Understanding (SDIC) Singapore Deposit Insurance Corporation Insurance & Why it Matters

Update: On Friday (22 Sep 2023), The Monetary Authority of Singapore (MAS) announced that they are raising DI coverage from $75,000 to $100,000 per bank per person from 1 April 2024.

Protected up to specified limits by SDIC

Seem familiar?

You’ve probably come across this line as a fine print at the bottom of a marketing product from financial institutions. But what exactly are you protected for, and how much is the limit?

Let’s find out what the Singapore Deposit Insurance Corporation (SDIC) is and the schemes it administers!

TL;DR: What is SDIC, and How Much Am I Insured For?

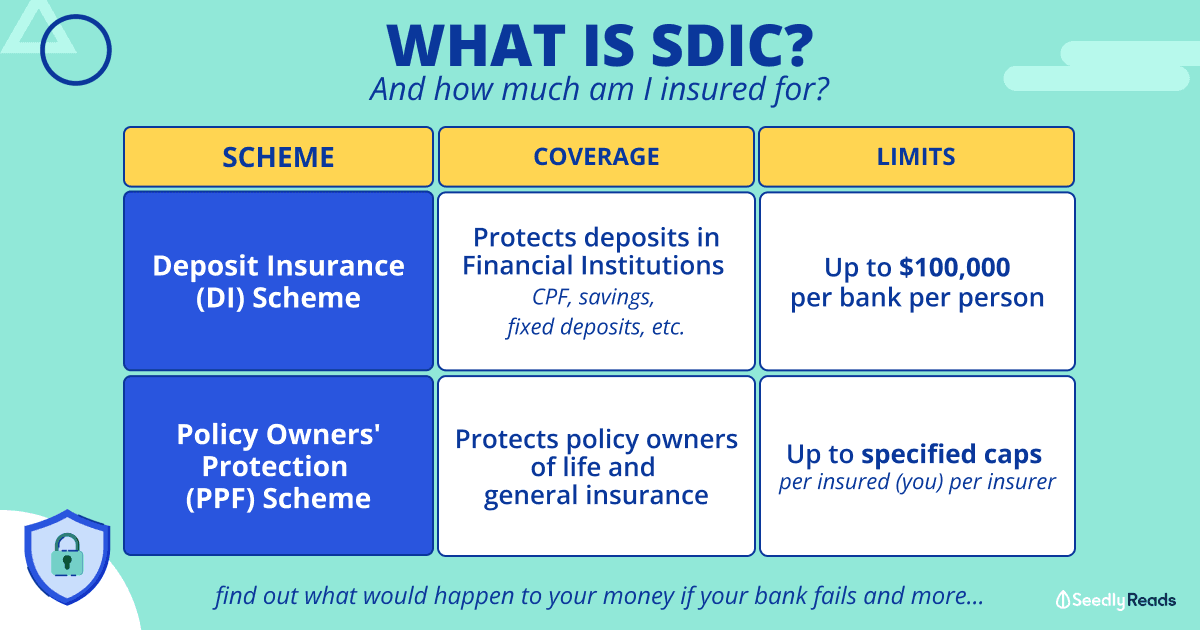

- The Deposit Insurance (DI) Scheme by SDIC guarantees deposits in a bank up to $75,000 per bank per person.

- On Friday (22 Sep 2023), The Monetary Authority of Singapore (MAS) announced that they are raising DI coverage from $75,000 to $100,000 per bank per person from 1 April 2024

- If a bank fails, compensation will be automatic once MAS declares the bank insolvent.

- The Policy Owners’ Protection (PPF) Scheme protects policy owners up to specified caps.

- If an insurer fails, policy owners would be compensated by SDIC according to the applicable protection ratios and guaranteed policy liabilities.

Jump To:

- What Is SDIC?

- What Is the Deposit Insurance Scheme?

- What Is Covered Under The Deposit Insurance Scheme?

- What Is the Policy Owners’ Protection Scheme?

- What Is Covered Under the Policy Owners’ Protection Scheme?

- Author’s Note

What Is SDIC Singapore? SDIC Rules and SDIC Insured Explained

SDIC stands for the Singapore Deposit Insurance Corporation, which administers the Deposit Insurance (DI) Scheme and Policy Owners’ Protection (PPF) Scheme in Singapore.

The SDIC board of directors is accountable to the Minister in charge of MAS.

Additionally, Singapore requires that all finance companies and full banks in Singapore join the Deposit Insurance Scheme.

If you have SDIC insurance, this typically indicates that the DI Scheme will cover your insured amounts up to a certain cap. In the event that your bank or finance firm collapses, SDIC will reimburse you for the insured amounts.

Is SDIC Part of the Government?

Although they are accountable to MAS, SDIC is not a part of the government and is a company limited by guarantee under the Companies Act.

What Is the Deposit Insurance Scheme?

Banks are some of the safest places where you can park your money. Yet things have gone wrong before, and even the world’s top banks can fail.

While Singapore’s licensed banks and financial institutions are supervised by the Monetary Authority of Singapore (MAS), MAS does not guarantee the soundness of individual financial institutions.

How can we protect our core savings if things go south?

Enter the Deposit Insurance Scheme administered by the Singapore Deposit Insurance Corporation (SDIC).

