aware of the conditions of certain companies, and it can be confusing when you try to manage it all by yourself.

Differences Between The Various Types Of Insurance

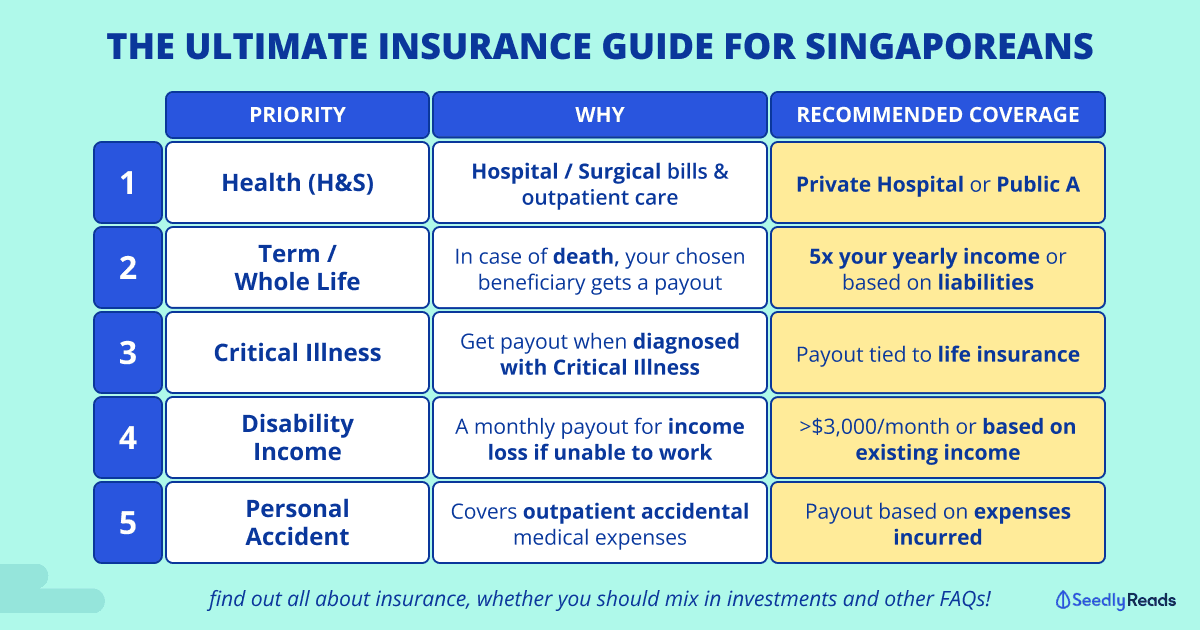

Rank 1: Health insurance (ESSENTIAL)

- What: This covers the really expensive Hospital and surgical bills and outpatient care; usually, this is an enhancement to Medishield Life, which is a government basic health plan for public hospitals up to B2 ward/service.

- Recommended Benchmark: At least public A or Private if you can afford it. The reason because I have personally seen the differences in treatment between both private and public hospitals, and it’s quite a world of difference.

- Why it’s important: MOST IMPORTANT. This is the one that usually causes the most damage financially. Because you are neither dead nor 100% healthy. It can be very painful to survive using your own cash or have less than the best care for you. One cancer chemotherapy session costs around $5,000 to $6,000, and surgery can be anywhere between $15,000 to $40,000 for a private quality standard. If you want to learn more about this, you can read my personal story here.

As one of our Seedly readers has pointed out, this insurance covers pre and post-hospitalisation charges. Lab, diagnostic and investigative tests are covered before the confirmation of a major disease.

For example, expensive PET scans and biopsy tests are claimable before one is diagnosed, say, with cancer.

