Best Personal Loan Rates in Singapore (2024): For Your Life Emergencies

Joel Koh

Joel Koh●

Life has a way of throwing curveballs, from unexpected medical bills to dream projects waiting to be realised.

When the hurdles seem a bit too high or the aspirations a tad out of reach, a personal loan becomes more than just borrowed funds; it’s a helping hand, enabling you to overcome challenges and embrace opportunities.

Whether it’s turning a house into a home or investing in personal growth, a personal loan can be the bridge that turns dreams into reality, making the journey uniquely yours.

As with any loan, a personal loan comes with an interest rate, processing fee, minimum repayment fee and loan tenure.

Although the application process is quite straightforward, there are quite a few things you need to carefully consider when you want to find the best personal loans for you.

TL;DR: Personal Loan Promotions And Comparison in Singapore (2024)

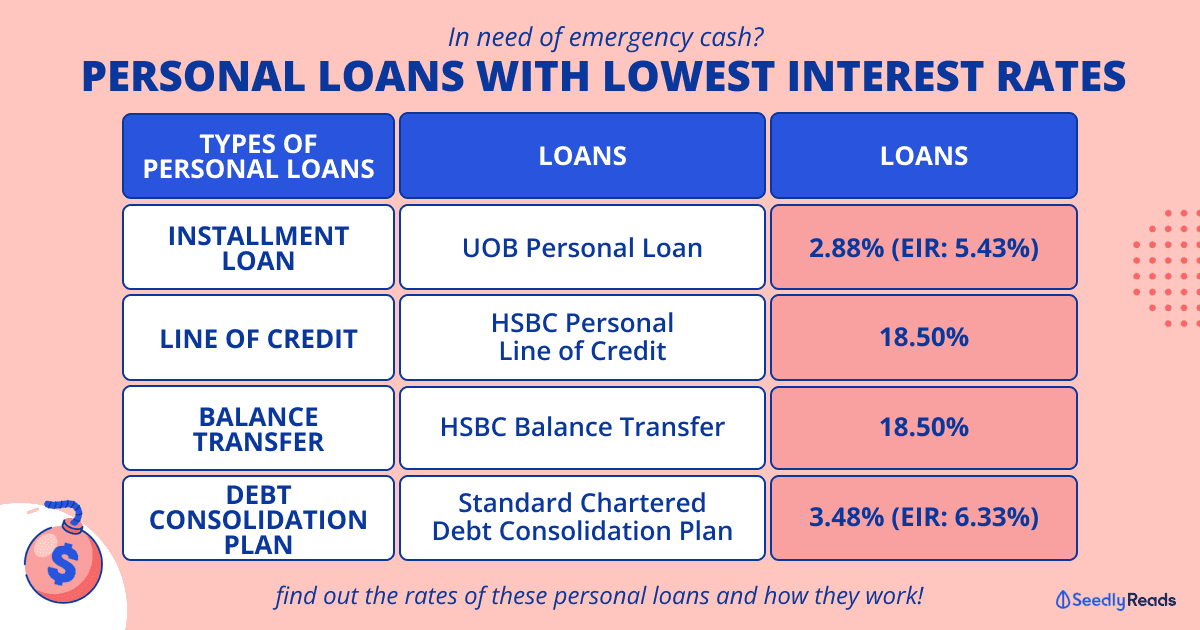

Lowest Personal Loan Rates

For the benefit of those looking for the lowest loan rates (although this shouldn’t be the only thing you’re looking at), here’s what you need to know:

| Personal Instalment Loans | Effective Interest rate (% p.a.) | Highest Loan Amount | Promotion |

|---|---|---|---|

| UOB Personal Loan Apply Now | 2.88% (EIR: 5.43%) | Up to 2X monthly income or S$200,000, whichever is lower | Get up to Cash Rebate up to 2% for loan amount of S$15,000 and above with minimum tenor of 36 months |

| GXS FlexiLoan Apply Now | 2.99% (EIR: 5.65%) | Up to $100,000 | Stand a chance to win 888,888 GrabRewards points (30 lucky winners) with you apply for a FlexiLoan of minimum $5,000 with at least 6-month tenure |

