A Beginner's Guide To Participating Whole Life Insurance VS Investment Linked Policies (ILPs)

As a working adult fresh out of university, I was at times overwhelmed by the plethora of insurance policies out there.

Insurance is a complicated topic to broach, especially when you are a complete beginner at it.

Some of the more commonly talked about policies include Life Insurance, as well as Investment-Linked policies (ILPs).

To help you distinguish between the different policies, here’s a beginner’s guide to Whole Life Insurance plan and Investment-Linked Policies (ILPs)!

TL;DR: A Beginner’s Guide To Participating Whole Life Insurance VS Investment Linked Policies (ILPs)

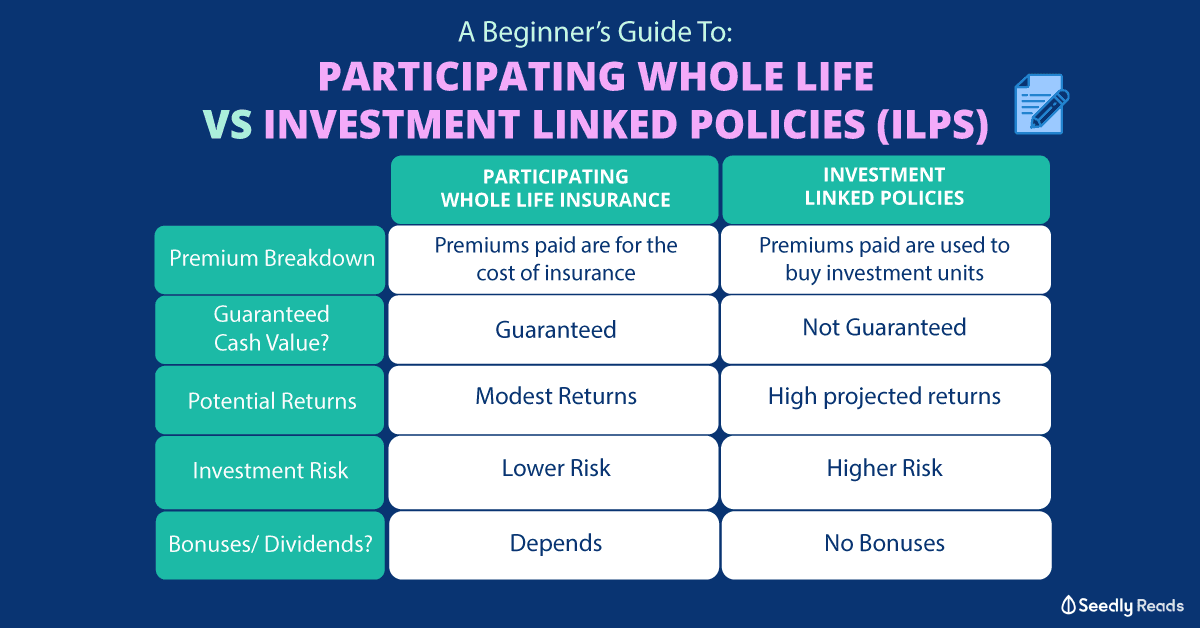

| Participating Whole Life Insurance | Investment Linked Policies | ||

|---|---|---|---|

| Similarities | - Both provides insurance coverage in the event of death or TPD. - Covers you for your whole life. - Accumulates cash value |

||

| Differences | Premium Breakdown | Premiums paid are for the cost of insurance. | Premiums paid are first used to buy investment units, which are then sold to pay for cost of insurance + other miscellaneous brokerage and admin fees. Investment returns are also used to offer you some insurance coverage. |

| Guaranteed Cash Value? | Cash value is guaranteed. You may get non-guaranteed bonuses/returns from this. | Cash value is not guaranteed. Actual returns may be higher or lower than projected. | |

| Potential Returns | Potential returns are modest, at about~3-4% | High projected returns of about ~4-8% | |

| Fund Choice | You do not need to pick a fund to invest in. | You have to pick a fund to invest in. | |

| Investment Risk | For those with guaranteed cash value, the insurance company bears the investment risk. Lower risk. | You bear the investment risk. Higher risk. |

|

| Any Bonuses? | Bonus depends on how the fund performs. If the fund does well, the bonus have to be declared by the insurer. | No Bonuses. Value of ILP depends on the sub funds you invest in. |

|

What is Participating Whole Life Insurance?