Rank 2: Life insurance (ESSENTIAL)

- Term Life: This is a purely coverage-focused product, where all your monthly/yearly premiums go into coverage, so at the end of the term (usually 65 years old), you are no longer covered. This also means there is no cash component and is what most savvy people recommend because they know how to use the excess cash saved to invest for better returns

- Whole Life: This is a mix of coverage product with a savings component tied to it. There is a cash value associated with your policy

- Investment-Linked Product (ILP): This is a variant of the life policy where they mix the investment component into coverage. Often with a long lock-in period before seeing returns

- What: In case of death, your family gets paid the total sum assured

- Recommended Benchmark: 5X your yearly income OR your existing liabilities (this is one of many benchmarks available to the public)

- Why it’s important: Should increase when you have dependents or more liabilities (e.g. loan, kids)

Rank 3: Critical Illness (ESSENTIAL)

- What: Usually designed as a rider (a fancy word for a top-up on your life policy), You get paid out a sum assured for a list of 37 critical illnesses when discovered by doctors

- Recommended Benchmark: Varies from policies, and the payout is tied to life insurance

- Why it’s important: Good to have because the likelihood of cancer is 1 in 3 people. You can opt for also the early critical illness, where you get paid out for earlier discovery to seek treatment (e.g. stage 1 & 2)

Rank 4: Disability (ESSENTIAL)

- What: A monthly payout for income loss if unable to work

- Recommended Benchmark: >$3,000/month payout to match your salary

- Why it’s important: Crucial if you are the sole breadwinner or entrepreneur, and when you go down, at least there is a constant stream of income coming in for day-to-day expenses

Rank 5: Personal Accident (ESSENTIAL)

- What: Cover outpatient accidental medical expenses

- Recommended Benchmark: Payout based on accident expenses (e.g. MRI, CT scan where you are not serious enough to get warded)

- Why it’s important: Generally, at quite an affordable price, you feel assured that if you sprain your leg or break an arm playing sports or activities, you can claim for the expenses (Also, food poisoning, insect bites etc.) Also, check with your company; they should usually have a group cover plan for such personal accident insurance.

Should You Mix Investment And Insurance?

A question that normally follows is: If my agent is selling me an Investment-Linked Product, is he/she trying to milk me?

I would think that he/she thinks you are lazy (and do not have time nor interest to make your own investments).

There is a saying that you would rather focus on a better tool for each purpose rather than a jack-of-all-trades.

By mixing both together, you are buying one product for multiple purposes (investing and insurance ), which may lead to a ton of middlemen: which in turn, drives up management fees, costs etc.

By keeping the investment component separate, here are the major positives:

- You are in control of your own finances (knowing what is happening etc.)

- You pay way fewer fees to more middlemen transacting the deals (management fees and costs)

- You have more flexibility to withdraw or reallocate the funds with way fewer fees (low or no lock-in)

However, that being said, the path to learning to self-invest requires a lot more patience in learning, hard work and also risk appetite, which most people may not be entirely committed to. So it’s really up to you if you are willing to commit the time and effort to do this.

You Bought An ILP From An Agent, Should You Surrender It?

You can read 21 different answers and perspectives on surrendering your ILP or endowment and things to consider.

- What was your intention when getting the policy? Is the policy still on its way to helping you meet that objective?

- Can you invest at a lower cost?

- Are you able to invest on your own and fetch a higher return?

- Are you well-covered, or do you have plans to get insurance coverage after cancelling your ILP?

- Does it make sense to carry on with the ILP in terms of cost and functionality?

” In short, if you are disciplined and know enough to do better financially and in terms of coverage, go ahead and cancel that policy! If not, stick to it.”

A definition: In ILPs, premiums are used to pay for units in investment-linked sub-fund(s) of your choice. Some of the units you bought are then sold to pay for insurance and other charges, while the rest remain invested.

- Very often, ILPs incur not only costs but it becomes rather tricky at a later stage in life. You can head over to this post here in our Community, where some users discussed the realities of the rising cost of insurance in the ILP eating up the investment value at a later stage.

- Also, you can refer to this user’s blog where he/she labelled it NEVER EVER BUY AN ILP. In summary, he/she only had a return of 0.35%, which is way below inflation at 5.1% in October.

- One of our community contributors, Alan, discussed the interesting trend of underinsuring. This is because they mix insurance with investment (aka whole life), endowments and ILPs. These investment products give mediocre insurance coverage.

- Hence, some agents may jump on this on this to sell policies which may be without sufficient coverage.

