Best Robo Advisors Comparison Guide (2026): Stashaway vs Syfe vs Endowus & More

Seedly

Seedly●

Thinking of investing but not sure where to start?

You are not alone. Robo-advisors have become a popular way for Singapore investors to build diversified portfolios without having to pick every ETF, unit trust, or stock themselves.

But which is the best robo advisor in Singapore for you?

The answer depends on what you care about most: fees, minimum investment amount, CPF or SRS support, portfolio choices, custody arrangements, and how hands-on you want to be.

This non-sponsored guide compares the major robo-advisors available to Singapore investors, focusing mainly on investment portfolios rather than cash-management products.

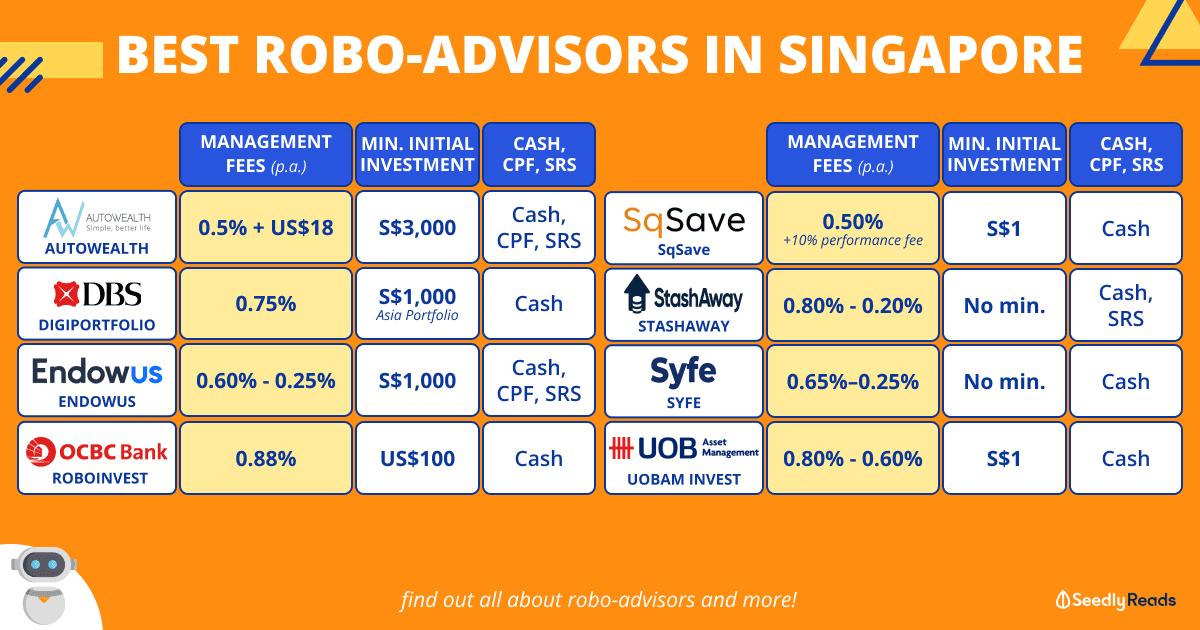

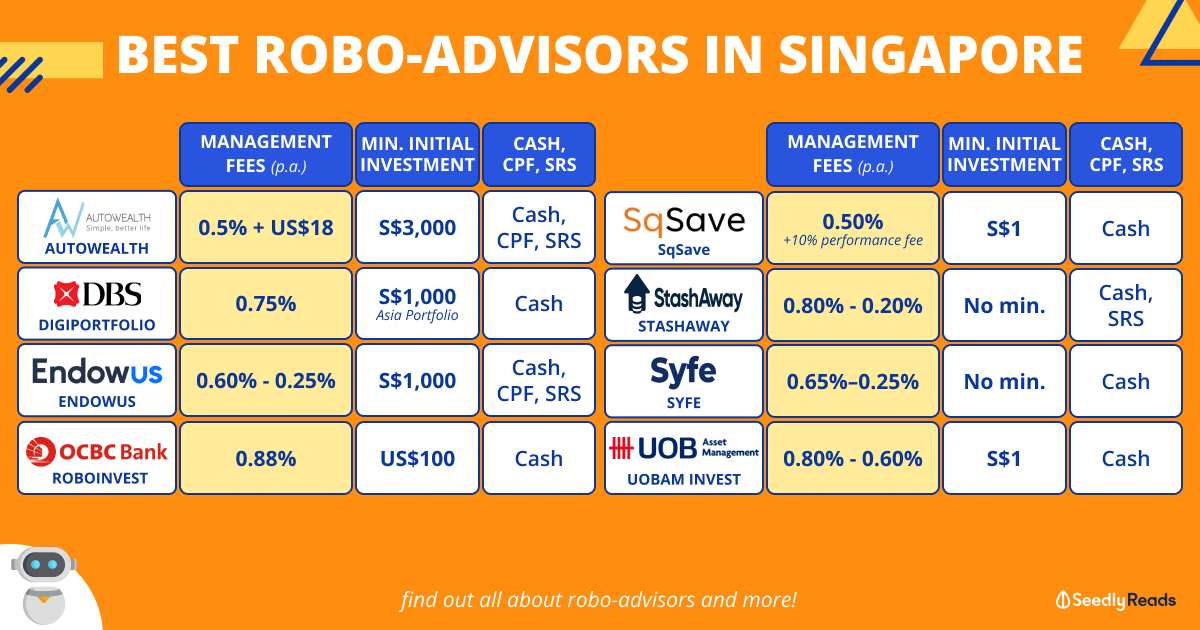

TL;DR: Best Robo-Advisors in Singapore at a Glance

Looking for a quick comparison before reading the full breakdown? Here is a snapshot of the main robo-advisors in Singapore, based on their standard fees, minimum investment amounts, and whether they support cash, CPF, or SRS funding.

What Is A Robo-Advisor?

A robo-advisor is a digital investment platform that uses technology to recommend and manage an investment portfolio based on your goals, risk profile, time horizon, and other information you provide.

In simple terms, it helps you invest without needing to choose every individual security yourself.

Most robo-advisors do a few things:

- They ask you questions to understand your risk profile.

- They recommend a portfolio.

- They invest your money into a basket of assets such as ETFs, unit trusts, equities, bonds, REITs, or money market funds.

- They rebalance the portfolio when needed.

- They charge a platform, advisory, or management fee.

Compared to doing everything yourself, robo-advisors can be useful if you want a more guided investing experience. Compared to traditional managed funds or advisory services, they may also have lower platform fees, although you still need to check underlying fund-level fees, GST, FX spreads, custody fees, and any performance fees.