| Standard Chartered CashOne Personal Loan Apply Now | 2.88% (EIR: 5.84%) | Up to 4X monthly income | Get up to $5,188 cashback when you apply for a loan amount of $10,000 and above, at an interest rate of 3.48% and above, and tenure of 3, 4, or 5 years. |

| Line of Credit | Prevailing Interest rate (% p.a.) | Highest Loan Amount | Promotion |

| HSBC Personal Line of Credit | HSBC Premier customers: 12% p.a. HSBC Advance, Visa Platinum, or Revolution credit card customers: 16.5% p.a. All other customers: 18.5% p.a. | Annual income of S$120,000 and above: Up to 6 times monthly income Annual income of S$30,000 and less than S$120,000: Up to 4 times monthly income | Get up to $3,000 cashback |

| Maybank CreditAble | 19.80% | Up to 4X monthly income | |

| DBS Cashline Loan | Annual Income ≥ $30,000: 22.90% Annual Income < $30,000: 29.80% | Up to 10X monthly income, with annual income of S$120,000 and above | - |

| OCBC EasiCredit Personal Loan | 22.90% - 29.80% depending on your income | Up to 2x monthly income if your annual income is S$20,000 - S$29,999 Up to 4x monthly income if your annual income is S$30,000 - S$119,999 Up to 6x monthly income if your annual income is S$120,000 and above | - |

| Balance Transfer / Credit Card Funds Transfer Note: Interest is payable at 18 - 29% p.a. with credit cards or line of credit | Prevailing Interest Rate (% p.a.) | One-time processing fee | Promotion |

| Citibank Balance Transfer - New customers | 20.95% | New Citibank credit card holders: 1.58% (EIR 3.65% p.a.) New Citibank Readt Credit holders: 1.58% (EIR 3.60% p.a.) | Enjoy 0% p.a. interest for 6 months with no fee (EIR 0% p.a.) or 2.99% p.a. interest for 24 months with no fee (EIR 2.99% p.a.) |

| HSBC Balance Transfer | 18.50% | Loan amount ≥ S$10,000: 1.50% (EIR: 3.26%) Loan amount < S$10,000: 2.50% (EIR: 5.47%) | Enjoy a waiver of processing fee for approved amount of S$10,000 and above. |

| Maybank Fund Transfer for CreditAble Customers | 20.90% | 6 months: 2.28% (EIR: 4.87%) 12 months: 4.38% (EIR: 5.06%) | Processing Fee of 1% waived for online application |

| Debt Consolidation Plan | Interest rate (% p.a.) | Fixed monthly repayment | Promotion |

| Bank of China Debt Consolidation Plan | 3.83% (EIR: 7.48%) | Up to 10 years | - |

| DBS/POSB Debt Consolidation Plan | 3.58% (EIR: 6.56%) | Up to 8 years | - |

| Standard Chartered Debt Consolidation Plan | 3.48% (EIR: 6.33%) | Up to 10 years | Get up to S$500 Cashback when you apply |

Click here to jump:

- What to know about personal loans

- Personal Instalment Loans

- Line of Credit / Overdraft Facility

- Balance Transfer / Funds Transfer

- Debt Consolidation Plan

- Other types of personal loans

Disclaimer: All rates are as of 16 Jan 2024 and may be subject to changes. Please check with the respective banks for updated information. The information provided by Seedly serves as an educational piece and is not intended to be personalised financial advice. Readers should always do their own due diligence and consider their financial goals before committing to any financial product and consult their financial advisor before making any decisions.

