Best Renovation Loan in Singapore (2026): The First-Time Homeowner Guide

Seedly

Seedly●

Whether you’re renovating your Build-to-Order (BTO), or your newly-bought resale flat,

renovation can easily become one of the biggest cash expenses you’ll face as a homeowner.

And let’s be honest: your renovation budget is rarely the only thing competing for your cash. You may also be paying for your wedding, furniture, appliances, moving costs, and emergency savings.

That’s where a home renovation loan Singapore homeowners commonly compare can help. It lets you spread out your renovation cost over a few years, instead of paying everything upfront.

But like any loan, it also comes with interest, fees, and monthly repayments. So before you apply for a house renovation loan, here’s what you need to know.

TL;DR: Best Renovation Loans in Singapore (2023)

Teleport here:

- How do renovation loans work in Singapore?

- How much renovation loan can I get in Singapore?

- Which bank is best for a renovation loan?

- Should you take a renovation loan?

In this renovation loan Singapore guide, we’ll walk through how renovation loans work, what they can be used for, and what to compare before applying.

A renovation loan is usually meant for renovation-related works only. In Singapore, banks commonly cap renovation loans at S$30,000 or six times your monthly income, whichever is lower, subject to approval. For example, DBS states that borrowers may borrow up to six times their monthly income or S$30,000, whichever is lower. Maybank also states that its renovation loan amount is up to six times monthly income or S$30,000, whichever is lower.

You also cannot use CPF savings to pay for renovation, improvement, or repair works.

Important note: This article avoids using promotional interest rates that may expire before July. Always check the bank’s official page again before applying, as rates and fees can change.

Disclaimer: The information provided by Seedly serves as an educational piece and is not intended to be personalised financial advice. Always do your own due diligence, consider your financial goals before committing to any financial product, and consult a qualified financial adviser if needed.

How Do Renovation Loans Work in Singapore?

As the name suggests, renovation loans are meant to finance renovation-related works for your home.

They are different from home loans. A home loan helps you finance the purchase of your property, while a renovation loan helps you pay for renovation works after you have bought or secured the home.

A renovation loan is also different from a personal loan. Personal loans usually give you more flexibility in how you use the funds, while renovation loans are more restricted. For example, banks may require you to submit a renovation invoice or quotation to show that the loan is being used for renovation works. DBS states that a renovation invoice or quotation is required for its renovation loan application.

The money may also not be disbursed directly into your personal bank account. DBS states that approved loan amounts are disbursed in cashier’s orders, and the cashier’s orders are issued under the appointed renovation contractor’s name.

This means a renovation loan may not be suitable if you want to use the money freely for furniture, appliances, or other non-renovation purchases.

A typical renovation loan tenure is up to five years, depending on the bank and your application. DBS and Maybank both state a renovation loan tenure of up to five years.

When comparing renovation loans, don’t just look at the interest rate. Also check:

- Processing, handling, or admin fees

- Insurance premiums, if any

- Late payment fees

- Prepayment or early redemption fees

- Cancellation fees

- Cashier’s order fees

- Whether the loan is paid directly to your contractor

- Whether the bank requires post-disbursement checks

For example, DBS currently lists a 2% handling fee and 1% insurance premium for its renovation loan. Maybank lists a 2% processing fee, minimum S$200, while CIMB lists a 1.55% processing fee for CIMB Renovation-i Financing.

What Can Renovation Loans Be Used to Pay For?

Renovation loans can usually be used for renovation-related works, but the exact list depends on the bank.

Using DBS as an example, its renovation loan can be used for:

| Usage of Renovation Loans |

|---|

| Electrical and Wiring |

| Built-in Cabinets |

| Painting & Redecorating Works |

| Structural Alterations |

| External Works Within Compound of the House |

| Flooring and Tiling |

| Basic Bathroom Fittings |

| Installation of solar panels |

How Much Money Do You Need For Renovation?

There is no one-size-fits-all answer.

Your renovation budget depends on your flat type, whether it is a BTO or resale flat, the condition of the unit, how much carpentry you want, and whether you are going for a simple or highly customized design.

Before speaking to banks, start by separating your renovation budget into three buckets:

| Budget Bucket | What goes inside |

|---|---|

| Must-haves | Electrical works, plumbing, flooring, kitchen, bathroom works, safety-related fixes |

| Nice-to-haves | Feature walls, extra carpentry, upgraded finishes, smart home features |

| Non-renovation costs | Furniture, appliances, curtains, décor, moving costs |

This matters because a renovation loan may not cover every item in your home setup.