For Singapore investors comparing robo-advisor performance Singapore-wide, remember that returns should not be viewed in isolation. A higher-return portfolio may simply be taking on more risk. Look at fees, asset allocation, risk level, drawdowns, and whether the portfolio suits your goals.

Also, while robo-advisors are convenient, they are not risk-free. Your capital is still exposed to market movements.

Robo-Advisor Fees

When comparing robo-advisors, do not just look at the headline management fee.

Check for:

- Platform, advisory, or management fees

- Underlying ETF or fund-level fees

- GST

- FX conversion spreads

- Custody or safekeeping fees

- Performance fees

- Withdrawal, transfer, or early-exit charges

- Minimum account or portfolio sizes

Some platforms look cheap at first glance but may have extra charges. Others may charge more but give you access to CPF, SRS, or a wider fund universe.

A Brief Introduction to the Robo-Advisors in Singapore

AutoWealth

-

Operation Licence

AutoWealth Private Limited is listed by MAS as a Licensed Financial Adviser for advising on investment products, including collective investment schemes and securities.

Management Fees / Platform Fees

AutoWealth currently lists these fee structures:

- AutoWealth Starter: 0.50% p.a. advisory fee + US$18 annual platform fee

- AutoWealth SRS: 0.40% p.a. advisory fee + US$18 annual platform fee

- AutoWealth CPF: 0.28% p.a. standard advisory fee

- AutoWealth Plus+: 8% performance fee on profits

AutoWealth also has cash-management options, but this guide focuses mainly on investment portfolios.

Minimum Amount to Start

- AutoWealth Starter: S$3,000

- AutoWealth CPF: S$3,000

- AutoWealth Plus+: S$10,000

Cash / CPF / SRS

AutoWealth supports cash, CPF, and SRS investing.