Things to Pay For Personal Loans

Besides paying for how much you’re borrowing, there are applicable fees you possibly will need to pay for:

| Interest rate: | Effective Interest Rate (EIR): |

| Banks typically give you a customised interest rate that you’ll see only after an approved application, as each situation is unique. Your credit score, income, and repayment history will determine your final loan interest rate. You will likely get a better rate if you have a good track record. | The EIR is a more accurate reflection of the cost of borrowing because it also considers other factors, such as the processing fee and loan repayment schedule. While a loan might have a lower interest rate, if it has a a higher EIR could mean that there are additional fees and charges imposed, and you might end up paying more. Basically, the higher this is, the more likely you need to pay more overtime. |

| Processing/Administrative fees: | Early Repayment Penalty: |

| These usually range from $0 to 3% of the loan amount borrowed and are deducted from the loan amount borrowed. E.g., your loan amount is $30,000, and it comes with a 2% processing fee, which means that the amount disbursed to you will be $29,400. Banks will occasionally waive the processing fee and offer promotional interest rates. | These loans usually come with an early repayment penalty. |

Then again, some banks will have promotional offers where you don’t have to pay for interest during the tenure period, so it really depends on your loan and the bank you opt for.

Types of Personal Loans

Next up, you need to familiarise yourself with the types of personal loans:

| Where to get Loans | Types of Loans | Application Requirements | Key Considerations | Suitable Profiles |

|---|---|---|---|---|

| Banks | Personal instalment loans | Singaporeans/Permanent Residents - Must be ages 21 and 65 years old. - You will need to be earning at least $20,000 a year. - If you earn between $20,000 and $30,000, the interest rates you will be paying will be higher than those who make more than $30,000 a year. Foreigners You will need to be earning between $40,000 and S$60,000 a year depending on the lender. You will also need an Employment Pass with at least 12 months of validity | - Interest is fixed, between 3.7% to 4.5% - Interest kickstarts immediately once you receive it, regardless of when you use the money. - Early repayment penalty | Those who require funds for unexpected or significant expenses, e.g., medical emergencies, weddings, funerals, divorces; usually for short-term purposes |

| Line of credit | Borrowers are required to open a line of credit with the borrower. | - Interest averaging between 18.5% p.a. and 20.95% p.a. depending on the credit facility - Credit line may be secured/unsecured - Open-ended, flexible schedule of repayment - No early repayment penalty - An ongoing annual fee that renews every year | Those who face unforeseen inconsistencies in salaries or for businesses that meet cash flow crunches and situations where there might be repeated cash outlays | |

| Balance transfer | Borrowers are required to own a credit card. | High interest kicks in after a grace period of 3 - 12 months | Those with a small amount of credit card or personal loan. Confident that they can repay over a few months as they have already had a repayment plan designed for the grace period. | |

| Debt consolidation plan | Only available to Singaporeans and Permanent Residents with the following criteria: - Must be a salaried employee with an annual income between S$30,000 and S$120,000. - Must have outstanding interest-bearing balances on unsecured credit facilities amounting to a minimum of 12 times your monthly income. | This plan is only for unsecured credit facilities like credit cards, personal loans (excluding education, renovation, medical, and business credit lines) You can only have one plan active at any one time. After three months, you can refinance your existing plan with another participating bank if you find one with lower interest rates. You cannot apply for a new credit card or loan until your outstanding debt is less than 8 times your monthly salary. You will be charged a late fee and interest if you miss a payment. | Those with a large amount of credit card bills or personal loans. They can only repay over a few years. | |

| Moneylenders (Licensed) | Personal instalment loans | Almost no requirements, but a licensed moneylender is legally allowed to loan you up to $3,000 if your annual income is less than $20,000 | Rumour has it that it is possible to incur an interest rate up to 30%. | Those with emergencies that require small amounts, such as a few hundred bucks to just $1,500. |

| Credit Unions | - Personal instalment loan - Marriage loan - Education loan - Renovation loan - Consolidating loan | - You need to be a Member of the Union. - You need to show that you can repay the loan and how you use the funds. | An alternative to banks and moneylenders | Those who require funds for unexpected or significant expenses, e.g., medical emergencies, weddings, funerals, divorces; usually for short-term purposes |

Best Bank for a Personal Loan

This is the most straightforward loan, which offers you a sum of cash upfront, and you will need to pay back the amount in instalments over a tenure. Four main factors you should consider before taking up a personal loan from a bank.

- How it works: Once you have submitted your application with the amount you intend to borrow, you will make an upfront one-time processing fee and commit to repaying the total amount via fixed equal monthly instalments that can stretch up to 60 months. The interest and fees you will have to pay are first calculated and computed in the total loan amount. You can also get your bank to waive the processing/administrative fee.

