Looking for the best digital bank Singapore has to offer? With more people using digital banking in Singapore, digital savings accounts can be a convenient place to park spare cash, separate savings goals, or manage day-to-day spending from your phone.

That said, the “best” account depends on what you value most: a no-frills rate, higher interest with conditions, ecosystem perks, or simple app-based banking. Here’s an updated look at the main digital bank savings accounts Singapore users tend to compare: Trust Bank, GXS Bank, and MariBank.

Disclaimer: Rates, fees, eligibility, and product terms can change. Always check the bank’s official website or app before applying.

TL;DR: Best Digital Bank Accounts (2026)

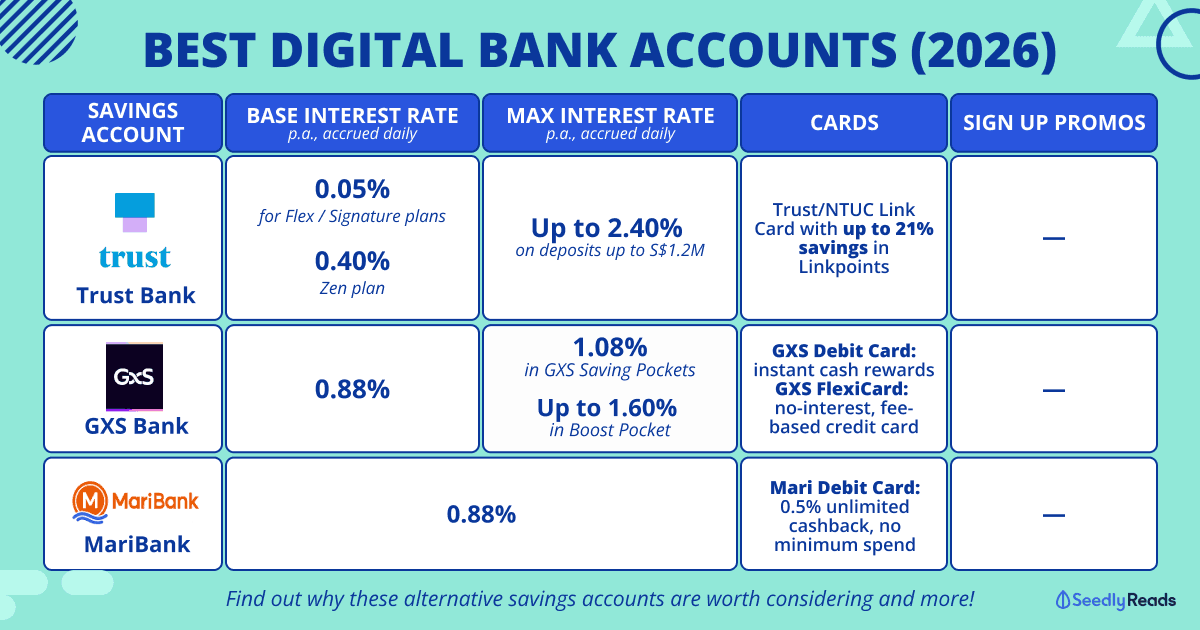

| Account | Base interest rate (p.a., accrued daily) | Bonus interest (p.a., accrued daily) |

|---|---|---|

| GXS Savings Account | Main Account: 0.88% p.a.; Saving Pockets: 1.08% p.a.; Boost Pockets: 1.01% to 1.60% p.a. depending on tenure | Saving Pockets remain useful for goals-based saving. Maximum balance varies by customer and can be up to S$95,000. |

| Mari Savings Account | 0.88% p.a. on all balances | Simple, fuss-free structure: no minimum deposit, no salary crediting, and no minimum spending required. Interest is credited daily. |

| Trust Bank Savings Account | Zen: flat 0.40% p.a.; Signature: up to 1.00% p.a.; Flex: up to 2.40% p.a. 0.05% for deposits above $500k | Trust now has three savings plans. The highest rate requires meeting bonus-interest conditions. Headline rates apply on deposits up to S$1.2 million; balances above that earn 0.05% p.a. |

Jump to:

- What is a digital bank?

- Trust Bank

- GXS Bank

- MariBank

- Should You Consider Opening an Account with a Digital Bank?

Disclaimer: The information provided by Seedly serves as an educational piece and is not intended to be personalised financial advice. Readers should always do their own due diligence and consider their financial goals before committing to any financial product. The article was updated on Wed (05 Jul 2026) to reflect the latest changes to Trust Bank’s cap increases.

What is a Digital Bank? Digital Banks vs Traditional Banks

A digital bank is a bank that lets you manage your account mainly through an app or website, rather than through a physical branch. For everyday users, this usually means digital onboarding, app-based transfers, lower-friction account management, and in some cases, fewer account fees.

However, digital banks are not all the same. MAS licenses GXS Bank and MariBank as digital/local banks, while Standard Chartered and FairPrice Group back Trust Bank, a digitally native full bank.