For CPF investing, you will need a CPF Investment Account with a local bank before your CPF OA funds can be invested.

Investment Methodology

AutoWealth builds globally diversified portfolios and manages the portfolio allocation based on your risk profile. Its current Starter portfolio page states exposure to over 8,000 stocks and 600 government bonds.

Safety

For AutoWealth, client portfolios are held in segregated custody accounts. AutoWealth’s current FAQ states that cash portfolios are held with Saxo Capital Markets, while SRS portfolios use Phillip Securities.

Miscellaneous

AutoWealth gives clients access to a wealth manager, including via WhatsApp, which may be useful if you want a more human-assisted experience rather than a fully app-only journey.

DBS digiPortfolio

Operation Licence

DBS Bank Ltd is listed by MAS as an exempt capital markets services entity and exempt financial adviser.

Management Fees

DBS digiPortfolio currently lists these fees:

- SaveUp Portfolio: 0.25% p.a.

- Income Portfolio: 0.75% p.a.

- Asia Portfolio: 0.75% p.a.

- Retirement Portfolio: 0.75% p.a.

- Global Portfolio ETF: 0.75% p.a.

- Global Portfolio UT: 0.75% p.a.

- Global Portfolio Plus: 0.75% to 0.85% p.a.

Minimum Amount to Start

- SaveUp Portfolio: S$100

- Income Portfolio: SGD/USD100

- Asia Portfolio: SGD1,000

- Retirement Portfolio: S$1,000

- Global Portfolio ETF: USD1,000

- Global Portfolio UT: SGD/USD1,000

- Global Portfolio Plus: SGD/USD10,000

Cash / CPF / SRS

DBS digiPortfolio is a cash-funded option.

Investment Methodology

DBS digiPortfolio portfolios are managed by DBS’ investment team. DBS states that the portfolios are monitored and rebalanced, with fund selection handled by DBS.

Investment Portfolios

DBS digiPortfolio currently includes:

- SaveUp Portfolio

- Income Portfolio

- Asia Portfolio

- Retirement Portfolio

- Global Portfolio ETF

- Global Portfolio UT

- Global Portfolio Plus

This may appeal to you if you prefer investing through a bank you already use.

Endowus

Operation Licence

Endowus Singapore Pte Ltd is listed by MAS as a CMS licensee and exempt financial adviser.

Management Fees

Endowus fees depend on the type of portfolio and funding source.

Current listed fees include:

- Cash management portfolios: 0.15% p.a.

- Single-fund mid/long duration portfolios: 0.30% p.a.

- Multi-fund CPF/SRS portfolios: 0.40% p.a.

- Multi-fund cash portfolios: 0.25% to 0.60% p.a., depending on assets under advice

Fund-level fees still apply, but Endowus rebates trailer fees where applicable.

Minimum Amount to Start

Endowus Fund Smart lists a S$1,000 minimum initial investment.

Cash / CPF / SRS

Endowus supports cash, CPF, and SRS investing.

Investment Methodology

Endowus focuses on access to funds, including institutional share classes where available, and rebates trailer fees to clients. It offers advised portfolios as well as Fund Smart for investors who want to select funds.

Investment Portfolios

Endowus offers different portfolio types across cash, CPF, and SRS. Depending on your goal, you may choose advised portfolios, income-focused portfolios, Fund Smart, or cash-management portfolios.

Safety

Endowus states that client assets are held in the client’s name through a custody arrangement with UOB Kay Hian.

This makes Endowus one of the more relevant platforms if you want a robo-advisor-style solution for CPF and SRS funds.

OCBC RoboInvest

Operation Licence

OCBC Bank is listed by MAS as an exempt capital markets services entity and exempt financial adviser.

Management Fees

OCBC RoboInvest charges 0.88% p.a., computed and charged monthly.

Minimum Amount to Start

OCBC RoboInvest portfolios start from USD100.

Cash / CPF / SRS

OCBC RoboInvest is cash-funded. Funding is done in SGD, and foreign-currency portfolios are converted where needed.

Investment Methodology

OCBC RoboInvest offers curated portfolios and automated portfolio management. OCBC states that ETF portfolios are screened and rebalanced semi-annually.

