Your 7.7 cart costs S$600.

One credit card advertises 20% rebates. Another offers 10% cashback. A third gives 5%.

The 20% card must be the obvious winner, right?

Not once the cashback caps come in.

The Lazada-UOB Card’s current 20% Lazada rebate is capped at S$20. On a S$600 purchase, that works out to an effective return of just 3.33%. Meanwhile, the Maybank XL Cashback Card’s 5% rate would return S$30, assuming you meet its S$500 monthly spending requirement and the transaction qualifies.

That is the problem with choosing a credit card for online shopping during 7.7: the headline rate is easy to compare, but the usable reward on your actual cart is what matters.

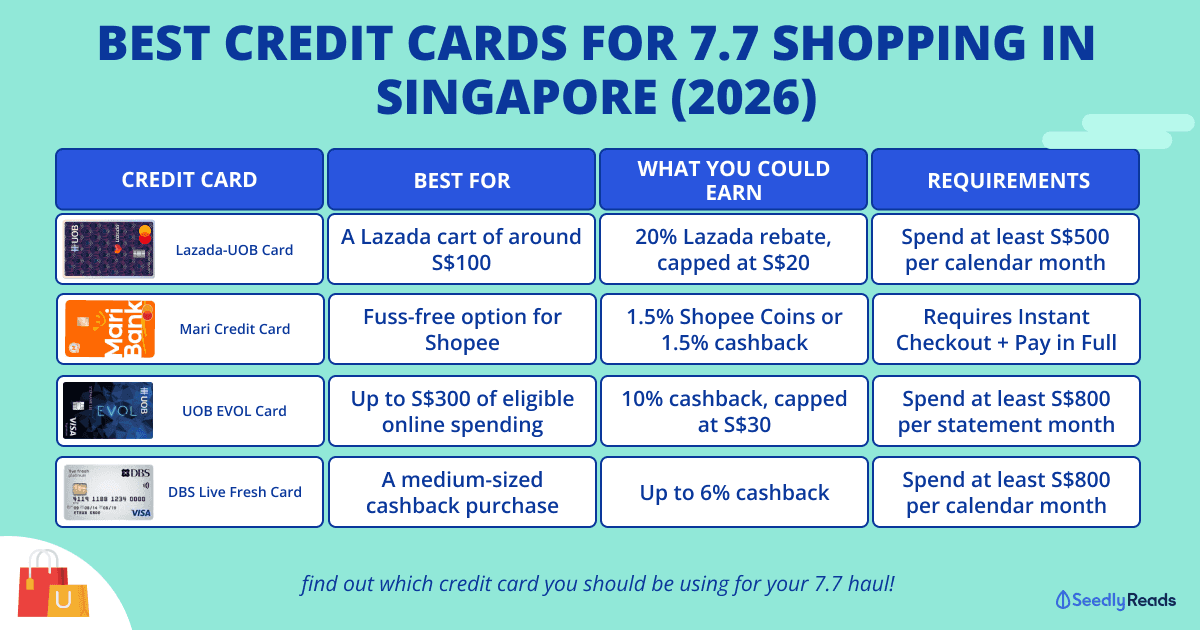

TL;DR: Which Credit Card Should You Use For 7.7?

| Your 7.7 purchase | Best card to check first | What you could earn | Main catch |

|---|---|---|---|

| Lazada purchase of around S$100 | Lazada-UOB Card | 20% Lazada rebate, capped at S$20 | Requires S$500 total monthly spend; rebate is issued as Lazada Gift Card credit. |

| Shopee purchase with no minimum-spend target | Mari Credit Card | 1.5% cashback plus 1.5% Shopee Coins | Coins require Mari Credit Card Instant Checkout and full payment. |

| General online purchase of around S$200 | CIMB Visa Signature | 10% cashback, capped at S$20 for online shopping | Requires S$800 in the same statement month. |

| General online purchase of up to S$300 | UOB EVOL Card | 10% cashback, with a S$30 shared cap | Requires S$800 per statement month; online and mobile-contactless purchases share the S$30 cap. |

| Online SGD purchase of around S$300 | OCBC FRANK Card | 8% cashback, capped at S$25 for the category | Requires S$800 qualifying monthly spend. |

| Larger online-shopping cart | DBS Live Fresh or Maybank XL Cashback | Up to 6% or 5% respectively | DBS requires S$800 monthly; Maybank XL requires S$500 monthly. |

| Large cart and already eligible for the introductory rate | HSBC Live+ | 8% cashback, capped at S$250 per calendar quarter | Only for eligible new-to-HSBC Live+ cardholders during their first two qualifying quarters. |

| No minimum spend and no tracking | UOB Absolute Cashback | 1.7% cashback | It is an American Express card, so check that the platform accepts it. |

