3% Guaranteed Annual Return in 3 Years with AIA Smart G3

So… Happy 100th birthday, AIA! Last year, Great Eastern celebrated their 110th anniversary with a short-term endowment plan, this year AIA did launch a new single premium endowment plan and even RAISED THE BAR with AIA Smart G3.

Some of us might have gotten a text (maybe like so, below) from your agents, and when your insurance agent drops you a text, (sometimes) you would panic a little!

We are here to break down AIA Smart G3 for you and compare it to other products in the market.

It is important to note that AIA Smart G3 is a single premium short-term endowment plan only available for purchase with purchase, in other words, you have to purchase AIA Regular Premium plans in order to buy into AIA Smart G3.

Disclaimer: We are not sponsored to cover this product. All opinions are our own, we just want to help you!

AIA Smart G3’s Benefits At A Glance

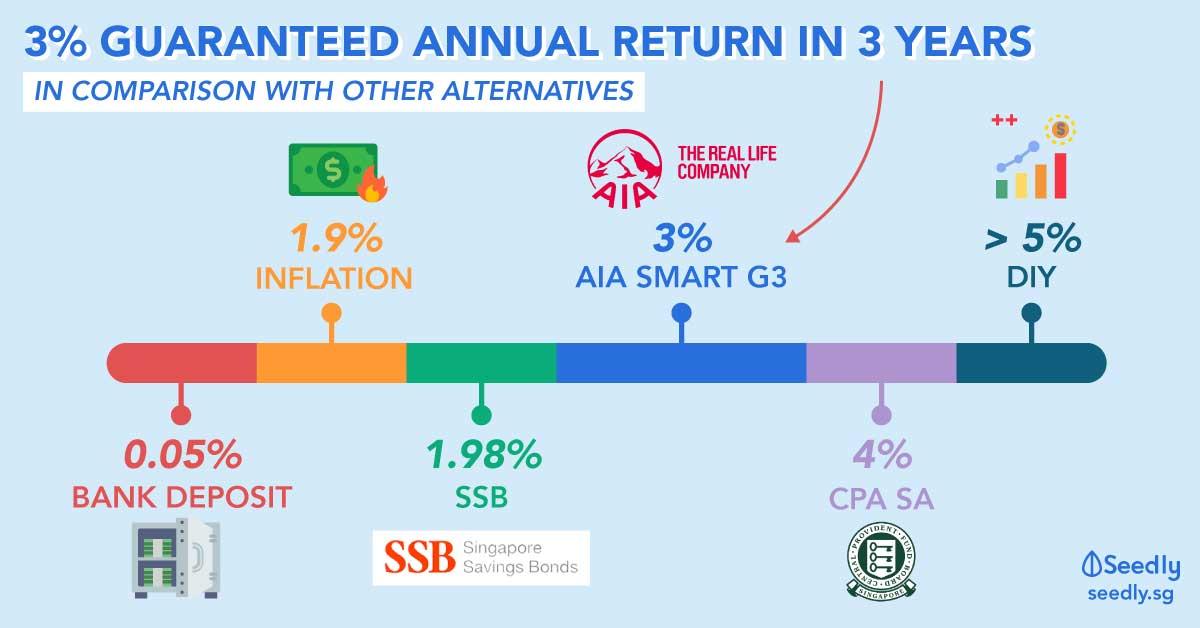

- Period: 3 years lock-in

- Guaranteed 3% per annum at maturity

- No medical underwriting required

- Death Benefit: Additional 10% payout of the insured amount

- Single Premium: Min. S$10,000

- Early termination charges

- Must be purchased WITH a Regular Savings Plan with annual premium mode only

Here’s the “perk” as extracted from their website,

“You can maximize your returns with a lump sum placement of up to 12 times the amount of the First Year Premium of the plan that you have purchased. So the better you protect yourself, the greater your returns!”

In other words, if you wish to save more with AIA Smart G3 (increase your cap/limit), you have to purchase a higher regular premium plan from AIA.

Important Note: This short-term endowment plan is only available with a purchase of a range of selected AIA Regular Premium Plans.

What do you have to purchase before being able to buy into AIA Smart G3?

| Eligible AIA Plans | Maximum Limit for AIA Smart G3 |

|---|---|

| AIA Beyond Critical Care | 12X of your first year premium |

| AIA Guaranteed Protect Plus (II) | 10X of your first year premium |

| AIA Secure Term Plus (II) | |

| AIA Platinum Term | |

| AIA Prime Secure | |

| AIA Secure Critical Cover | |

| AIA Diabetes Care | |

| AIA Triple Critical Cover | |

| AIA Premier Disability Cover | |

| AIA Prime Critical Cover | |

| AIA Pro Lifetime Protector | 3X of your first year premium |

| AIA Platinum Pro Secure | |

| AIA SmartRewards Saver (II) | |

| AIA Smart Growth (II) | |

| AIA Retirement Saver (III) | |

| AIA Wealth Pro Advantage |

Note: Maximum

More Things to Note about AIA Smart G3:

- Lump sum premium for AIA Smart G3 has to be in multiples of S$1,000

- AIA Smart G3 has to be purchased WITH a Regular Savings Plan with annual premium mode only

- There is a cap on the amount you can save with AIA Smart G3 which depends on your regular savings plan annual premium.

- Limited tranche: from 4 January 2019 to 26 February 2019 or when the tranche size is met, whichever is earlier (the “Offer Period”).

- Early termination charges – results in getting back something definitely lower than your initial capital

- Huge initial cash outlay

Example: You save S$10,000 with AIA Smart G3 + S$200/month on regular premium plans

You need to first purchase AIA Regular Savings Plan, for example, a plan with a regular monthly premium of S$200 paid annually.

- Initial Cash Outlay: S$2,400 (Regular savings plan) + S$10,000 (AIA Smart G3) = S$12,400

If you held it till maturity (for 3 years) for AIA Smart G3 alone:

- Amount at maturity: S$10,927.27

- Amount saved with AIA Smart G3: S$927.27 over 3 years

- Amount saved with SSB (1.98%): S$605.83 over 3 years

- Higher return than SSB (with early penalty charges)

More details on AIA Smart G3 can be found here.

Where else can you put this S$10,000 apart from AIA Smart G3?

If you are not a fan of the huge initial cash outlay or if you are looking for low-risk alternatives to invest your money in, here are some other alternatives for you to consider:

- This month’s SSB at 1.98% for 3 years, minimum cash outlay S$500, no early termination charges. More details here.

- Voluntary cash top-up to CPF Ordinary Account (2.5%-3.5%), Special Account (4%-5%), and/or Medisave Account (4%-5%). More details here.

- 1.9% p.a. CIMB Fixed Deposits. More details here.

- OCBC Passbook or Statement Savings Account – Get S$110 worth of NTUC Fairprice gift vouchers for every S$10,000 and a limited edition gold or rose passbook. More details here.

- More high yielding interest rate savings account here.

- More alternative investment options can be read from this guide.

Advertisement