Investment Portfolios

OCBC RoboInvest currently offers 38 portfolios across different themes and markets. It may suit investors who prefer a bank-backed robo-investing option and want access to curated portfolios from a familiar banking app.

Safety

OCBC states that Saxo is appointed as custodian and trade execution agent for OCBC RoboInvest.

SqSave (formerly SquirrelSave)

Operation Licence

PIVOT Fintech Pte Ltd is listed by MAS as a CMS licensee and exempt financial adviser.

Management Fees

SqSave charges:

- 0.50% p.a. management fee

- 10% performance fee on positive returns, subject to its high-water mark methodology

SqSave also states that special fee rates may be available on request for assets above S$500,000.

Minimum Amount to Start

SqSave has no minimum amount to open an account and no minimum balance requirement. Its app states that you can invest from S$1.

Cash / CPF / SRS

SqSave is a cash-funded platform.

Investment Methodology

SqSave uses an AI-driven approach to build globally diversified portfolios using ETFs. Its DAAS process selects from a pool of ETFs and allocates according to your profile.

Investment Portfolios

SqSave’s Global ETF portfolios are designed to offer diversified exposure across global assets.

Safety

SqSave states that client monies and investments are held separately by custodians, including Tiger Brokers Singapore, State Street Bank and Trust Company, and UOB.

StashAway

Operation Licence

Asia Wealth Platform Pte Ltd is listed by MAS as a CMS licensee and exempt financial adviser.

Management Fees

StashAway charges tiered management fees for investment portfolios:

- First S$25,000: 0.80% p.a.

- Next S$25,000 to S$50,000: 0.70% p.a.

- Next S$50,000 to S$100,000: 0.60% p.a.

- Next S$100,000 to S$250,000: 0.50% p.a.

- Next S$250,000 to S$500,000: 0.40% p.a.

- Next S$500,000 to S$1 million: 0.30% p.a.

- Above S$1 million: 0.20% p.a.

Its Flexible Portfolio Single ETF option is listed at 0.30% p.a.

Minimum Amount to Start

StashAway has no minimum investment amount for many of its investment portfolios.

Cash / CPF / SRS

StashAway supports cash and SRS investing, depending on the product.

Investment Methodology

StashAway offers managed and flexible portfolios across different themes and strategies. Portfolio options include General Investing, Shariah Global Portfolio, Flexible Portfolios, Goal-based Investing, Income Investing, Singapore Investing, Thematic portfolios, and other ETF-based options.

Investment Portfolios

StashAway may appeal to investors who want no minimum investment amount and a broad range of portfolio styles, from general investing to thematic and income-focused portfolios.

Safety

StashAway states that client deposits are held in a DBS trust account, and investments for relevant portfolios are held in custody with Saxo.

Syfe

Operation Licence

Syfe Pte Ltd is listed by MAS as a CMS licensee and exempt financial adviser.

Management Fees

Syfe’s managed portfolio fees are based on client tier:

- Blue: 0.65% p.a., no minimum

- Black: 0.55% p.a., from S$50,000

- Gold: 0.45% p.a., from S$250,000

- Platinum: 0.35% p.a., from S$1 million

- Diamond: 0.25% p.a., from S$5 million

Minimum Amount to Start

Syfe generally has no minimum investment amount.

However, for REIT+ and Income+, you need S$5,000 if you want dividends paid out to your bank account instead of reinvested.

Cash / CPF / SRS

Syfe supports cash investing and SRS funding for supported managed portfolios.

Investment Methodology

Syfe offers a range of managed portfolios and cash-management products. Its investment portfolio options include Core, Equity100, Equity Alpha, Themes, Income+, REIT+, Custom, and other portfolio types.

Investment Portfolios

Syfe may be suitable if you want low or no minimums, SRS-supported portfolios, or a choice between broad market, REIT, income, thematic, and custom portfolios.

Safety

Syfe states that client funds are held in trust accounts with DBS and HSBC, while investments are held with Saxo as custodian.

UOBAM Invest

Operation Licence

UOB Asset Management Ltd is listed by MAS as a CMS licensee and exempt financial adviser.

Management Fees

UOBAM Invest charges:

- 0.80% p.a. on the first S$25,000

- 0.60% p.a. above S$25,000

Minimum Amount to Start

You can start investing from S$1.

