Here's How You Can Protect Yourself From the Growing Trend of People Unable to Refund CPF Used for Housing

Getting a house in Singapore is not easy, at all.

Given our limited land space, it’s honestly no surprise that our property prices are “off the roof”.

Lame puns aside, we all have it hard when it comes to buying our first house, with so many barriers to applying for our first Build to Order (BTO) flats.

But thankfully, we can use the money in our Central Provident Fund (CPF) Ordinary Account (OA) to pay for our housing!

But here’s the ‘catch’. We need to refund the amount taken out of our CPF OA with interest if we ever sell the house in the future to ensure we have enough for retirement.

This accrued interest as it is called is computed on the amount taken out of our CPF OA at a rate of 2.5% per annum. Not forgetting that this interest is compounded annually.

Thus, the amount we have to refund to our CPF OA can really snowball if we are not careful.

Lucky for you potential new homeowners, we might just have a solution. Enter the Voluntary CPF Housing Refund.

TL;DR: Step-by-Step Guide to Making a Voluntary CPF Housing Refund

The Rising Trend of People Unable to Repay CPF Money Used for Housing

Over the years, there has been a rising trend in the number of people who are unable to repay their CPF money used to finance their housing when they sell their property:

In 2018, roughly 3,380 people were unable to fully repay the CPF money used for housing.

In 2019, it rose to 3,960 people.

In 2020, there were 4,580 people who cannot fully repay the CPF money.

According to a report on CPF trends, the percentage of people unable to repay the CPF money when they sell their house has been growing, with an 8% increase in 2018, an 11% increase in 2019, and a 13% increase in 2020.

So why is there an increasing number of people who cannot repay the CPF money used for housing?

Imagine this, you want to buy a house, but you don’t have enough money.

Of course, with the government providing a simple solution where you can withdraw money from your CPF OA to help fund your housing, that doesn’t seem like such a big problem, does it?

But here’s the catch:

When you sell your house, you are required to make refunds from the sales proceeds.

Otherwise, you are required to make two refunds:

First, your existing home loan’s outstanding balance needs to be paid back. This could be your HDB home loan or bank loan. This is the first refund that needs to be made and takes priority over everything else.

Secondly, you will need to refund all the CPF funds you took out from your CPF savings inclusive of the principal and the accrued interest.

This can include expenses like the downpayment, lawyer’s fees, stamp duties and HDB grants.

The amount you have to refund generally consists of the principal amount you took out from your CPF OA as well as the accrued interest that compounds annually and is calculated from the date you withdrew money from your CPF OA.

In other words, you will have to refund the interest on the principal amount based on the current CPF-OA interest rate of 2.5% p.a.!

Here’s an example of how the accrued interest works:

Think of it as a reverse interest; the longer the money is out of the account, the more the accrued interest you’ll have to refund into your CPF OA when you sell your property.

This may result in a negative cash sale, a scenario where you might have to refund cash to your CPF OA when selling your house.

Here is an example of a negative cash sale:

| Selling Price | $460,000 |

|---|---|

| Outstanding Mortgage Loan | $300,000 |

| Remaining Sales Proceeds After Paying Off Outstanding Mortgage Loan | $160,000 |

| Total Required CPF Refund (Principal Amount + Accrued Interest) | $180,000 + $48,000 = $228,000 |

| Negative Sale (Remaining Sale Proceeds – Total Required CPF Refund) | $160,000 – $228,000 = -$68,000 |

In the illustration above, there is a negative cash sale of $68,000.

However, in the event that there is a negative cash sale and the amount that you have to refund to your CPF savings is more than your sale proceeds in cash, CPF will write off the additional amount.

In other words, you will not have to fork out any cash above the sales proceeds from your HDB flats. But, do note that this is only the case if you managed to sell your property at either its market value or above it.

In the event that you sell your property at below its market value and the amount that you have to refund to your CPF OA is more than your sale proceeds in cash; you will be required to refund all the money you took out of your CPF account plus accrued interest.

This means that you will have to top up cash to make up for the shortfall.

But on balance, you can write to CPF and appeal to write off this ‘debt’ if you are strapped for cash. Approval however is up to CPF’s discretion and is judged on a case-by-case basis.

To avoid this situation, you can make either a partial voluntary housing refund or a full voluntary housing refund to reduce the amount of accrued interest you have to refund.

This will reduce the amount of CPF savings that need to be refunded when you sell your property.

After all compound interest works both ways.

The sooner you refund your CPF savings, the less you have to refund to your CPF accounts when you sell or transfer the property.

