To Borrow or Not to Borrow - Is It a Good Idea to Take out a Loan to Invest?

Joel Koh

Joel Koh●

I recently came across this discussion post that someone from our Seedly Community on Facebook shared.

A rather interesting discussion about borrowing to invest was unfolding over this Straits Times article where:

Earlier this year, 31-year-old insurance agent Heng Kai Sheng got advances on three separate credit cards to the tune of $150,000. With the money, he opened a share-financing account at a local bank and pledged the lot as collateral. He was granted leverage of around 3.5 times, a $500,000 kitty Mr Heng’s ploughing into the stock market.

Mr Heng said he has a three- to-five-year horizon for his investments, and maintains he’s doing the maths to make sure he can always cover the interest, which ranges from 1.38% to 2.03% on the credit cards.

My immediate thought?

This crazy risky strategy got me thinking, when is it ever a good idea to take up a loan to invest?

Note: This does not constitute investment advice. The information here is for educational purposes and/or for study or research only.

TL;DR: Borrowing to Invest is an inherently high risk/high reward investment strategy.

Here are the risks you need to carefully consider before proceeding.

- Borrowing money to invest multiplies your gains but also your losses

- Borrowing money to invest guarantees your liability

- Returns from investments are not guaranteed especially in this volatile market

- Possibility of job loss or loss of ability to create capital

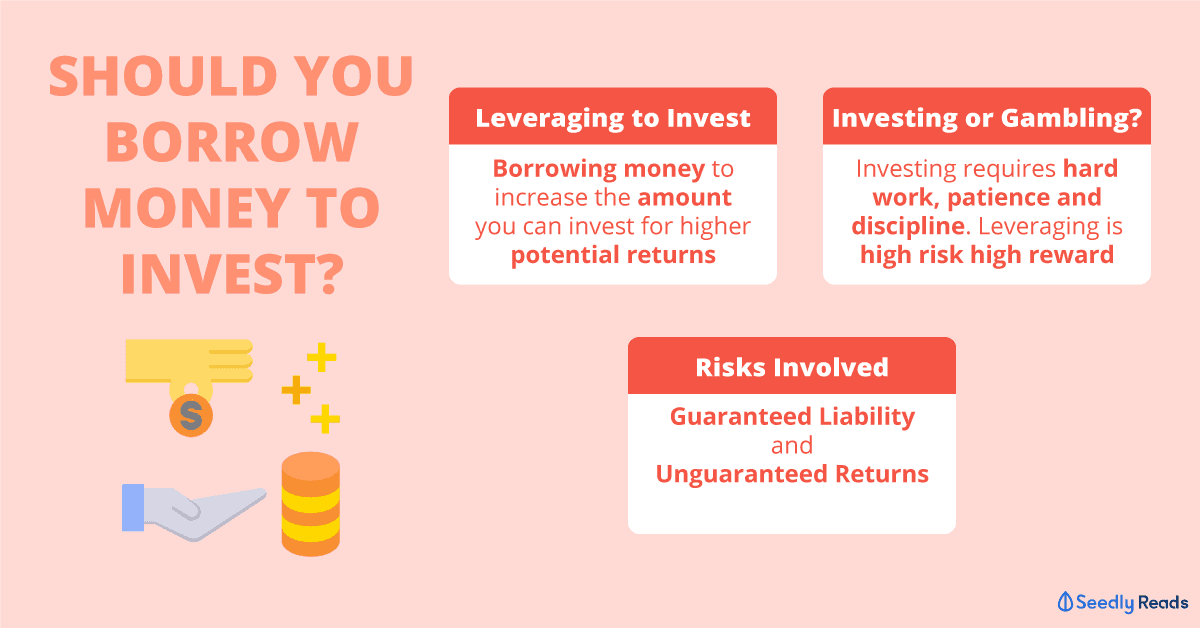

Leveraging to Invest

Somebody once told me that the key to building wealth is to borrow money to invest. Work, patience and discipline to save up be dammed.

It’s tempting to see how this can play out when investing in real estate.

For example, you might have $100,000 to invest over a one-year time frame. We will explore two scenarios

The first scenario will be to buy a house that costs $100,000. The house may appreciate 10% in a year giving you a $10,000 return on your investment.

For the second scenario, you can choose to use the $100,000 as the downpayment to buy a $1 million home and take up a housing/mortgage loan to pay for the rest of it.

If the house appreciates 10% like the first scenario. You would have gained a 100% return on your investment and earnt $100,000!

That’s the power of using debt – known in financial lingo as leverage.

Leverage refers specifically to an investment strategy where you borrow money/capital to increase the amount of money you can use to invest in order to increase the potential returns on your investments.

Leverage multiplies your gains in good times but herein lies the problem; it also multiplies your losses in bad times.

Let’s say the house’s value were to drop 10% after a year.