Cash / CPF / SRS

UOBAM Invest is cash-funded.

Investment Methodology

UOBAM Invest uses your risk profile, investment goals, and algorithm-based portfolio construction. UOBAM also states that its portfolio committee reviews portfolios quarterly.

Investment Portfolios

UOBAM Invest offers portfolios that invest through ETFs and unit trusts across asset classes such as equities, bonds, and money market instruments. Current portfolio options include Global and Global Impact portfolios.

Safety

UOBAM Invest is backed by UOB Asset Management’s investment infrastructure and MAS-regulated status.

UTRADE Robo by UOB Kay Hian

Operation Licence

UOB Kay Hian Private Limited is listed by MAS as a CMS licensee.

Management Fees

UTRADE Robo charges:

- 0.88% p.a. for assets up to S$50,000

- 0.68% p.a. for assets above S$50,000 and up to S$100,000

- 0.50% p.a. for assets above S$100,000

These fees are subject to GST.

Minimum Amount to Start

The minimum initial investment is S$5,000 per portfolio. Subsequent top-ups start from S$500.

Cash / CPF / SRS

UTRADE Robo currently supports cash funding. CPF is not supported at this stage.

Investment Methodology

UTRADE Robo uses modern portfolio theory, ETF selection, portfolio implementation, rebalancing, and recalibration. It selects ETFs from a broad ETF universe and builds portfolios based on your risk profile and goals.

Investment Portfolios

UTRADE Robo says its ETF portfolios provide access to global diversification across more than 7,000 stocks and bonds.

Safety

UTRADE Robo is provided by UOB Kay Hian Private Limited, which holds a MAS Capital Markets Services Licence.

So… Which Robo Advisor Should You Use?

A search for “Singapore best robo advisor” will give you many options, but there is no single answer that works for everyone.

Here is a simple way to narrow it down.

If you want the best robo advisor for beginners, start by comparing platforms with low or no minimum investment amounts. StashAway, Syfe, SqSave, UOBAM Invest, DBS SaveUp, and OCBC RoboInvest may be worth looking at first because they have relatively accessible entry points.

If you want to invest CPF or SRS funds, Endowus remains one of the most comprehensive options in this list because it supports cash, CPF, and SRS. AutoWealth also supports cash, CPF, and SRS investing, while StashAway and Syfe support SRS for selected portfolios.

If you prefer a bank-backed platform, DBS digiPortfolio, OCBC RoboInvest, UOBAM Invest, and UTRADE Robo may feel more familiar.

If you care most about costs, compare the full fee stack. Do not just look at the management fee. Check GST, underlying fund fees, FX spreads, custody or safekeeping fees, performance fees, and withdrawal or transfer charges.

If you care about performance, compare each platform’s official portfolio performance updates with care. Make sure you are comparing portfolios with similar risk levels, asset allocation, currencies, and time periods.

Here’s What Real Users Have to Say About the Various Robo Advisors

Would you prefer to hear from actual people and users who have used robo-advisors, before making your decision?

Our Seedly community members have left honest reviews covering stuff like the pros and cons of each robo-advisor as well as the returns they have made.

You can use this one-stop portal to compare ALL the robo-advisors on the market and see which is the one for you!

The Importance of Doing Your Own Diligence Before Investing

Before investing, read user reviews, compare official fee schedules, and understand how each platform handles custody, withdrawals, rebalancing, and risk.

Robo-advisors can make investing easier, but they do not remove investment risk.

The best robo-advisor for you is the one that fits your goals, risk appetite, funding source, and investing style — while keeping costs transparent.

Related Articles

- A Dummy’s Guide to Investing in Robo Advisors

- What Are Robo-Advisors? We Answer 5 Common Questions!

- Robo Advisors Singapore: 6 Reasons Why You Should Invest With Robos And 3 Reasons Why You Should Not

- Robo Advisors vs S&P 500: Which Should You Pick As Your First Investment?

- Robo Advisors Returns Revealed: StashAway, Endowus, Syfe, Kristal.AI and More!

- Budget 2023 Singapore Summary

- Best Credit Card in Singapore

- Best Travel Insurance in Singapore

Advertisement