1) Buying To Sell

If you plan to sell the flat in a few years, you may not want to spend too much on highly customised renovation.

That doesn’t mean you should do the bare minimum. The home still needs to be comfortable and functional. But you may want to avoid overly personal design choices that future buyers may not appreciate.

For BTO buyers, one option to consider is HDB’s Optional Component Scheme (OCS).

Searching for an HDB renovation loan Singapore option? It’s worth knowing that HDB’s OCS is not a renovation loan. Instead, HDB describes OCS as a flexible, opt-in scheme that gives you the added convenience of having your home closer to move-in condition when you collect your keys.

The actual OCS items and costs vary by project, so check the specific HDB sales brochure for your launch before deciding whether to opt in.

The upside is convenience. The downside is that you may later decide to overlay, replace, or customize the finishes, which can add to your renovation cost.

2) Buying Your Forever Home

If you are renovating what you see as your long-term home, you may be more willing to spend on comfort, durability, and design.

That can be reasonable, but the key is to spend intentionally.

Focus first on things that affect your daily life, such as:

- Kitchen layout

- Storage

- Lighting

- Electrical points

- Bathroom usability

- Flooring

- Ventilation

- Maintenance needs

It is very easy to get carried away during renovation planning. A few upgrades here and there can quickly turn into a much larger bill.

So before committing, ask yourself:

- Will I still value this upgrade five years from now?

- Is this a need or a nice-to-have?

- Can I afford the monthly repayment comfortably?

- Do I still have enough emergency savings after moving in?

A home should improve your quality of life, not leave you financially stretched.

How Much Renovation Loan Can You Get?

The maximum renovation loan amount is generally S$30,000 or six times your monthly income, whichever is lower, subject to the bank’s approval.

For example, DBS states that you may borrow up to six times your monthly income or S$30,000, whichever is lower, subject to credit eligibility. Maybank’s personal loans page also states that its renovation loan amount is up to six times monthly income or S$30,000, whichever is lower.

So if your renovation budget is S$45,000 and your approved renovation loan is capped at S$30,000, you still need to fund the remaining S$15,000 using cash or another financing option.

Be careful about stacking multiple loans. Even if you qualify for them, more monthly repayments can affect your cash flow.

If you plan to buy another property later, your existing debt obligations can also matter. MAS states that the Total Debt Servicing Ratio (TDSR) threshold for property loans is set at a maximum of 55% of the borrower’s monthly income.

Can You Use CPF to Repay Renovation Loan?

No. You cannot use CPF savings to repay a renovation loan.

CPF states that CPF savings cannot be used for renovation, improvement, or repair works for your property.

This means your renovation cost must be paid using cash, a renovation loan, or another form of financing.

You can use CPF for approved housing-related purposes, such as eligible property purchases and housing loan repayments, subject to CPF rules. But renovation is not one of the permitted uses.

CPF savings can also be invested under the CPF Investment Scheme if you meet the eligibility criteria, but that is separate from using CPF to pay for renovation. CPF states that eligible members can invest their OA and SA savings under CPFIS, subject to criteria such as age, account balances, and completion of the Self-Awareness Questionnaire where applicable.

Read more:

- The Ultimate List of Interior Designers To Avoid In Singapore

- Getting Your First Property In Singapore: We Answer 10 Commonly Asked Questions