- Loan Tenure: 1 – 7 years

- Reason(s) for taking up this loan: This loan is suitable for the purchase of big-ticket items or expenses that you cannot pay all at once

- Early Repayment Penalty: Yes

Example: One of your relatives met an unexpected medical emergency that requires complicated surgery. They have not been insured under a Health Insurance Plan, which can help cover the medical expenses incurred. The medical bill totals up to $10,000, and your relative’s family can take up a personal instalment loan and slowly repay it over a longer timeframe.

CIMB Cashlite

| Effective Interest Rate (% p.a.) | Highest Loan Amount | Promotion |

| 3.38% (EIR: 6.32%) |

Up to 8X monthly income | Get up to $2,000 cashback |

Apply Now

Citibank Quick Cash Loan

| Effective Interest Rate (% p.a.) | Highest Loan Amount | Promotion |

| 3.45% (EIR: 6.50%) |

Up to 4X monthly income | Get up to $600 GrabGifts voucher |

DBS/POSB Personal Loan

| Effective Interest Rate (% p.a.) | Highest Loan Amount | Promotion |

| 3.88% (EIR: 7.56%) |

Up to 10X monthly income | – |

Apply Now

GXS FlexiLoan

GXS is a relatively new contender in the personal loan space, given that digital banks are still in their nascent period. The GXS FlexiLoan is an unsecured loan that does not have an early repayment penalty, annual fee, processing fee, or late payment fee. However, it does charge late interest upon late repayment.

| Effective Interest Rate (% p.a.) | Highest Loan Amount | Promotion |

| 2.99% (EIR: 5.65%) |

Up to $100,000 | Stand a chance to win 888,888 GrabRewards points (30 lucky winners) with you apply for a FlexiLoan of minimum $5,000 with at least 6-month tenure |

Apply Now

HSBC Personal Loan

| Effective Interest Rate (% p.a.) | Highest Loan Amount | Promotion |

| 3.60% (EIR 6.50%)Existing Premier Customers: 3.00% (EIR: 5.50%) |

Up to 8X monthly income | Get up to $3,000 cashback |

Apply Now

Maybank CreditAble Term Loan

| Effective Interest Rate (% p.a.) | Highest Loan Amount | Promotion |

| 3.28% (EIR 6.00%) |

Up to 4X monthly income | Apply for a CreditAble account and charge to your Credit Card and/or withdraw from your CreditAble Account a minimum of S$600 for each of the first two consecutive months upon approval and receive a pair of American Tourister Linex 66/24 Luggage TSA, or an AirPods (3rd generation) with Lightning Charging Case, or S$200 cashback. |

OCBC EasiCredit Personal Loan

| Effective Interest rate (% p.a.) | Highest Loan Amount | Promotion |

| 3.80% (EIR 7.49%) |

Up to 6X monthly income | – |

Standard Chartered CashOne Personal Loan

| Effective Interest Rate (% p.a.) | Highest Loan Amount | Promotion |

| 2.88% (EIR: 5.84%) |

Up to 4X monthly income | Get up to $5,188 cashback when you apply for a loan amount of $10,000 and above, at an interest rate of 3.48% and above, and tenure of 3, 4, or 5 years. |

Apply Now

UOB CashPlus Loan

| Effective Interest Rate (% p.a.) | Highest Loan Amount | Promotion |

| 3.40% (EIR: 6.22%) |

Up to 4X monthly income Up to 6X (Capped at S$200,000) if your annual income is S$120,000 and above |

– |

UOB Personal Loan

| Effective Interest Rate (% p.a.) | Highest Loan Amount | Promotion |

| 2.88% (EIR: 5.43%) |

Up to 2X monthly income or S$200,000, whichever is lower | Get up to Cash Rebate of up to 2% for a loan amounts of S$15,000 and above with a minimum tenor of 36 months |

Apply Now

Personal Loan: Line of Credit

Sometimes known as an Overdraft Facility, it is an established arrangement between the bank and clients which determines the maximum loan amount the customer can borrow.