For this comparison, a card makes the shortlist if it offers at least one of the following:

- A platform-specific Shopee or Lazada reward

- At least 5% cashback on qualifying online shopping

- At least 4 miles per S$1 on qualifying online spending

- A simple, no-minimum-spend return of at least 1.6%

This is not about finding the card with the biggest number in its advertisement. It is about finding the card whose requirements match the way you already spend.

First, Calculate The Reward You Can Actually Use

Use this formula before deciding which credit card is best for shopping:

Usable reward = lower of (eligible spend × reward rate) or remaining reward cap

Then ask three more questions:

- Will you meet the card’s minimum monthly or quarterly spend?

- Have you already used part of its cashback or miles cap?

- Will Shopee or Lazada code the purchase under an eligible merchant category?

A 10% card with a S$20 online-shopping cap is effectively a 10% card only for the first S$200.

Do not manufacture S$800 of spending just to earn S$20 cashback. That is the card winning, not you.

Best Platform-Specific Cards For Shopee And Lazada

Lazada-UOB Card: Best For The First S$100 Of Lazada Spending

The Lazada-UOB Card currently gives 20% rebates on eligible Lazada spending after you charge at least S$500 to the card in the calendar month.

The problem is the S$20 monthly Lazada rebate cap.

That means the full headline rate applies only to the first S$100 of eligible Lazada spending:

S$100 × 20% = S$20

A S$300 Lazada purchase still earns a maximum S$20, reducing the effective return to 6.67%. On a S$600 purchase, the effective return falls to 3.33%.

The rebate is also issued as Lazada Gift Card credit rather than ordinary cash credited against your card bill.

Best for: A smaller Lazada cart, provided you were already going to hit S$500 of total card spending that month.

Skip it when: Your Lazada cart is much larger than S$100 and another card can give 5% to 8% across more of the purchase.

Mari Credit Card: Best No-Minimum-Spend Card For Shopee

For eligible local card spending, the Mari Credit Card gives 1.5% unlimited cashback with no minimum spend.

When you pay for Shopee purchases in full through Mari Credit Card Instant Checkout, you also receive 1.5% in Shopee Coins. The Shopee Coins promotion is stated to run until 31 December 2026.

This is not the highest headline rate in the market, but it is one of the easiest to use. There is no S$800 target to monitor and no S$20 online-shopping cap.

Just remember that half of the platform-specific reward comes as Shopee Coins, not cash.

Best for: Shopee shoppers who do not want to track monthly spending targets or category caps.

Skip it when: You can comfortably meet a high-rate cashback card’s requirements or prefer 4 miles per S$1.

UOB One Card: Potentially The Highest Shopee Rate, But Not A One-Day Strategy

The UOB One Card can provide up to 10% total cashback at Shopee under its regular structure.

Eligible new-to-UOB customers approved between 15 May and 30 September 2026 can receive enhanced cashback of up to 20% at Shopee during their first qualifying quarter.

The catch is substantial.

You must make at least 10 purchases and spend S$600, S$1,000 or S$2,000 in each month of the qualifying three-month quarter. Cashback is then paid quarterly. The maximum rate depends on the tier you maintain.

So yes, the 20% headline is real. But this is a three-month spending plan, not a card to apply for purely because you have one 7.7 order.

Best for: Existing UOB One users already meeting the quarterly requirements, or new users who genuinely want the card beyond 7.7.

Skip it when: You would have to invent spending or make unnecessary transactions to preserve the quarterly tier.