- Renovation Shopping Hacks: Based On Real Community Reviews

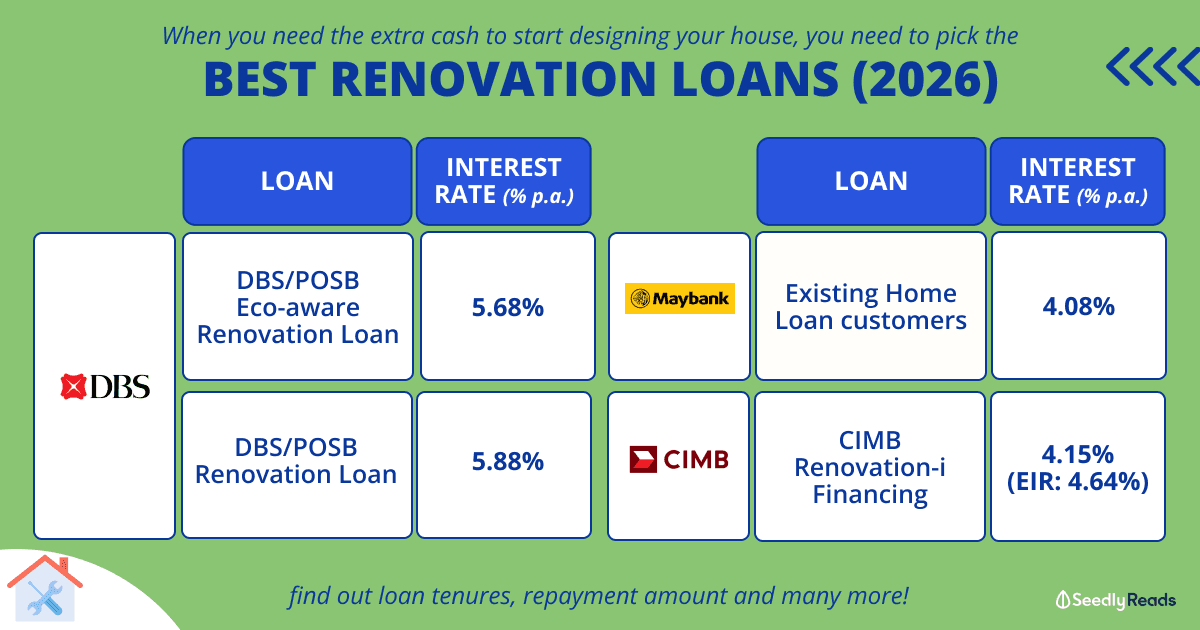

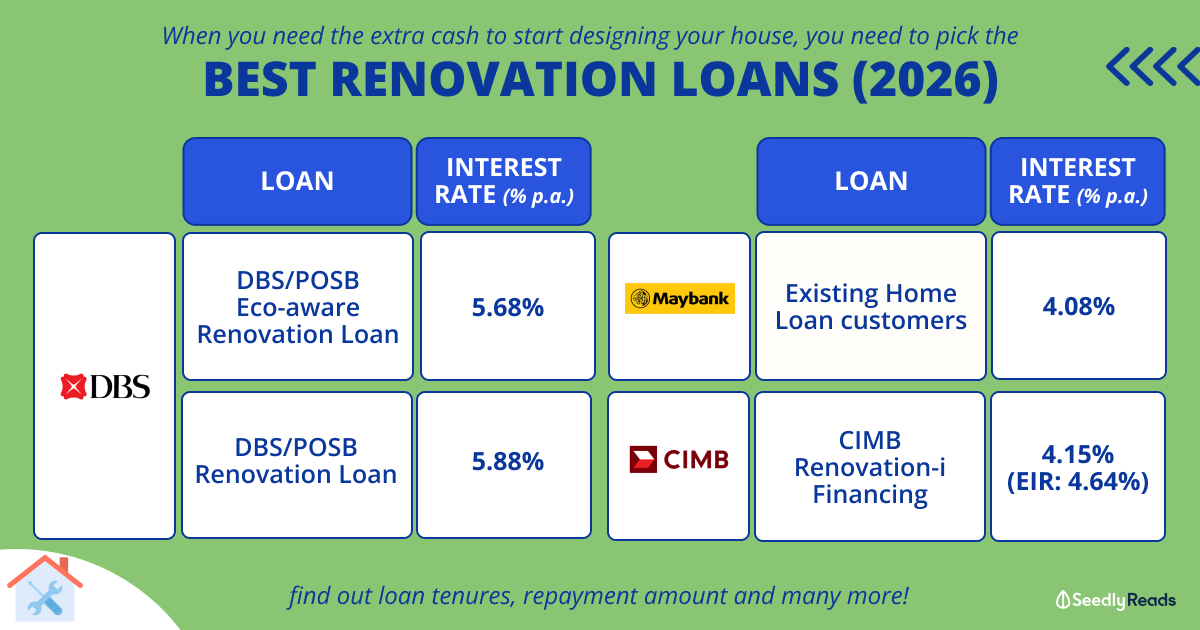

Best Renovation Loans in Singapore (2024)

When people search for the best renovation loan Singapore has to offer, the lowest advertised rate is usually the first thing they look at.