Once the application is approved, the borrower can access funds from the line of credit at any time, as long as they do not exceed the maximum amount set in the agreement.

With that being said, banks often charge fees for opening a credit line and annual fees to maintain your credit line account.

- How it works: Start applying via your bank, and once it is approved, you can withdraw the funds via mobile/internet banking, physical branch, cheque or ATM. You will be charged daily the moment you start withdrawing your funds. It is good to note that you stop paying the interest once you repay the loan amount.

- Additional Fees/Interests: There are two layers of interest. Firstly, you will need to open a line of credit, which comes with an annual fee. Second, the interest rates on the amount you borrow range from 18.60% to 22.00%.

- Loan Amount: Banks typically offer up to 2-6 times your monthly salary.

- Loan Tenure: Flexible. You decide how long the loan tenure will be, but do note that you will be paying interest on it until the day you repay.

- Reason(s) for taking up this loan: This loan is suitable for purchasing big-ticket items or expenses that you cannot pay all at once or when you face unexpected situations where cash is not immediately available. This allows you to withdraw the money without processing it except for the initial application.

- Early Repayment Penalty: These loans do not have an early repayment penalty.

Example: As a small business owner, you may not have sufficient cash flow to free up the purchase of operational supplies during peak periods. Once sales are settled, you can quickly repay the amount owed to the bank. This may be the most suitable for those who foresee needing to borrow cash multiple times throughout the year.

These are what banks are offering:

| Line of Credit | Prevailing Interest rate (% p.a.) | Highest Loan Amount | Promotion |

|---|---|---|---|

| Citibank Ready Credit | 22.95% | Up to 4X your monthly income or up to 8X your monthly income if your annual income is S$120,000 and above | |

| DBS Cashline Loan | Annual Income ≥ $30,000: 22.90% Annual Income < $30,000: 29.80% | Up to 10X monthly income, with annual income of S$120,000 and above | - |

| HSBC Personal Line of Credit | HSBC Premier customers: 12% p.a. HSBC Advance, Visa Platinum, or Revolution credit card customers: 16.5% p.a. All other customers: 18.5% p.a. | Annual income of S$120,000 and above: Up to 6 times monthly income Annual income of S$30,000 and less than S$120,000: Up to 4 times monthly income | Get up to $3,000 cashback |

| Maybank CreditAble | 19.80% | Up to 4X monthly income | |

| OCBC EasiCredit Personal Loan | 22.90% - 29.80% depending on your income | Up to 2x monthly income if your annual income is S$20,000 - S$29,999 Up to 4x monthly income if your annual income is S$30,000 - S$119,999 Up to 6x monthly income if your annual income is S$120,000 and above | - |

| UOB CashPlus Credit | 29.98% | Up to 6X (Capped at S$200,000) if your annual income is S$120,000 and above | - |

Personal Loan: Balance Transfer / Funds Transfer

A Balance Transfer or Funds Transfer is a type of unsecured, short-term loan that uses the available credits on your credit card.

It can be a strategic move for individuals looking to manage their debt more effectively. It can help save money on interest payments, especially if the new credit card offers a lower interest rate or a promotional period with no interest.

It transfers your outstanding balance from credit cards to a 0% or low-interest account, commonly offered on a credit card over a grace period, usually from three to 18 months.

his is most often used to reduce interest payments and help consolidate multiple credit debts into one place. Generally, you are not required to pay any interest if you manage to pay off all credit card balances before your grace period.

- How stuff works: Once you submit an application for Balance Transfer on your credit card, you will pay a one-time processing fee on the amount you borrowed. Afterwards, you will enjoy a low to 0% interest rate over the grace period. You will be charged interest ranging from 18% to 29% when the grace period has ended, depending on the credit card. There is usually a minimum repayment you need to commit to.

- Additional Fees: You will also be charged a one-time processing fee, typically ranging from 1% to 5%, depending on your credit card company. Occasionally, some credit cards will offer up promotions when this is waived.