For the first scenario, you still can sell the house for $90,000 and only lose $10,000 or 10% of your investment,

For the second scenario, the lost will be staggering since you are leveraging. A 10% drop for the $1 million dollar home means that you will lose $100,000 or 100% of your initial investment.

In addition, you will have to pay the interest on the home loan for your house as well.

Investing or Gambling?

Investing is all about weighing the potential reward you receive against the risk of losses.

Investing means that you take the savings you have acquired through hard work, patience and discipline and make the money work for you.

Trying to take a short cut by leveraging to invest is a high-risk/high return strategy that in my opinion borders on gambling.

However, there are situations where it may work.

Leveraging to invest can work when the return on investment of the loan is high and the risk level of the investment is low.

It also comes with a whole host of risks:

- Your liability/costs are guaranteed. You will have to pay off the loan eventually or possibly declare bankruptcy.

- The investment needs to mature before the loan term.

- Returns are not guaranteed especially in this volatile market we are experiencing now due to the impact of COVID-19

- Need to service the loan monthly and high-interest rate/penalties if you are unable to pay on time. You have to consider that losing your job in this market is a real possibility

In general, investors should avoid investing their loans in a risk vehicle like derivatives or the stock market.

Leveraging to Invest in the Stock Market – A Hypothetical Case Study

For this discussion, we will be looking at the strategy behind leveraging to invest in a high-risk vehicle like the stock market and the risks involved.

A good example to show this will be to explore Mr Heng Kai Sheng’s investment strategy which he was comfortable sharing publicly with the Straits Times.

Although the facts of this situation are based on the numbers Mr Heng has provided, we will be exploring a hypothetical situation with a fictional Mr H.

I have no qualms in saying that what Mr Heng is doing is extremely risky. He is stacking leverage on margin to invest in the stock market.

First Layer – Leverage Using Credit Cards

The first layer of leverage is the $150,000 Mr H borrowed from the banks via advances on three credit cards.

Mr H “said he has a three to five-year horizon for his investments, and maintains he’s doing the maths to make sure he can always cover the interest, which ranges from 1.38% to 2.03% on the credit cards.”

I am theorizing that this is the best-case scenario where he can make his monthly payments regularly.

However, if things go south and Mr H for whatever reason and he cannot make payments on time, this is what may happen.

According to a report based on data of credit cards in Singapore made by ValueChampion, the average rate of credit cards Annual Percentage Rate (APR) is Singapore is 25%.

APR is the interest rate you will have to pay for borrowing money on your credit card and it compounds on a daily basis.

The 25% interest rate you see is just the tip of the iceberg.

Once you incur an unpaid balance at the end of your billing cycle, your debt can increase exponentially every single day you don’t pay off your balance.

Based on the three-year horizon Mr H stated, he would have incurred $64,703 of interest or 43% of his principle!

Second Layer – Margin

On top of the leverage, Mr H is opening up a share-financing or Margin account

Margin is debt or borrowed money brokerage firms or banks uses to invest in other financial instruments.

A margin account allows you to borrow money from a broker or bank for a fixed interest rate to purchase more stocks in anticipation of receiving considerably high returns.

Mr H stated that he is using the $150,000 he borrowed using his credit cards as collateral. The local bank then lent him a margin of $350,000 so that he has $500,000 to invest in the stock market.

We are adjusting the numbers and the margin as what Mr H stated isn’t what brokers would normally accept.

Here is why this is so risky.

Borrowed Cash: $150,000

Margin: $150,000

Purchasing Power: $300,000

Stock Value: $300,000

Say you were to purchase 3,000 shares of a stock valued at $100 per share giving you $300,000 of the company’s shares.

When the share price drops 20% to $240,000 with a non-actualised loss of $60,000. Normally, you will be able to wait it out.

However, in this hypothetical situation, you would be forced to make a bad decision by your broker because you are leveraged.

Borrowed Cash: $150,000

Margin: $150,000

Purchasing Power: $300,000

Stock Value: $240,000

Most brokerage accounts require that you keep a minimum margin percentage of 50%. Since the value of your stock portfolio has dropped the most you can have outstanding is down to $120,000.

As a result, the broker has every right to make what is called a margin call.

Margin calls are what occurs when a margin account funds drop because of a drop in the stock portfolio. They are a demand for more capital to meet the minimum maintenance margin.

Brokers can make the margin call and demand that you top up $30,000 in this case to meet the minimum maintenance margin of 50%.

Otherwise, they can force you to sell your stocks regardless of market price to meet the margin call.

This will take all the decision making out of your hands if you do not have the capital.

In this case for Mr H, he can either choose to borrow more money to top-up for the margin call or actualise the losses in his stock portfolio when the broker sells his stocks to make the margin call.

Since he does not even have any cash, things are going to get real bad real fast.

There you have it a breakdown of whether you should be borrowing to invest.

As much as leveraging to invest can bring about potentially higher returns, it can be very risky.

Proceed with caution.

Got any questions about investing? Our friendly Seedly Community is here to help! No need paiseh one…

Advertisement