Fun fact: ILPs became popular in the 2000s when the term insurance was not sexy enough. Agencies hence rebranded it to include investment components with coverage… there you go. ILP! Its intention was to target lazy people who didn’t want to look at growing their own money in their own ways (but most likely, if you are reading this, you should already be quite savvy, so kudos to you.)

Should You Buy All From One Agency Or Pick And Choose From Various?

Agencies usually focus on and specialise in different policy verticals. Hence, it may or may not be the best price point for various types of policies.

- However, get the ESSENTIAL (e.g. a whole life or term life with Agency X). Your RIDER (e.g. Critical Illness or Health) may be cheaper as a top-up versus individually purchasing the different plans from different agencies.

- Lastly, there is a big plus if you stick to one agency – Your Agent (point of contact). That being said, personally, my family has seen a ton of agents leave the industry just after 5-10 years (innately, these people are very driven to succeed, so being an agent may not be a long-term career path).

- Next, you get assigned another agent who may not do follow-up meetings and reviews as you have fallen off the ‘sales funnel’ in some sense.

Disclaimer: There are, of course, many agents who stay on the scene for a long time. Kudos to them on that!

Is Your CPF Insurance Coverage Enough?

Introducing the DPS (Dependent Protection Scheme) and MediShield Life.

To be extremely clear on this, these 2 auto opt-in CPF policies act as insurance protection for you:

- Dependant Protection Scheme: The Dependants’ Protection Scheme (DPS) is term insurance that provides insured members and their families with some money to get through the first few years should the insured members pass away or suffer from Terminal Illness or Total Permanent Disability. It covers only a $46,000 sum assured but for a very low premium amount yearly, between $36 to $260.

- MediShield Life: It is a basic health insurance plan administered by the Central Provident Fund (CPF) Board, which helps to pay for large hospital bills and selected costly outpatient treatments, such as dialysis and chemotherapy for cancer. It is structured so that patients pay less MediSave/cash for large hospital bills.

- ElderShield: ElderShield is a severe disability insurance scheme that provides basic financial protection to those who cannot do simple daily activities and need long-term care, especially in their old age. (you must not be able to do some of the basic routines, e.g. walking, bathing, eating, etc.)

- CareShield Life: ElderShield has been succeeded by CareShield Life and supplements.

This one below is slightly different; it acts as forced savings (via CPF) for only healthcare usage:

- MediSave: It is a national medical savings scheme that helps CPF members put aside part of their income into their MediSave Accounts to meet their future personal or approved dependent’s hospitalisation, day surgery, and certain outpatient expenses.

- This is a sum of money (which you are forced to save every month) that you can use when you are warded in public or private hospitals

The question of whether it is enough, it would depend on your expectations and personal situation.

I would say, personally, I do not think that it is enough. Hence, I’m sharing my own insurance coverage:

- Health: Upgraded to Private Hospital level (NTUC INCOME, bought at a young age) with as-charged rider

- Term + Whole Life: Coverage up to $500,000 presently (AVIVA MINDEF Scheme) with a whole life (bought at a young age)

- Critical Illness and Early CI: Riders on top of the AVIVA MINDEF Scheme

- Personal Accident: Currently, with my company policy

Concluding Thoughts

The next time your friends (in the financial advice and planning industries) ask you out for coffee, just show them the table and use it as a guide for your discussion.

If he or she starts asking you to look at investment components to mix into coverage, you should ask for the reasons behind that recommendation.

In fact, if you are reading this now, it shows that you are already considering a DIY approach to managing your own money.

It’s really not that hard, given today’s technology and the accessibility of platforms that allow you to invest independently with just a few clicks.

Starting with ETFs, for example.

Related Articles

- Best Travel Insurance With COVID-19 Medical Coverage: What To Choose For My Vaccinated Travel Lane (VTL) Getaway?

- Cheat Sheet: Best Travel Insurance Guide In Singapore 2022

- Things To Look Out For When Buying Travel Insurance

- Budget 2023 Singapore Summary

- Compare Travel Insurance in Singapore

- Best Credit Card in Singapore

Advertisement