- Loan Amount: The amount you can loan is based on your credit card limit. Banks usually require a minimum loan amount but can offer up to 10 times your monthly salary if you have a high monthly income and a good credit score.

- Loan Tenure: 3 to 12 months grace period until the high-interest rates kick in based on the initial interest rate of all your credit cards.

- Reason(s) for taking up this loan: This particular type of loan allows you to transfer any outstanding loans you already have into one place. Balance transfer loans are a great way to consolidate your debt into a more manageable account with fixed monthly repayments you can budget for. Do look out for promotions where banks will waive the processing fee via cashback or incentives.

- Early Repayment Penalty: These loans do not have an early repayment penalty.

Example: *Choy, touchwood* You might have racked up $20,000 in credit card debts spread over many credit cards as you could not keep up with your expenses tracking. Rather than paying the total 20-25% interest rates on all those credit cards, you can apply for the Balance Transfer to focus your repayment on one. The 6 to 12-month grace period will give you time to think. Make your best effort to pay back the debt as soon as possible and develop a repayment plan.

To avoid the example above, you can read the Seedly Money Framework for 2022 & Beyond!

| Balance Transfer / Credit Card Funds Transfer Note: Interest is payable at 18 - 29% p.a. with credit cards or line of credit | Prevailing Interest Rate (% p.a.) | One-time processing fee | Promotion |

|---|---|---|---|

| Citibank Balance Transfer - New customers | 20.95% | New Citibank credit card holders: 1.58% (EIR 3.65% p.a.) New Citibank Readt Credit holders: 1.58% (EIR 3.60% p.a.) | Enjoy 0% p.a. interest for 6 months with no fee (EIR 0% p.a.) or 2.99% p.a. interest for 24 months with no fee (EIR 2.99% p.a.) |

| DBS/POSB Balance Transfer | 25.90% | 3 months: 1.80% 6 months: 2.50% 12 months: 4.50% | - |

| HSBC Balance Transfer | 18.50% | Loan amount ≥ S$10,000: 1.50% (EIR: 3.26%) Loan amount < S$10,000: 2.50% (EIR: 5.47%) | Enjoy a waiver of processing fee for approved amount of S$10,000 and above. |

| Maybank Credit Card Fund Transfer | 28.50% | 6 months: 2.28% (EIR: 4.87%) 12 months: 4.38% (EIR: 5.06%) | - |

| Maybank Fund Transfer for CreditAble Customers | 20.90% | 6 months: 2.28% (EIR: 4.87%) 12 months: 4.38% (EIR: 5.06%) | Processing Fee of 1% waived for online application |

| OCBC Balance Transfer | 26.00% | 4.00% | Apply online and get $18 cashback (no minimum loan amount) |

| Standard Chartered Credit Card Funds Transfer | 29.90% | From 0.99% (EIR: 4.01%) for 3-month tenure | Enjoy 0% interest rate for 6, 9 or 12 months with processing fee of only 1.65%, 2.5% or 4.5% of approved loan amount respectively (EIR from 3.26%) |

| UOB CashPlus Funds Transfer | 29.98% | Zero processing fee | 0% interest for online application |

| UOB Credit Card Balance Transfer | 25.00% | 3 months: 1.49% (EIR: 6.11%) 6 months: 2.50% (EIR: 5.34%) 12 months: 4.28% (EIR: 4.95%) | Get unlimited cash rebate of up to 0.50% |

Personal Loan: Debt Consolidation Plan

A Debt Consolidation Plan is an instalment loan used to pay off your personal debt.

Yup, a plan to combine all your credit card debts and personal loans into one loan with a lower interest rate. This is often to manage and eliminate your debt over several years and is sometimes termed the Debt Restructuring Programme. This may sound similar to the Balance Transfer, but there is a criterion — the borrower’s debt must exceed 12 times their monthly salary.

Do note that debt consolidation loans usually come with a one-time processing fee, a flat interest rate, and a 1 to 10-year tenure!

- How it works: Once you have submitted your application, the bank to which you have submitted your application will combine all the loans into a single loan by buying out all your outstanding balances, fees and charges. After that, you will then make monthly repayments to the said bank over a few years until your debt is cleared.