But that shouldn’t be the only deciding factor.

Instead, compare the more durable details first: eligibility, loan quantum, fees, tenure, disbursement method, and whether the loan suits your renovation needs.

| Renovation loan / bank | What to know before applying |

|---|---|

| DBS/POSB Renovation Loan | Available to Singapore Citizens or PRs aged 21 to 65, subject to eligibility. DBS states that borrowers can apply for up to six times monthly income or S$30,000, whichever is lower. DBS currently lists a 2% handling fee and 1% insurance premium. |

| DBS/POSB Eco-aware Renovation Loan | This is DBS’ eco-focused renovation loan option. DBS states that applicants must fulfil at least six out of 10 items under its Eco-aware Renovation Checklist to enjoy the Eco-aware rate. |

| Maybank Renovation Loan | Maybank states that its renovation loan is for Maybank Home Loan customers. Its personal loans page states that the loan amount is up to six times monthly income or S$30,000, whichever is lower, and the tenure is up to five years. Maybank’s application page lists a 2% processing fee, minimum S$200. |

| CIMB Renovation-i Financing | CIMB’s official fees page lists CIMB Renovation-i Financing fees, including a 1.55% processing fee, 1% cancellation fee, 1% prepayment fee, S$80 late payment fee, and cashier’s order charges. Check CIMB’s official application page or contact CIMB directly for the latest active rate before publication. |

| OCBC Renovation Loan | OCBC should not be listed as an active renovation loan provider. OCBC’s official home loans page states that it does not offer renovation loans. |

What About Monthly Repayments?

Monthly repayments depend on:

- Loan amount

- Tenure

- Interest rate

- Effective interest rate

- Processing or handling fees

- Insurance premiums

- Bank-specific rounding and repayment schedule

Because interest rates and fees can change, always check the bank’s official repayment schedule before applying. The final repayment shown by the bank should take priority over any estimate.

This is especially important if you are comparing a home renovation loan Singapore package against a personal loan, credit line, or paying in cash. The cheapest option is not always the one with the lowest headline rate — it is the one with the lowest overall cost that still fits your cash flow.

So… Should You Still Take A Home Reno Loan?

There are two schools of thought:

Take The Home Reno Loan

A renovation loan can make sense if you need help with cash flow and are confident that you can afford the monthly repayment.

This may apply if:

- You want to keep some emergency cash on hand

- Your renovation cost is higher than expected

- You have stable income

But remember: the loan amount is not the same as the amount you receive.

Some banks deduct fees from the approved loan amount. DBS states that its handling fee and insurance premium are deducted from the approved loan amount. CIMB also states that its processing fee is deducted upon financing disbursement.

So if you are approved for S$30,000, you may receive less than S$30,000 after fees.

Before applying, calculate the total cost of borrowing, not just the interest rate.

Start Saving Now

If your BTO or resale completion is still some time away, saving up early can reduce how much you need to borrow.

A simple approach is to create a renovation fund and contribute to it monthly.

For example, you can set aside money for:

- Renovation works

- Furniture

- Appliances

- Moving costs

- Emergency repairs

- Temporary accommodation, if needed

The more you save before collecting your keys, the less you may need to borrow later.

Some homeowners also prefer to pay part of the renovation in cash and borrow only for the shortfall. This can help reduce interest costs while preserving some liquidity.

For big-ticket purchases, using a credit card can be useful only if the merchant accepts cards and the rewards are worth more than any processing fees. Do not use a credit card just to earn miles or cashback if it causes you to overspend or carry high-interest credit card debt.

Also remember that renovation loan disbursements may be made directly to your contractor, not to you personally. DBS states that cashier’s orders are issued under the appointed renovation contractor’s name.

Building Your Dream Home

Whether you decide to take a home renovation loan or not, have a proper discussion with your partner and work out a realistic budget.

Your budget should include:

- BTO or resale flat payments

- Renovation works

- Furniture

- Appliances

- Curtains and blinds

- Moving costs

- Wedding or ROM expenses, if applicable

- Emergency savings after moving in

Once you know your full cost, you’ll be in a better position to decide whether you need a renovation loan, how much to borrow, and how quickly you can repay it.

The goal is not to create the most impressive home on Instagram.

The goal is to build a home that you enjoy living in — while still sleeping well at night.

Have more home renovation loan-related questions? Why not ask the Seedly community?

Advertisement