Participating Whole Life Insurance is an insurance policy that focuses on covering individuals against certain events. Upon death or permanent disability, you will get a lump sum payout which will be given to your loved ones. This amount is determined by the coverage that you get.

Participating Whole Life plans mean that premiums used are channeled in a fund that is used to invest in low-risk instruments like government bonds, etc.

What is an Investment-Linked Policy (ILP)?

ILP is an insurance product that invests your money in the market. This means potentially higher returns, but also higher volatility and risks.

ILPs also offer coverage should anything happen to the insured. As to how much coverage is agreed upon, it is worked out between the agent and the individual.

ILPs are often confused with participating whole life plans. They are, however very different. First, ILPs give you the freedom to choose the participating sub-funds you want to invest in. However, unlike participating whole life policies, ILPs have no guaranteed cash value, meaning that your returns are heavily reliant on the performance of the sub-funds invested in.

That said, there are two types of ILPs you can choose from:

- Single-Premium ILPs: This means that you pay for your ILP with a lump-sum premium, which will be used to purchase a sub-fund of your choice. This usually has less insurance protection than ILPs with regular premiums.

- Regular Premium ILPs: You can pay for your ILP with regular installments, and have the flexibility of adjusting your insurance coverage.

What’s The Similarities and Differences Between Them?

All these may seem really confusing, so here’s a quick overview of the similarities and differences between the two policies:

| Participating Whole Life Insurance | Investment Linked Policies | ||

|---|---|---|---|

| Similarities | - Both provides insurance coverage in the event of death or TPD. - Covers you for your whole life. - Accumulates cash value |

||

| Differences | Premium Breakdown | Premiums paid are for the cost of insurance. | Premiums paid are first used to buy investment units, which are then sold to pay for cost of insurance + other miscellaneous brokerage and admin fees. Investment returns are also used to offer you some insurance coverage. |

| Guaranteed Cash Value? | Cash value is guaranteed. You may get non-guaranteed bonuses/returns from this. | Cash value is not guaranteed. Actual returns may be higher or lower than projected. | |

| Potential Returns | Potential returns are modest, at about~3-4% | High projected returns of about ~4-8% | |

| Fund Choice | You do not need to pick a fund to invest in. | You have to pick a fund to invest in. | |

| Investment Risk | For those with guaranteed cash value, the insurance company bears the investment risk. Lower risk. | You bear the investment risk. Higher risk. |

|

| Any Bonuses? | Bonus depends on how the fund performs. If the fund does well, the bonus have to be declared by the insurer. | No Bonuses. Value of ILP depends on the sub funds you invest in. |

|

Should I get an ILP Or A Participating Whole Life Plan?

Before choosing an ILP or a participating whole life plan, you have to be aware that both plans are vastly different, and are used for different purposes.

For one, whole life plans offer more coverage, as you can get an early critical illness cover. Furthermore, premiums paid are a fixed premium payment term. So if you are considering getting a form of life insurance coverage, a whole life plan is something you should consider.

In retrospect, ILPs may not be as suitable for those looking at an extensive whole life coverage.

If you are holding onto an ILP for a long time, you may have to decrease your insurance coverage and depend on your investments for coverage.

You should not be looking to replace a whole life plan with an ILP, as you may risk losing coverage, as well as expose yourself to greater risk.

However, if you are looking to invest a sum of money, but don’t know how to DIY your own, ILPs are worth considering.

If you are planning to purchase an ILP, you can keep in mind the following:

- ILPs can be risky, as your money may take a hit if your sub-funds perform poorly due to a volatile market.

- There have been criticisms that some ILPs may have a relatively high sales charge, ongoing charges and low allocation rates for buying units in the first few years. So do check on these components with your agent, if you decide to purchase an ILP.

Overall, whether it is an ILP or a participating whole life insurance, make sure that you question your agent thoroughly on any doubts you may have of the plan! Don’t buy a policy for the sake of buying, and make sure you get the best plan that fits your long term goals and needs!

Advertisement