Services can also differ. For example, GXS states that its savings account has no cash or cheque services, although it supports FAST, PayNow, and receiving funds via inter-bank GIRO. Trust, on the other hand, supports PayNow and ATM withdrawals at Trust or Standard Chartered ATMs.

Retail Vs. Wholesale Vs. Full Digital Bank Licenses

In Singapore, MAS’s digital bank licence framework has two categories: Digital Full Banks and Digital Wholesale Banks. Digital Full Banks may serve retail customers and take retail deposits, while Digital Wholesale Banks focus on SMEs and other non-retail customer segments.

In December 2020, MAS awarded two Digital Full Bank licences to the Grab–Singtel consortium and Sea Group; these are now represented by GXS Bank and MariBank. MAS also awarded two Digital Wholesale Bank licences, now operated by ANEXT Bank and Green Link Digital Bank, which primarily serve micro, small and medium-sized enterprises and other non-retail clients.

Separately, Trust Bank is also a digital-first bank in Singapore, but it is not part of the 2020 MAS digital-bank licence cohort. It operates under a Full Bank licence and is backed by Standard Chartered Bank and FairPrice Group, allowing it to offer retail banking services in a manner closer to a conventional full bank, albeit through a digital-first model.

Are Digital Banks Safe?

MAS regulates digital banks in Singapore, but you should still understand what protection applies.

For eligible Singapore-dollar deposits, the Deposit Insurance Scheme protects deposits with a Scheme member up to S$100,000 per depositor per Scheme member. This generally covers SGD savings, current, and fixed deposit accounts, but not foreign-currency deposits, structured deposits, structured notes, or investment products.

That means the same protection may not apply to your bank savings account and your investment or insurance-linked product. For example, SDIC does not insure TrustInvest funds, while the PPF Scheme protects the Singlife Account as an insurance savings product, not under the bank Deposit Insurance Scheme.

Trust Bank

![]()

Standard Chartered and FairPrice Group back Trust Bank, a digital-first bank. It operates through the Trust App and offers a savings account, debit card, credit cards, loans, insurance, and investment access.

Trust Bank Savings Account Interest Rates (2026)

| Trust Savings plan | Current rate | How it works |

|---|---|---|

| Zen | Flat 0.40% p.a. | The fuss-free option with no bonus hoops. |

| Signature | Up to 1.00% p.a. | Earn bonus interest when you meet selected earn, spend, or save conditions. |

| Flex | Up to 2.40% p.a. | Starts from 0.05% p.a. base rate and lets you choose any three bonus-interest “scoops” each month. |

Trust advertises up to 2.40% p.a. interest on deposits up to S$1.2 million, and states that balances above S$1.2 million earn 0.05% p.a.

For the Flex plan, available bonus-interest options include:

| Bonus-interest action | Current bonus rate |

|---|---|

| Refer a new Trust credit card customer who successfully signs up | +1.20% p.a. |

| Purchase total S$20,000 of eligible TrustInvest funds | +0.70% p.a. |

| Credit min. S$1,500 monthly salary via GIRO | +0.45% p.a. |

| Keep min. S$100,000 Average Daily Balance | +0.30% p.a. |

| Make 5 × S$30 qualifying card spends | +0.20% p.a. for NTUC Union members; +0.10% p.a. for non-union members |

| Increase ADB by S$3,000 from the previous month | +0.20% p.a. |

| Receive total S$1,500 incoming PayNow | +0.15% p.a. |

| Spend total S$500 in foreign currency | +0.15% p.a. |

Trust states that bonus interest applies for the full month once you unlock the relevant condition.

Trust Bank Savings Account Key Information

- Minimum balance requirement: None

- Fall-below fee: None

- Monthly service fee: None

- Account closure fee: None

- Card annual fee: None

- Interest crediting: Calculated at the end of each day and paid monthly

- PayNow: Supported

- ATM withdrawal: No Trust fee at Trust / Standard Chartered ATMs; overseas ATM withdrawals may be available, but overseas ATM operators may charge fees

- Cheques: No cheque book and cheque deposits are not supported

Trust Bank Cards

Trust’s card lineup now includes the Trust Link / NTUC Link credit card and the Trust Cashback Credit Card.

For the Trust Link / NTUC Link credit card, Trust states that there is no annual fee and no foreign transaction fee. It also advertises up to 21% savings on groceries and food at FairPrice Group when you spend on credit card.

For the Trust Cashback Credit Card, Trust advertises up to 1% unlimited instant cashback on eligible spend and up to 15% bonus cashback on a preferred category, with the 15% cashback capped at S$250 per quarter.

GXS Bank

Grab and Singtel founded GXS Bank as one of the first two digital banks to serve retail customers.

Recently, GXS has rolled out the GXS Debit Card, a welcome addition to its banking ecosystem.