The Deposit Insurance (DI) Scheme provides basic protection to small depositors.

Bank Deposit Insurance Singapore

Currently, the DI scheme guarantees deposits in a bank up to $75,000 per bank per person.

In other words, if you have an account with DBS that fails in some doomsday scenario, MAS will declare DBS insolvent, and SDIC will automatically compensate you up to $75,000.

Singapore requires all full banks and finance companies to be members of the Deposit Insurance Scheme. As such, this covers all banks in Singapore, including digital banks.

Monetary Authority of Singapore (MAS) to Raise SDIC Insurance to $100k

Speaking of the DI scheme, MAS has announced on 27 June that they are proposing to raise DI coverage per depositor from $75,000 to $100,000.

On the morning of 22 September, it was confirmed that the proposal was accepted and that the changes would take effect from 1 April 2024.

The regulator stated that:

the Maximum DI Coverage was last increased in 2019 from $50,000 to $75,000 for relevant insured deposits per depositor per DI Scheme member, fully insuring 91% of insured depositors covered under the DI Scheme then. With deposit growth over time, the percentage of fully-covered insured depositors has since fallen slightly to 89%.

Hence, we (MAS) propose to increase the Maximum DI Coverage from $75,000 to $100,000 with effect from 1 April 2024.

This will restore the percentage of fully-covered insured depositors to 91%. The proposed increase aims to improve DI coverage for small depositors while keeping the expected increase in DI Scheme members’ premiums manageable, as these costs are ultimately passed on to bank customers.

In a sense, MAS is looking to continue the majority of small depositors and keep them insured as average deposit balances grow. This amount was also calculated to balance covering the majority of small depositors and managing the cost of premiums.

Additionally, MAS recommends that the DI scheme grant the regulator the authority to specify a particular time when deposit balances are considered final. The suggestion seeks to make the calculation of DI compensation more transparent.

As claims become less frequent over time, the agency also recommends a time restriction for DI compensation applications to keep administrative expenses down.

DI Deposit Protection Scheme: Bank Deposit Guarantee and Insurance Protection for Your Monies

SDIC insures Singapore dollar-denominated deposits placed with a DI Scheme member in any of its branches in Singapore.

These include:

- A deposit held in a savings account

- A deposit held in a fixed deposit account

- A deposit held in a current account

- Any monies placed under the CPF Investment Scheme

- Any monies placed under the CPF Retirement Sum Scheme

- Any monies placed under the Supplementary Retirement Scheme

- Other products, as prescribed by the Authority.

However, it does not insure financial products such as

- Foreign currency deposits

- Structured deposits

- Investment products such as unit trusts, shares and other securities.

Moreover, all your insured deposits placed with that member are aggregated and insured up to $75,000. So having multiple accounts with a total value of more than $75,000 in a single bank will still only guarantee up to $75,000.

CPIFS Fixed Deposit

The only exception to this is CPF. Monies placed with a DI Scheme member under the CPF Investment Scheme (CPFIS) and CPF Retirement Sum Scheme (CPFRS) are aggregated and separately insured up to $75,000.

What Is the Policy Owners’ Protection Scheme?

Like the DI scheme, the Policy Owners’ Protection (PPF) Scheme has been set up to protect policy owners if a life or general insurer fails, a PPF Scheme member.

What Is Covered Under the Policy Owners’ Protection Scheme?

Under the scheme, both life and general insurance policies are covered.

Life insurance includes all types of life insurance, endowment policies, annuities, and long-term accident and health (A&H) policies. General insurance includes all compulsory insurance policies under the Motor Vehicles (Third Party Risks and Compensation) Act, Work Injury Compensation Act, and short-term accident and health (A&H) policies.

SDIC will compensate policy owners for claims, surrenders of policies, maturity of policies, and ongoing annuity payments which occurred before MAS decides to activate the use of the PPF Fund.

Of course, there are applicable caps which are as follows:

- Individual life and voluntary group life policies (with the exception of annuities): Cap of $500,000 for the aggregated guaranteed sum assured and $100,000 for aggregated guaranteed surrender value per life assured per insurer.

- Individual and voluntary group annuities: Cap of $100,000 for the aggregated commuted value of guaranteed benefits (i.e. annuity payments, death or surrender benefits) per life assured per insurer.

- Non-voluntary group term life policies: Cap of $100,000 for guaranteed sum assured per policy.

- Non-voluntary group whole life or endowment policies: Cap of $100,000 for guaranteed sum assured and $50,000 for guaranteed surrender value per policy.

- Non-voluntary group annuities: Cap of $100,000 for the commuted value of guaranteed benefits per policy.

For general insurance, there are usually no limits in terms of PPF coverage except in the following instances:

- Limits specified under the law for compulsory insurance policies

- $50,000 for own property damage motor claims under personal motor insurance policies

- $300,000 for property damage claims under personal property (structure and contents) insurance policies.

Author’s Note

Now that we know about SDIC, the schemes they administer, and what they cover, here is what I would do with that information.

Although Singapore’s financial system has been rock solid, the global financial situation has shown us that even top banks can suffer from bank runs and fail.

Whether it is signing up for insurance or depositing money in the bank, diversifying even your bank monies and insurance policies is not such a bad idea. After all, it is better to be safe than sorry!

Related Articles

Advertisement