Best Cashback Cards For Smaller 7.7 Carts

CIMB Visa Signature: 10% On The First S$200

The CIMB Visa Signature offers 10% cashback on online shopping after at least S$800 is posted in the same statement month.

Online-shopping cashback is capped at S$20 per category, while the total monthly cashback cap is S$100 across all eligible categories. Spending beyond the category cap earns the 0.2% base rate.

This makes it strongest for roughly the first S$200 of eligible online shopping:

S$200 × 10% = S$20

It may be a good 7.7 card when the rest of your S$800 monthly target comes from purchases you already intended to make.

It is much less attractive when the 7.7 order is your only spending on the card.

UOB EVOL: 10% With A Larger S$30 Shared Cap

The UOB EVOL Card offers 10% cashback on eligible local online and mobile-contactless spending after S$800 per statement month.

The relevant cashback is capped at S$30, shared between online spending and mobile-contactless purchases. If you miss the minimum spend, the affected categories earn only the 0.3% base rate.

If the shared cap is completely unused, the headline rate covers up to S$300:

S$300 × 10% = S$30

Check how much mobile-contactless spending you have already made before 7.7. Your meals and in-store Apple Pay purchases may already have eaten into the same cap.

OCBC FRANK: 8% On Online SGD Spending

The OCBC FRANK Credit Card gives 8% cashback on qualifying online transactions in Singapore dollars after S$800 of monthly qualifying spend.

The online-SGD category is capped at S$25, while total monthly cashback across its categories is capped at S$100. Spending below the S$800 threshold earns 0.3%.

Its full 8% rate therefore covers up to S$312.50:

S$25 ÷ 8% = S$312.50

It is not as eye-catching as 10%, but the slightly larger usable spending range means FRANK can match or beat a 10% card once that card’s smaller category cap is exhausted.

Best Cashback Cards For Larger 7.7 Purchases

DBS Live Fresh: Up To 6% With A Higher Shopping Cap

DBS Live Fresh offers:

- 0.3% base cashback on eligible spending

- An additional 5.7% on qualifying shopping

- A S$50 monthly cap on the additional shopping cashback

You need S$800 of total calendar-month spending to receive the additional cashback.

This gives it considerably more room than cards with S$20 or S$30 category caps.

On a qualifying S$600 shopping purchase, the total return would be S$36 before considering any bank voucher:

S$600 × 6% = S$36

Best for: Medium-to-large carts when you can naturally meet the S$800 monthly target.

Maybank XL Cashback: 5% With A Lower S$500 Minimum

The Maybank XL Cashback Card offers 5% cashback across its Dine, Shop, Travel and Play categories, including qualifying online shopping.

It requires S$500 of total spending in the calendar month and has a monthly bonus-cashback cap of S$80. Other qualifying transactions earn 0.2%.

The 5% rate is lower than DBS Live Fresh’s 6%, but Maybank’s lower S$500 minimum can be much easier to meet without forcing extra spending.

The S$80 bonus cap also gives the card enough room for up to S$1,600 of eligible spending at 5%.

Best for: Bigger carts and shoppers who prefer a lower monthly hurdle over the highest headline rate.

HSBC Live+: 8% For Eligible New Cardholders

HSBC Live+ offers 8% cashback on qualifying online and offline shopping for eligible new-to-HSBC Live+ cardholders during their first two calendar quarters.

The 8% consists of 5% base cashback and 3% additional cashback, with total cashback capped at S$250 per calendar quarter.

However, the spending test depends on when your card was issued.

For example, someone whose card was issued between April and June 2026 must spend at least S$600 in eligible purchases in each month from July to September 2026 to qualify for 8% during that quarter.

This can be the strongest cashback option for a large 7.7 purchase — but only when you already hold the card and understand which qualifying quarter applies to you.

It is not a straightforward last-minute application pick.