What Is a Voluntary CPF Housing Refund and Why Should You Make One?

Think about accrued interest and how you can reduce the accrued interest you will have to pay with the CPF voluntary housing refund.

Although not the best solution, one way we believe that could help minimise the effects of this issue is if you made a Voluntary CPF Housing Refund.

A Voluntary CPF Housing Refund can be made when you top up money to your CPF OA in order to pay back the amount you have used when purchasing your house.

Besides the biggest benefit of reducing the amount of money you need to pay back to your CPF when you sell your house in the future, there are other benefits to making a Voluntary CPF refund as well, these include:

- Ensuring you have a larger retirement fund since the funds inside your CPF will keep growing thanks to compound interest

- The money you have paid back can be channelled towards other CPF schemes such as the CPF Investment Scheme (CPFIS)

Of course, you have to take note that you cannot withdraw that money until you are at least 55 years old, so as much as you are eager to cut down the repayment amount, make sure you save enough for a rainy day.

Step-by-Step Guide to Making a Voluntary CPF Housing Refund

Ready to reduce the amount of interest you need to repay your CPF OA for your housing loans?

There are two ways in which you can make a Voluntary CPF Refund, via the myCPF Digital Services website or via the CPF Mobile App

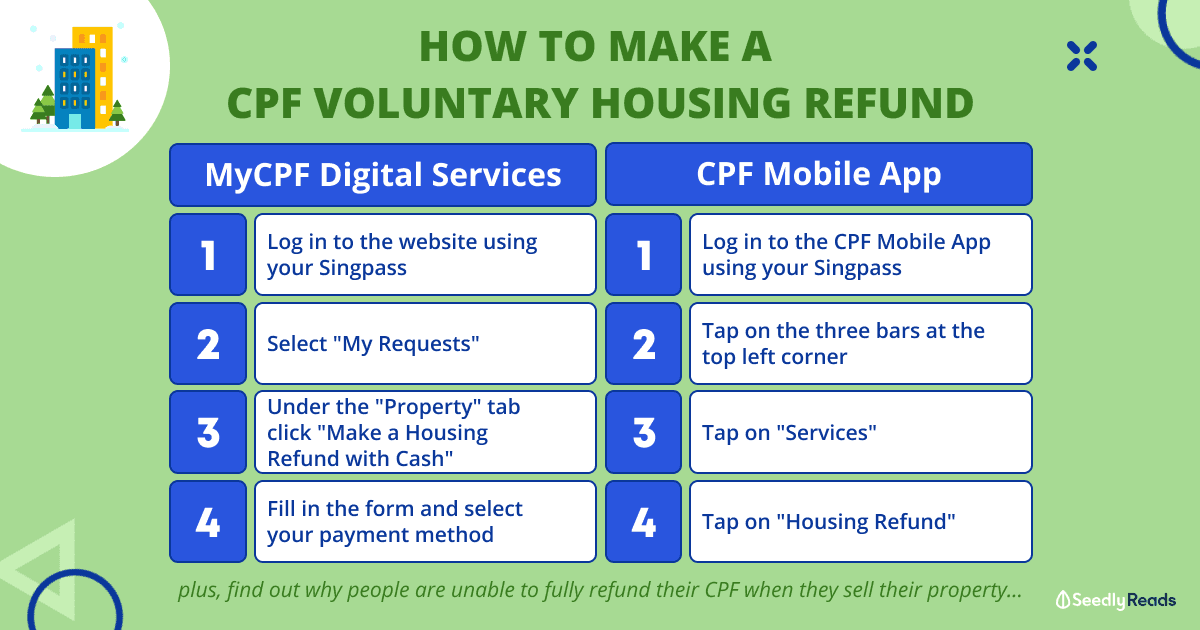

Here are the steps for the myCPF Digital Services website:

- Log in to the website using your Singpass

- Select “My Requests” on the Digital Services website

- Under the “Property” tab, click on “Make a Housing Refund with Cash”

- Fill in the form and select your payment method

Here are the steps for using the CPF Mobile App:

- Log in to the CPF Mobile App using your Singpass

- Tap on the three bars at the top left corner

- Tap on “Services”

- Tap on “Housing Refund”

Closing Thoughts

In the spirit of the upcoming Lunar New Year, one famous superstition is that it is bad luck to owe debts across the new year.

Keeping that in mind, I guess a debt to the government kinda counts? So try to repay what you owe your CPF OA for your housing.

Looking for ways to boost your luck this Lunar New Year?

Here’s how you can get good luck by simply depositing your money at the right time!

Advertisement