We all know that life can be unpredictable.

Just a few years ago, we were all enjoying life as per usual, and then bam!

Covid engulfed the world.

Many businesses had to close down, nightlife ground to a complete halt, and once high-income pilots suddenly had zero income.

While it can be very tempting to jump straight into investing with your first paycheck, it might not be such a good idea when you don’t set aside an emergency fund for a rainy day.

Imagine this…

You were retrenched, and all your money is in investments.

But with the market in a sea of red, you would lose a part of your capital, maybe even all of it, if you were to sell them.

How are you going to feed yourself and pay your bills now?

That’s why it is so important for anyone starting out on their financial journey to have an emergency fund.

After you’ve cleared your debts if any.

TL;DR: Emergency Fund – How Much Should You Save & Where to Keep It

With life being full of twists and turns, one should set aside a sum of money for urgent and unplanned life events.

This sum of money should be equivalent to at least six months to 12 months of your living expenses,

And saved in ultra-low risk, high liquidity accounts such as:

- High-interest savings accounts

- Cash management accounts

- Insurance savings plans

- Singapore Savings Bond

Disclaimer: Do note that the information provided by Seedly serves as an educational piece and does not constitute an offer or solicitation to buy or sell any investment product(s). It does not consider the specific investment objectives, financial situation or particular needs of any person. Readers should always do their own due diligence and consider their financial goals before investing in any investment product(s).

What Is An Emergency Fund?

As defined by the Cambridge Dictionary, an emergency is

something dangerous or serious, such as an accident,

that happens suddenly or unexpectedly and needs fast action in order to avoid harmful results

The nature of an emergency means that you’ll be caught unprepared. Duh.

While sufficient insurance coverage can help you lighten the financial load in the event of major emergencies, such as disability or critical illness,

You’re still left vulnerable if you experience a sudden loss of income.

This is where an emergency fund comes in handy, as it will be your last line of defence (financially) to help cover your expenses in the meantime as you look for another job or recover from an accident.

How Much Should I Save in My Emergency Fund?

If you came looking for a magic number, you’d be sorely disappointed, as an emergency fund really depends on your lifestyle and situation.

That said, the general consensus is to have six months’ worth of living expenses.

But with things being so uncertain these days, I’d personally recommend at least six to twelve months’ worth to be extra safe, especially if you are a freelancer/gig worker, or have other dependents.

Call me kiasi (Hokkien: overly afraid) if you want.

Some individuals may even consider using their salary as the benchmark instead to ensure a sufficient pool of money.

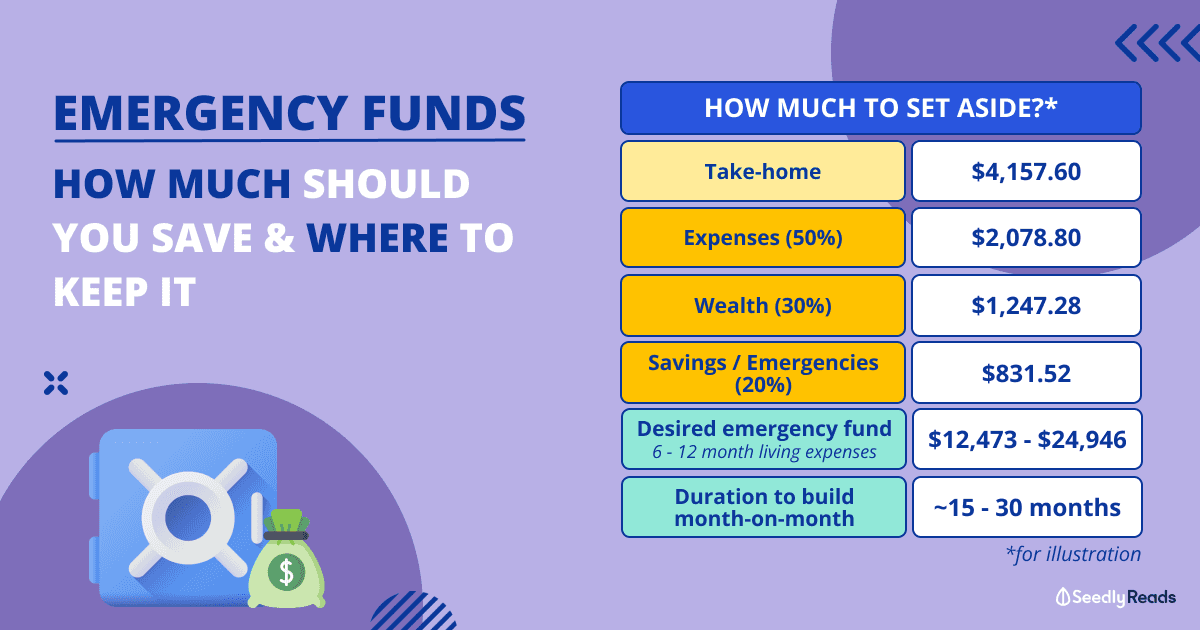

To start setting aside your emergency funds, you may use the 50/30/20 rule to allocate your monthly salary (after CPF deduction) and adjust based on your comfort level.

| What | Description |

| Expenses (50%) | For all essential and non-essential expenses |

| Wealth (30%) | For investments |

| Savings (20%) | For emergencies |

If possible, challenge yourself by allocating as much as possible towards your Savings and Wealth Accounts. Here’s an example.