The essence is finding a plan of low interest and fees while keeping your monthly payment at a reasonable level.

While you look for the best loan that works for you, remember to look for promotions that may give you interest-free periods. Don’t be afraid to ask for a waiver of your annual fees!

| Debt Consolidation Plan | Interest rate (% p.a.) | Fixed monthly repayment | Promotion |

|---|---|---|---|

| Bank of China Debt Consolidation Plan | 3.83% (EIR: 7.48%) | Up to 10 years | - |

| Citi Debt Consolidation Plan | 3.99% (EIR: 7.50%) | Up to 7 years | - |

| DBS/POSB Debt Consolidation Plan | 3.58% (EIR: 6.56%) | Up to 8 years | - |

| HSBC Debt Consolidation Plan | 4.20% - 7.90% (EIR: 7.50% - 13.00%) | Up to 10 years | Get up to 5% cashback when you apply |

| Standard Chartered Debt Consolidation Plan | 3.48% (EIR: 6.33%) | Up to 10 years | Get up to S$500 Cashback when you apply |

| UOB Debt Consolidation Plan | 1 - 6 years: 4.50% (EIR: 8.22%) 7 - 8 years: 5.50% (EIR: 9.67%) | Up to 8 years | - |

Licensed Moneylenders

Alternatively, you can borrow money from Licensed Moneylenders.

‘Licensed’ says that these moneylenders are legal entities that operate within the Moneylenders Act and Rules.

These moneylenders are certainly not the typical Ah-Longs you know who spray O$P$ on walls! They are restricted by law on the amount they can lend, the fees they charge and the acceptable interest rate.

One Seedly contributor has rightfully pointed out the differences between borrowing from a moneylender versus a bank, and you can read it here.

Compared to borrowing from banks, licensed moneylenders operate as small businesses and loan out small amounts that are pegged to your income – up to $3,000 if your annual income is less than $20,000.

Otherwise, they can loan you up to six times your monthly payment. With fewer processes, borrowing from licensed moneylenders may be faster, and there may be fewer restrictions on citizenship and income.

HOWEVER, moneylenders could potentially charge you up to 30% of the interest rate even though the Government’s guidelines have a cap on the monthly interest rate as they may not abide by the guidelines set or have other hidden fees.

Hence, always do your due diligence to check and enquire for the details so that you stay on top of your finances!

Based on guidelines set by the Ministry of Law, a licensed moneylender is only permitted to impose the following charges, interests and expenses:

- The monthly interest rate is capped at 4%;

- The monthly late interest rate is capped at 4% for each late repayment, and the late interest can only be charged on an amount that is repaid late;

- A late fee of not more than S$60 per month;

- A fee not exceeding 10% of the principal of the loan when a loan is granted;

- Legal costs ordered by the court for a successful claim by the moneylender for the recovery of the loan;

- An administrative fee that must not exceed 10% of the principal loan granted;

- The total cost charged by a legal lender, including interest, late interest, administrative fees, late fees, and other related charges, must not exceed the principal loan amount.

Loans From Credit Unions

The lesser-known sibling of banks and moneylenders, a Credit Union is a non-profit money cooperative whose members can borrow from pooled deposits at low-interest rates.

Credit Unions, sometimes termed “Credit Co-operatives” or “Credit Co-ops”, are financial institutions created and operated by their members, who pool their resources to help one another. Unlike commercial banks, a credit co-op is not for profit, and it aims to provide access to affordable financial solutions for its members, who are also its collective owners.

Nonetheless, with Co-op being an exclusive initiative, there are things you need to know:

- You need to be a Member of the Union to start borrowing

- You need to show that you can repay the loan and how you use the funds

Some notable names include TCC Credit Co-operative and Straits Times Co-op.

So, is a Personal Loan for you?

While most of us really wish that we don’t have to resort to taking up personal loans to finance certain aspects of life, it can become inevitable, especially when heavily cash-strapped. As such, these are some essential considerations should the situation arise.

When in doubt, you can always head over to our friendly Seedly Community to ask for opinions and advice!

Related Articles:

Advertisement