Other High-Return Cards That Require More Planning

These cards can be excellent, but they are easier to get wrong.

| Card | Potential 7.7 return | Why it is not a simple recommendation |

| Maybank Family & Friends | 6% after S$800 monthly spend or 8% after S$1,600; online-shopping cap is S$20 or S$30 respectively | Online Shopping must be one of your selected preferred categories. Category changes take effect the following month and remain for three months, so existing users should set it during June for July spending. |

| Trust Cashback Card | Up to 15% bonus cashback on a selected preferred category, plus up to 1% instant base cashback | The preferred-category reward is capped at S$250 per quarter and depends on quarterly spending. Trust’s published top-tier illustration uses S$2,000 of spending per month over three months. |

| POSB Everyday Card | 5% on Amazon.sg, Lazada, Shopee, RedMart, Taobao and TikTok Shop | Requires S$800 monthly qualified spend and has a S$20 online-shopping cap. |

| Citi SMRT Card | 5% savings on eligible online purchases | Requires S$500 per statement month; spending below that receives only the 0.3% base rate. Mobile-wallet and travel-related online transactions are excluded from the online category. |

| UOB One Card | Up to 10% at Shopee, or up to 20% for eligible new-to-UOB cardholders during the first qualifying quarter | Requires 10 transactions and the same S$600, S$1,000 or S$2,000 monthly tier across a three-month quarter. |

These are worth considering when you already have the card and its spending system is in place.

Applying for one purely to chase a 7.7 purchase may create more work than reward.

Best Cards With No Minimum Spend

Not everyone wants to track a statement month, five spending categories and three different caps.

For a smaller purchase, a flat-rate card can be the more sensible option.

| Card | Reward | Catch |

| UOB Absolute Cashback | 1.7% cashback on selected local spending, with no minimum spend and no cashback cap | American Express acceptance is required. Some commonly excluded local transaction types receive 0.3% instead. |

| Citi Cash Back+ | 1.6% cashback with no minimum retail spend and no cap | Lower reward than category cards, but far less tracking. |

| OCBC Infinity | 1.6% unlimited cashback on eligible online and in-store transactions | No minimum spend; exclusions still apply. |

A flat 1.6% or 1.7% return is not very exciting. But it is still better than aiming for 10%, missing the minimum spend and receiving only 0.2% or 0.3%.

Worked Example: A S$600 Lazada Purchase

Assume the transaction qualifies, the relevant caps are unused and all spending requirements are met.

| Card | Reward | Effective return |

| Lazada-UOB | S$20 Lazada Gift Card credit | 3.33% |

| Maybank XL Cashback | S$30 | 5% |

| DBS Live Fresh | S$36 | 6% |

| HSBC Live+ | S$48 | 8% |

This is why Lazada-UOB is not automatically the best credit card for a large Lazada purchase despite advertising 20%.

The card is strongest at the beginning of the cart. Once the S$20 cap is reached, a lower-rate card with more headroom can overtake it.

Treat Bank Vouchers As An Add-On

A 7.7 bank voucher can still change the winning card, especially if it gives an immediate fixed-dollar discount.

But compare the whole outcome:

Bank voucher + ordinary card reward

versus:

Reward from your best cashback or miles card

For example, consider a hypothetical S$600 purchase:

- A 5% cashback card returns S$30.

- A different card offering a S$15 bank voucher and 0.3% cashback returns S$16.80 in total.

- A S$40 bank voucher would change the result.

Do not choose a card automatically just because its logo appears beside a 7.7 voucher. Check whether the immediate discount is large enough to compensate for the cashback or miles you are giving up.

Also confirm that the voucher has been deducted before paying. A voucher sitting in your account is not a saving until it appears in the final checkout total.

Bottom Line: Match The Card To The Cart

There is no single best credit card for shopping during every 7.7 sale.

The practical winners are:

- Lazada-UOB for roughly the first S$100 of eligible Lazada spending

- Mari Credit Card for a low-fuss Shopee purchase with no minimum spend

- CIMB Visa Signature, UOB EVOL or OCBC FRANK for smaller general online purchases when you meet the monthly requirement

- DBS Live Fresh, Maybank XL Cashback or eligible HSBC Live+ accounts for larger carts

- Citi Rewards, DBS Woman’s World, OCBC Rewards or HSBC Revolution when collecting miles

- UOB Absolute Cashback, Citi Cash Back+ or OCBC Infinity when you want a simple fallback without chasing spending targets

Check your remaining cap, not just the advertised rate. Then add any live bank voucher and compare the final result before paying.

Advertisement