GXS Savings Account Interest Rates

| GXS Account Feature | Current rate | Notes |

|---|---|---|

| Main Account | 0.88% p.a. | For regular transactions. |

| Saving Pockets | 1.08% p.a. | Useful for separating savings goals. |

| Boost Pocket — 1 month | 1.01% p.a. | Base + bonus rate fixed for selected tenure. |

| Boost Pocket — 3 months | 1.22% p.a. | Bonus interest is tied to the selected tenure. |

| Boost Pocket — 4 months | 1.40% p.a. | - |

| Boost Pocket — 8 months | 1.30% p.a. | - |

| Boost Pocket — 12 months | 1.60% p.a. | Highest current GXS Boost Pocket rate listed in official help page. |

GXS says daily interest is based on the aggregate balance of the Main Account and Saving Pockets at the end of each day, and credited once accumulated interest reaches at least S$0.01. Boost Pocket interest rates are fixed for the selected tenure and consist of base plus bonus interest.

GXS Savings Account Key Information

GXS Saving Pockets

GXS Saving Pockets are useful if you want to split your money into goals, such as emergency funds, travel, or home expenses. You can move funds between your Saving Pockets and Main Account through the app.

Boost Pockets work differently: they offer higher base-plus-bonus rates depending on tenure, but if you close a Boost Pocket before the lock-in period ends, GXS says you earn the base interest to date and forfeit the bonus interest.

MariBank

![]()

MariBank is part of the Sea ecosystem and integrates with Shopee. Its Mari Savings Account is one of the more straightforward digital savings bank options: one stated base rate, no minimum deposit, no salary crediting, and no minimum card spend.

Maribank Savings Account Interest Rates

Mari Savings Account currently earns 0.88% p.a. on all balances. MariBank states that interest is credited daily and calculated based on the previous day’s balance.

Maribank Savings Account Key Information

Maribank Sign Up

You can open a Mari Savings Account digitally through the MariBank app using MyInfo via Singpass. MariBank states that no documents are needed when your details are retrieved via MyInfo.

Should You Consider Opening an Account with a Digital Bank?

A digital bank savings account can be useful if you want a low-maintenance account, app-first experience, or a way to separate short-term savings goals. But it should not be chosen based on headline interest rate alone.

Digital banks can work well as secondary savings accounts, especially for emergency funds, short-term savings goals, or spending buckets.

For a no-hoops setup, compare the plain rates first:

| Account | Fuss-free rate / base option |

| GXS Saving Pockets | 1.08% p.a. |

| Mari Savings Account | 0.88% p.a. |

| Trust Zen plan | 0.40% p.a. |

If you are willing to meet salary, spend, balance, PayNow, investment, or referral conditions, Trust’s Flex or Signature plans may offer higher rates. But the conditions are more involved, so check whether you would realistically meet them each month.

Digital Banks vs Singlife Account

Singlife Account is not a bank savings account or fixed deposit. It is an insurance savings solution. That makes it different from the digital bank savings accounts above.

Current Singlife Account base returns are:

| Singlife Account balance tier | Current base return |

| First S$10,000 | 1.5% p.a. |

| Above S$10,000 to S$100,000 | 1.0% p.a. |

| Above S$100,000 | No base returns |

Singlife states that returns are calculated daily and credited monthly, but crediting rates are not guaranteed. It also states that the Singlife Account is protected under the Policy Owners’ Protection Scheme, administered by SDIC, rather than the bank Deposit Insurance Scheme.

Under the PPF Scheme, MoneySense states that individual life and voluntary group life policies have limits of S$500,000 for guaranteed sum assured and S$100,000 for guaranteed surrender value per life assured per insurer.

Digital Bank Pros and Cons

| Pros | Cons |

|---|---|

| Interest accrued daily (i.e. interest compounds faster than traditional banks that credits interest monthly) | No physical bank branches. |

| Little to no fees compared to traditional banks | Limited number of ATMs and CDMs. |

| No minimum monthly balance! | Services are maintained online and hence more susceptible to technological issues. |

| 24/7 helplines and support services | |

| More efficient and flexible than traditional banks due to use of technology |

After all, putting all your eggs into one basket is not a good idea.

If you do not own a savings account with a traditional bank

A digital bank savings account can be a practical first account if you are comfortable banking mainly through an app. But do not ignore basic access needs. If you regularly need cash deposits, cheque handling, branch assistance, or complex bank services, you may still want to keep a traditional bank account.

Also, keep the SDIC limit in mind. Eligible SGD deposits are insured up to S$100,000 per depositor per Scheme member, not per account.

If you are an NTUC Union member or shop at Fairprice frequently

Trust Bank is worth comparing if you shop frequently at FairPrice Group or use Link rewards. Trust advertises up to 21% savings on groceries and food at FairPrice Group when you spend on the Trust Link credit card, subject to its terms.

The old OCBC / NTUC Plus! Visa Cards should not be treated as a current comparison point. Link Rewards states those cards stopped earning and redeeming Linkpoints after 31 Jan 2023, and points users to Trust cards, the FairPrice app, or Link Rewards card options instead.

Related Articles

Advertisement