Tom earns the 2023’s median income of $5,197 per month.

- Take-home after CPF deduction: $4,157.60

- Allocation of take-home salary:

- 50% for expenses: $2,078.80

- 30% for investments: $1,247.28

- 20% for savings and emergency funds: $831.52

- Therefore, the desired emergency fund is:

- Emergency Fund = 12 × Monthly Expenses = $

Given this salary and percentage allocation, Tom would need approximately 30 months to save enough to reach a 12-month emergency fund, assuming nothing will change in the next one to two years.

If Tom is married and may have a child soon, he may need to increase his savings for emergencies as there would be more expenses. This is a prudent step to ensure financial readiness for the upcoming changes.

Seek Professional Advice If You Need To

Before you start thinking about setting aside emergency, it’s also important to understand your current financial situation.

Find someone who can offer a piece of professional advice on your risk profile. This means finding a financial consultant or advisor who is an expert in this area.

Talk to a few of them, determine your needs, balance the recommendations of different consultants, and decide if you want to do it yourself.

In fact, Manulife is offering free consultations now! When you speak with a financial consultant, you stand a chance to win an iPhone 15 Pro, too!

Where Can I Keep My Emergency Fund?

Now that you know how much you need to set aside, here comes the bigger question:

Where should you keep your emergency funds?

Before we explore any products, there are two criteria for an emergency fund:

- They must be virtually risk-free or ultra-low-risk

- High liquidity with easy access to your funds

In layman’s terms, your money should be safe and able to be withdrawn quickly.

So here are your best options to keep your emergency funds in:

High-Interest Savings Account

Traditionally, a high-interest savings account with a bank would be where most people put their emergency funds.

This is because banks are virtually risk-free, and you can easily withdraw your cash with a debit card while enjoying interest of up to 3 per cent.

However, you’ll have to jump through several hoops in order to achieve such a high interest.

Cash Management Accounts

As of late, many cash management accounts, such as Syfe Cash+, Endowus Cash Smart and Grab Earn+ have popped up on the scene.

They offer attractive projected interest rates of up to 5 per cent, but most of them charge a management fee.

Unlike bank accounts, these cash management accounts are less liquid with withdrawal times up to a week and come with a slightly riskier but still low risk.

These accounts also have an investing element, as the funds you deposit into these accounts are invested into low-risk funds like cash funds, money market funds (MMF) and short-duration bond funds.

Insurance Savings Plan

Want something that helps you cover your back with insurance coverage and grow your funds?

Consider insurance savings plans such as Singlife or Singtel’s Dash PET, which are also ultra-low risk with high liquidity.

Plus, your deposits are insured by the SDIC and have a guaranteed surrender value at the point of failure that is capped at $100,000.

You can spend directly from these accounts as they combine a regular savings plan, insurance protection, and a traditional bank account.

Singapore Savings Bond

Lastly, we have the Singapore Savings Bond (SSB), which is fully backed by the Singapore government, making it virtually risk-free.

While SSB rates are currently very attractive, the big downside is that it offers the least liquidity out of all the options listed, taking up to 30 days to withdraw, depending on when you make your redemption request.

If you’re wondering why I did not list fixed deposits, I’d argue that fixed deposits are not liquid enough to be considered a place to park all your emergency funds.

I mean, that’s why they have ‘fixed’ in their names.

So, Where Should I Park My Emergency Funds?

Again, this largely depends on your personal preference but remember the two criteria that I mentioned earlier.

Your emergency funds need to be ultra-low risk with high liquidity.

At the baseline, a high-interest savings account is something most of us would already have, so if you’re just starting out, this would be a fuss-free place to park your hard-earned money.

However, it is good to make this account separate from your transactions account as this is your “in case of emergency, break glass” money.

For those of us who want to grow our emergency funds as well to combat inflation, you may consider a combination of the above products.

Personally, I use a mix of a high-interest savings account and a cash management account for my emergency funds.

This allows me to have immediate access to funds via my debit card while letting me grow my emergency funds at a slightly higher rate in a cash management account or withdraw more if need be.

Need a second opinion?

Feel free to ask your questions on the Seedly Community about managing your emergency funds!

Advertisement